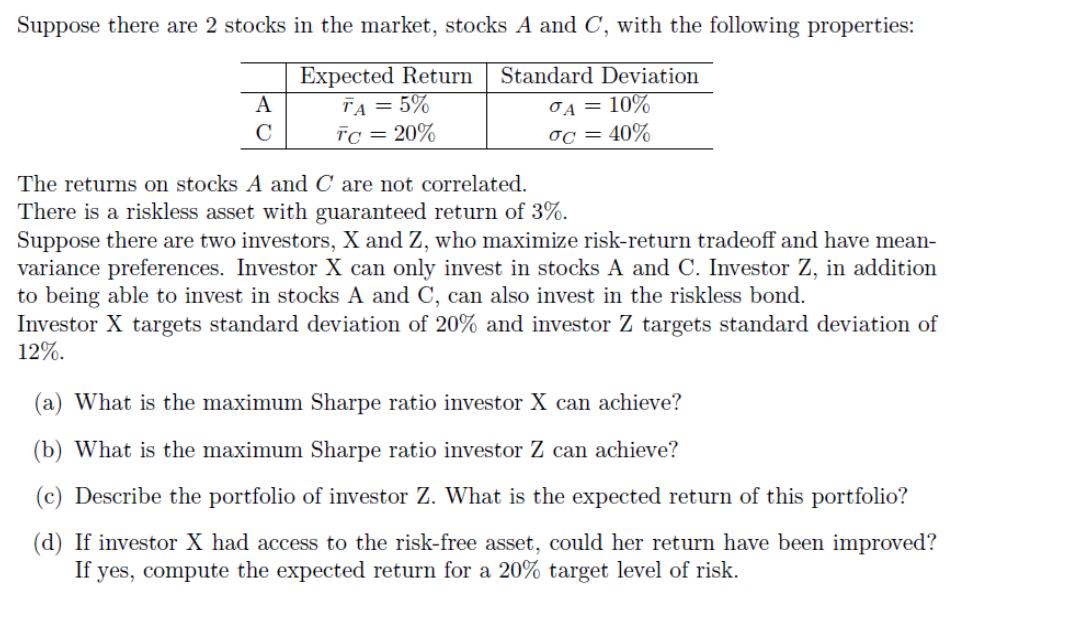

Suppose there are 2 stocks in the market, stocks A and C, with the following properties:...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To calculate the maximum Sharpe ratio for each investor we need to find the optimal portfolios that maximize the riskreturn tradeoff The Sharpe ratio is defined as the ratio of excess return to the st... View the full answer

Related Book For

Quantitative Investment Analysis

ISBN: 978-1119104223

3rd edition

Authors: Richard A. DeFusco, Dennis W. McLeavey, Jerald E. Pinto, David E. Runkle

Posted Date: