Suppose that you are holding a stock portfolio that has a current market value of $1,000,000 and

Question:

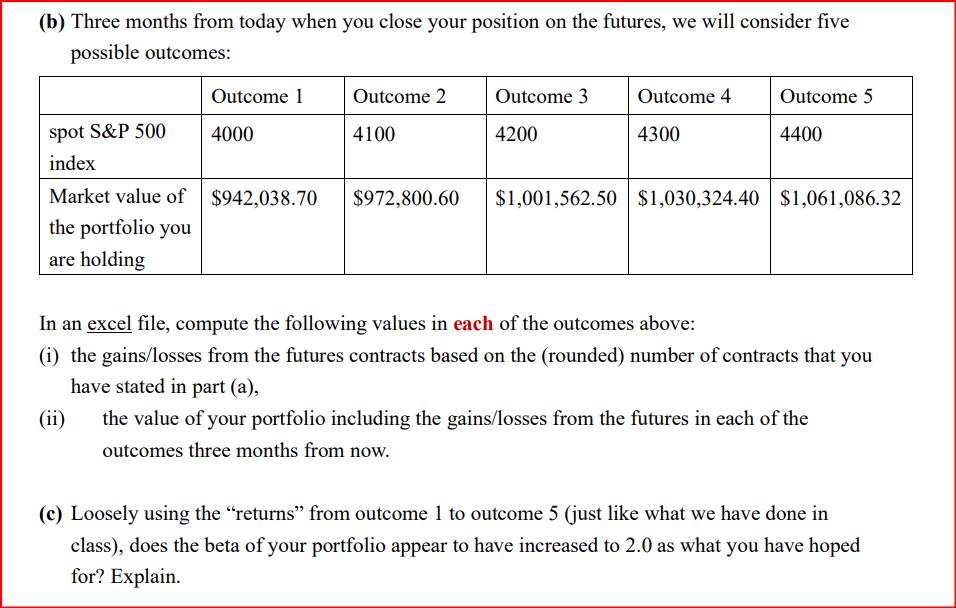

Suppose that you are holding a stock portfolio that has a current market value of $1,000,000 and its beta is 1.25. You expect the general market will go up in the next few months and you try to gain from the bull market by increasing the beta of your portfolio to 2.0 three months from now. You will use the e-mini S&P 500 that expires four months from today to raise the beta of your portfolio. The current spot price of the S&P 500 index is 4200. The annual riskfree interest rate is 5% (cc) and the estimated annual dividend yield of the S&P 500 3 index portfolio is 1%.

(a) Specify clearly how many e-mini S&P 500 index futures you will buy or sell to raise the beta of your portfolio to 2.0 (the number of contracts has to be round to the closest integer).

Expert Answer:

To raise the beta of your portfolio to 20 you need to calculate the number of emini SP 500 index futures contracts you should buy or sell The formula ... View the full answer

Intermediate Financial Management

ISBN: 978-1111530266

11th edition

Authors: Eugene F. Brigham, Phillip R. Daves