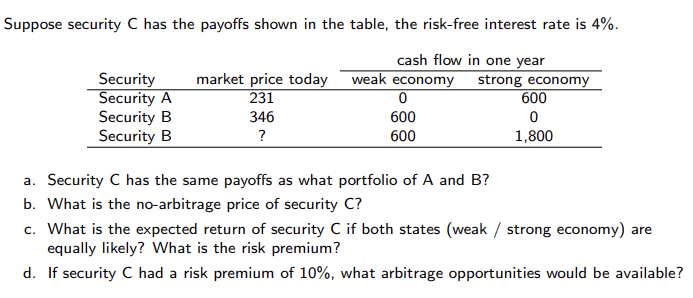

Question: Suppose security C has the payoffs shown in the table, the risk-free interest rate is 4%. a. Security C has the same payoffs as what

Suppose security C has the payoffs shown in the table, the risk-free interest rate is 4%. a. Security C has the same payoffs as what portfolio of A and B ? b. What is the no-arbitrage price of security C ? c. What is the expected return of security C if both states (weak / strong economy) are equally likely? What is the risk premium? d. If security C had a risk premium of 10%, what arbitrage opportunities would be available

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock