Question: Suppose that the current and expected future short-term interest rates are given by: i_t = 0.03 i^e_t + 3 = 0.06 i^e_t + 1 =

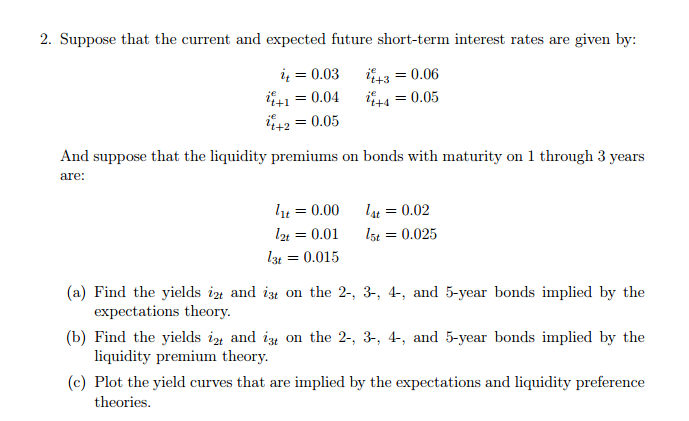

Suppose that the current and expected future short-term interest rates are given by: i_t = 0.03 i^e_t + 3 = 0.06 i^e_t + 1 = 0.04 i^e_t + 4 = 0.05 i^e_t + 2 = 0.05 And suppose that the liquidity premiums on bonds with maturity on 1 through 3 years are: l_1t = 0.00 l_2t = 0.01 l_3t = 0.015 l_4t = 0.02 l_5t = 0.025 (a) Find the yields i_2t and i_3t on the 2-, 3-, 4-, and 5-year bonds implied by the expectations theory. (b) Find the yields i_2t and on the 2-, 3-, 4-, and 5-year bonds implied by the liquidity premium theory. (c) Plot the yield curves that are implied by the expectations and liquidity preference theories

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock