Question: Suppose that stock returns are generated by a two-factor model. The expected returns and factor sensitivities of two well-diversified portfolios A and B are given

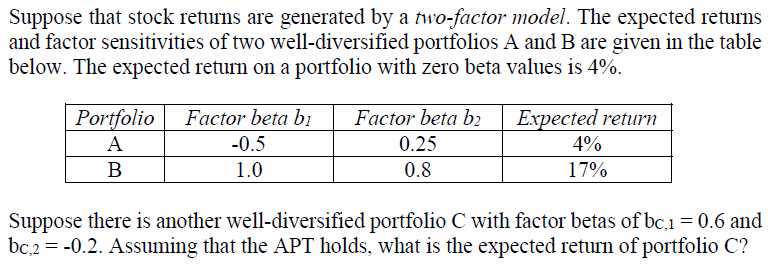

Suppose that stock returns are generated by a two-factor model. The expected returns and factor sensitivities of two well-diversified portfolios A and B are given in the table below. The expected return on a portfolio with zero beta values is 4%. Portfolio A B Factor beta bi -0.5 1.0 Factor beta b2 0.25 0.8 Expected return 4% 17% Suppose there is another well-diversified portfolio C with factor betas of bc,1 = 0.6 and bc,2 = -0.2. Assuming that the APT holds, what is the expected return of portfolio C

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock