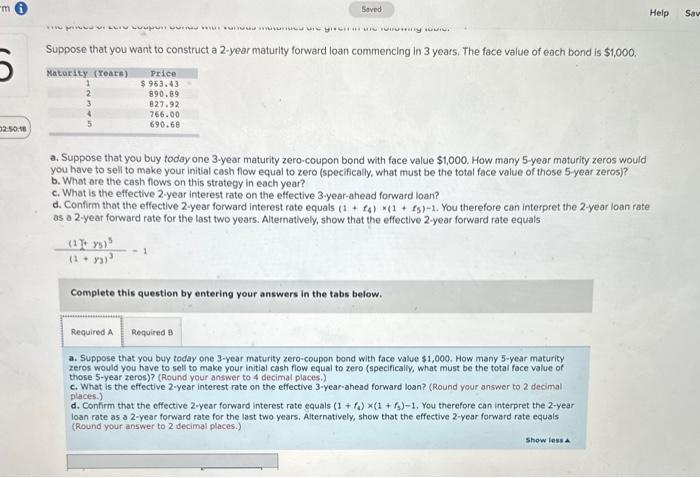

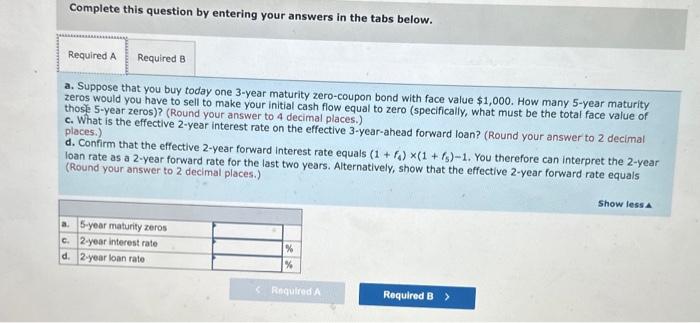

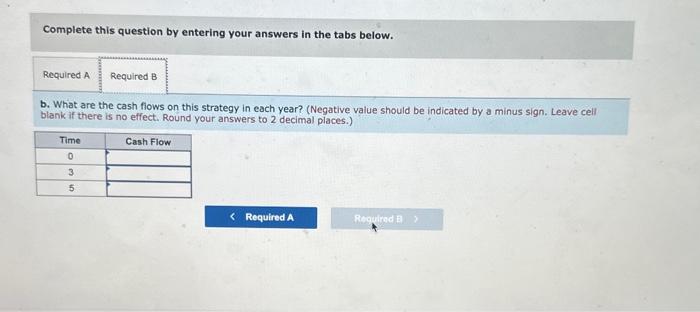

Question: Suppose that you want to construct a 2-year maturity forward loan commencing in 3 years. The face value of each bond is $1,000. a. Suppose

Suppose that you want to construct a 2-year maturity forward loan commencing in 3 years. The face value of each bond is $1,000. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those. 5 -year zeros)? b. What ore the cash flows on this strategy in each year? c. What is the effective 2-year interest rate on the effective 3-year-ahead forward loan? d. Contirm that the effective 2-year forward interest rate equals (1+t4)(1+f5)1. You therefore can interpret the 2-year loan rate as a 2 -year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (1+y)3(1+y5)51 Complete this question by entering your answers in the tabs below. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5-year zeros)? (Round your answer to 4 decimal places.) c. What is the effective 2 -year interest rate on the effective 3 -year-ahead forward loan? (Round your answer to 2 decimal places.) d. Confirm that the effective 2 -year forward interest rate equals (1+f4)(1+f5)1, You therefore can interpret the 2 -year loan rate as a 2 -year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (Round your answer to 2 decimal places.) Complete this question by entering your answers in the tabs below. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5 -year zeros)? (Round your answer to 4 decimal places.) c. What is the effective 2 -year interest rate on the effective 3 -year-ahead forward loan? (Round your answer to 2 decimal d. Confirm that the effective 2 -year forward interest rate equals (1+f4)(1+f5)1. You therefore can interpret the 2 -year Ioan rate as a 2-year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (Round your answer to 2 decimal places.) Complete this question by entering your answers in the tabs below. b. What are the cash fiows on this strategy in each year? (Negative value should be indicated by a minus sign. Leave cell blank if there is no effect. Round your answers to 2 decimal places.) Suppose that you want to construct a 2-year maturity forward loan commencing in 3 years. The face value of each bond is $1,000. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those. 5 -year zeros)? b. What ore the cash flows on this strategy in each year? c. What is the effective 2-year interest rate on the effective 3-year-ahead forward loan? d. Contirm that the effective 2-year forward interest rate equals (1+t4)(1+f5)1. You therefore can interpret the 2-year loan rate as a 2 -year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (1+y)3(1+y5)51 Complete this question by entering your answers in the tabs below. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5-year zeros)? (Round your answer to 4 decimal places.) c. What is the effective 2 -year interest rate on the effective 3 -year-ahead forward loan? (Round your answer to 2 decimal places.) d. Confirm that the effective 2 -year forward interest rate equals (1+f4)(1+f5)1, You therefore can interpret the 2 -year loan rate as a 2 -year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (Round your answer to 2 decimal places.) Complete this question by entering your answers in the tabs below. a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5 -year zeros)? (Round your answer to 4 decimal places.) c. What is the effective 2 -year interest rate on the effective 3 -year-ahead forward loan? (Round your answer to 2 decimal d. Confirm that the effective 2 -year forward interest rate equals (1+f4)(1+f5)1. You therefore can interpret the 2 -year Ioan rate as a 2-year forward rate for the last two years. Alternatively, show that the effective 2 -year forward rate equals (Round your answer to 2 decimal places.) Complete this question by entering your answers in the tabs below. b. What are the cash fiows on this strategy in each year? (Negative value should be indicated by a minus sign. Leave cell blank if there is no effect. Round your answers to 2 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts