Question: Suppose that we back-test a VaR model using 1,300 days of data. The VaR confidence level is 99% and we observe 15 exceptions. Should we

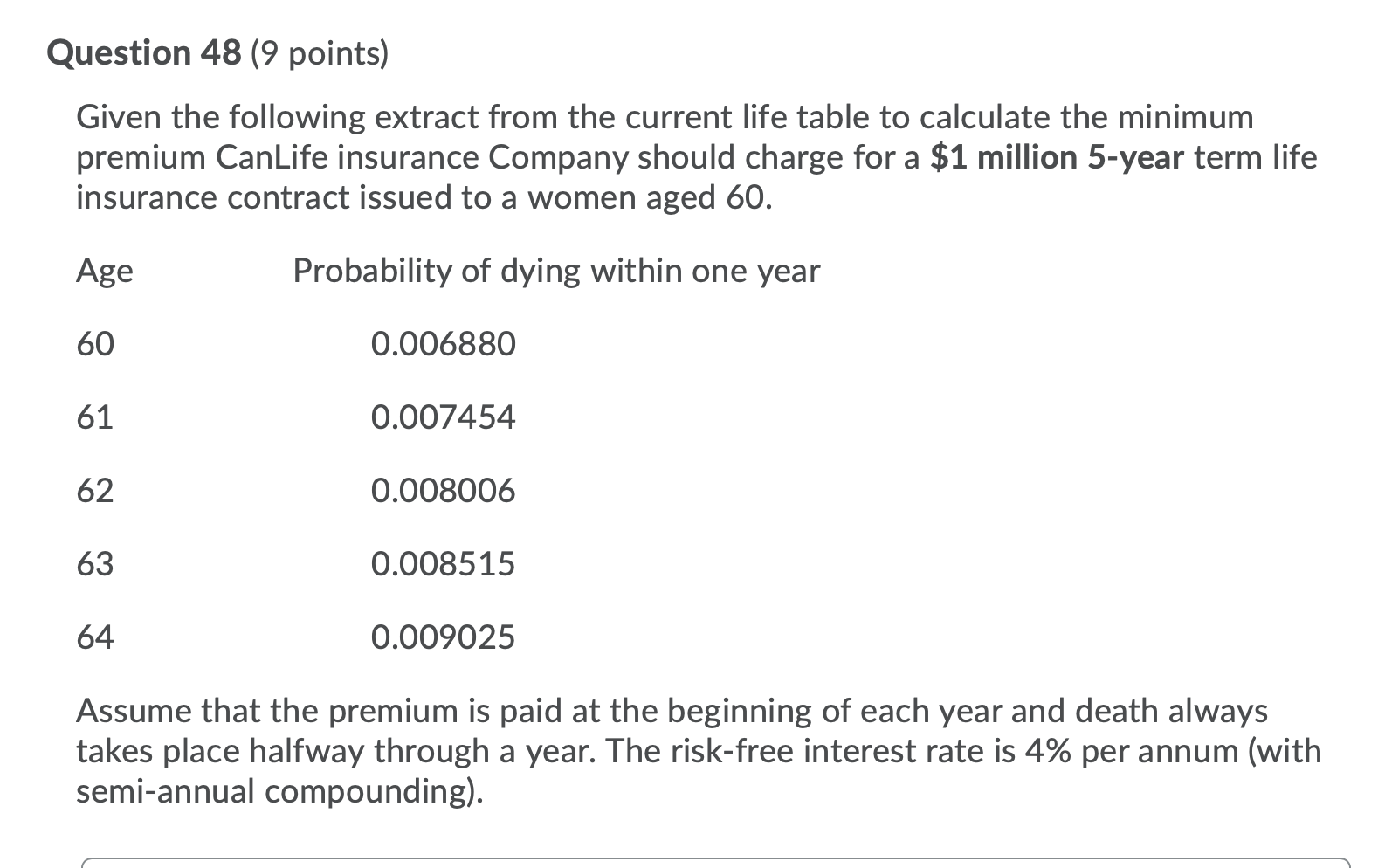

Suppose that we back-test a VaR model using 1,300 days of data. The VaR confidence level is 99% and we observe 15 exceptions. Should we reject the model at the 5% confidence level? Use Kupiec's two-tailed test. Question 48 (9 points) Given the following extract from the current life table to calculate the minimum premium CanLife insurance Company should charge for a $1 million 5-year term life insurance contract issued to a women aged 60. Age Probability of dying within one year 60 0.006880 61 0.007454 62 0.008006 63 0.008515 64 0.009025 Assume that the premium is paid at the beginning of each year and death always takes place halfway through a year. The risk-free interest rate is 4% per annum (with semi-annual compounding). Suppose that we back-test a VaR model using 1,300 days of data. The VaR confidence level is 99% and we observe 15 exceptions. Should we reject the model at the 5% confidence level? Use Kupiec's two-tailed test. Question 48 (9 points) Given the following extract from the current life table to calculate the minimum premium CanLife insurance Company should charge for a $1 million 5-year term life insurance contract issued to a women aged 60. Age Probability of dying within one year 60 0.006880 61 0.007454 62 0.008006 63 0.008515 64 0.009025 Assume that the premium is paid at the beginning of each year and death always takes place halfway through a year. The risk-free interest rate is 4% per annum (with semi-annual compounding)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts