Question: Suppose that we have two standardized inputs X1, X2 and an output Y and we consider regression models of Y on X1 and X2. In

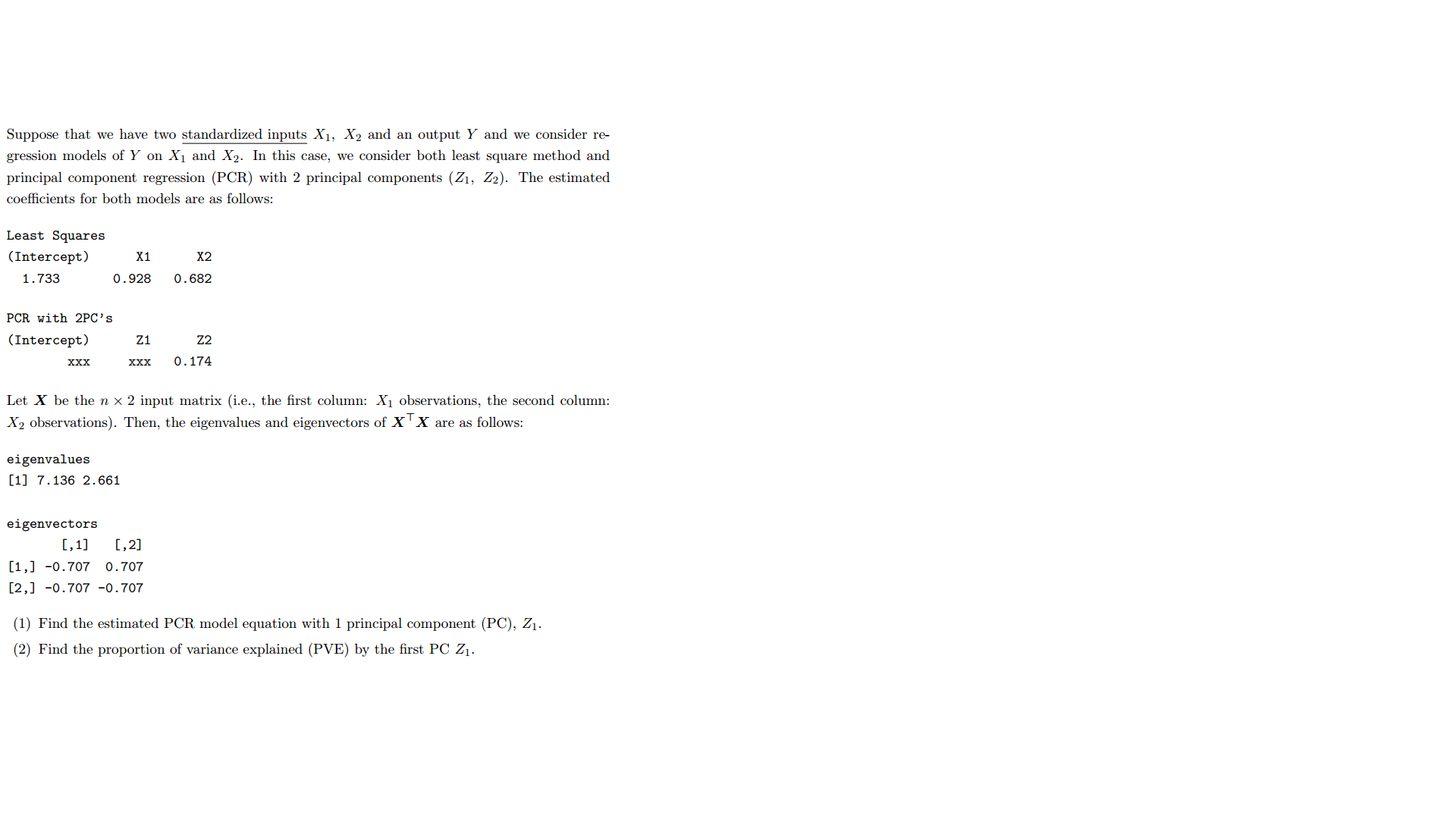

Suppose that we have two standardized inputs X1, X2 and an output Y and we consider regression models of Y on X1 and X2. In this case, we consider both least square method and principal component regression (PCR) with 2 principal components (Z1, Z2). The estimated coefficients for both models are as follows:

Least Squares

(Intercept) X1 X2

1.733 0.928 0.682

PCR with 2PC's

(Intercept) Z1 Z2

xxx xxx 0.174

Let X be the n 2 input matrix (i.e., the first column: X1 observations, the second column: X2 observations). Then, the eigenvalues and eigenvectors of (X^T)X are as follows:

eigenvalues

[1] 7.136 2.661

eigenvectors

[,1] [,2]

[1,] -0.707 0.707

[2,] -0.707 -0.707

(1) Find the estimated PCR model equation with 1 principal component (PC), Z1.

(2) Find the proportion of variance explained (PVE) by the first PC Z1.

Suppose that we have two standardized inputs X1, X2 and an output Y and we consider re- gression models of Y on X1 and X2. In this case, we consider both least square method and principal component regression (PCR) with 2 principal components (Z1, Z2). The estimated coefficients for both models are as follows: Least Squares (Intercept) X1 X2 1.733 0. 928 0. 682 PCR with 2PC's (Intercept) Z1 Z2 XXX XXX 0. 174 Let X be the n x 2 input matrix (i.e., the first column: X1 observations, the second column: X2 observations). Then, the eigenvalues and eigenvectors of X X are as follows: eigenvalues [1] 7. 136 2. 661 eigenvectors [,1] [,2] [1,] -0.707 0.707 [2,] -0.707 -0.707 (1) Find the estimated PCR model equation with 1 principal component (PC), Z1. (2) Find the proportion of variance explained (PVE) by the first PC Z1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts