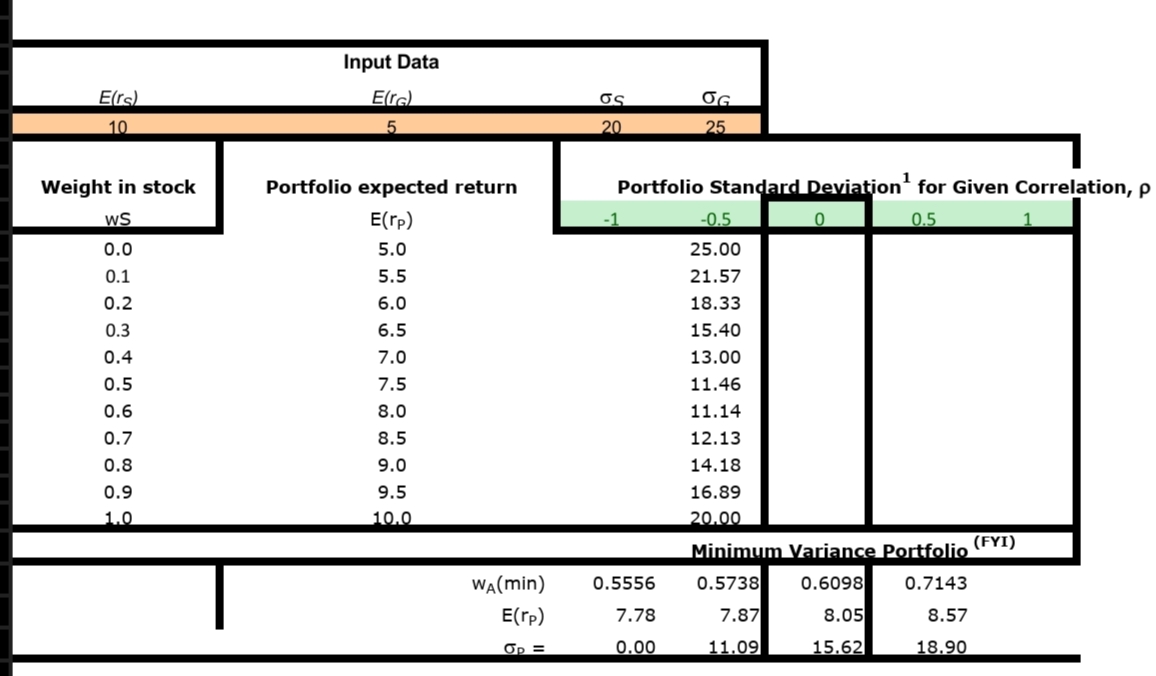

Question: Suppose stocks ( denoted by subscript S ) offer an expected rate of return of 1 0 % with a standard deviation of 2 0

Suppose stocks denoted by subscript S offer an expected rate of return of with a standard deviation of and gold denoted by subscript G offers an expected return of with a standard deviation of

a Create the investment opportunity set of stocks and gold if the correlation coefficients are and respectively. Attach the graph to your spreadsheet.

Hint: copy the formulas to other correlation coefficients and graph the curves.

b Briefly comment on how the correlation of both assets determines the risk of the risky portfolio consisting of stocks and gold.

c Suppose that the correlation coefficient is Along the corresponding investment opportunity set, identify the portfolio of risky assets where the weight in stock of the portfolio is and thus the weight in bond is also Also, identify another portfolio that would be dominated by this portfolio based on the meanvariance criterion.

d Continuing from c if the investor can buy a Treasury Bill that pays in returns with certainty, what is the Sharpe ratio of this risky portfolio?

e Continuing from c and d is the portfolio from part c an optimal one, or can you find a better portfolio? Give an example of such a portfolio along the investment opportunity set

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock