Question: Suppose there are three instruments, M, A and B. M is the market portfolio, while A and B are individual stocks. The equilibrium mean vector

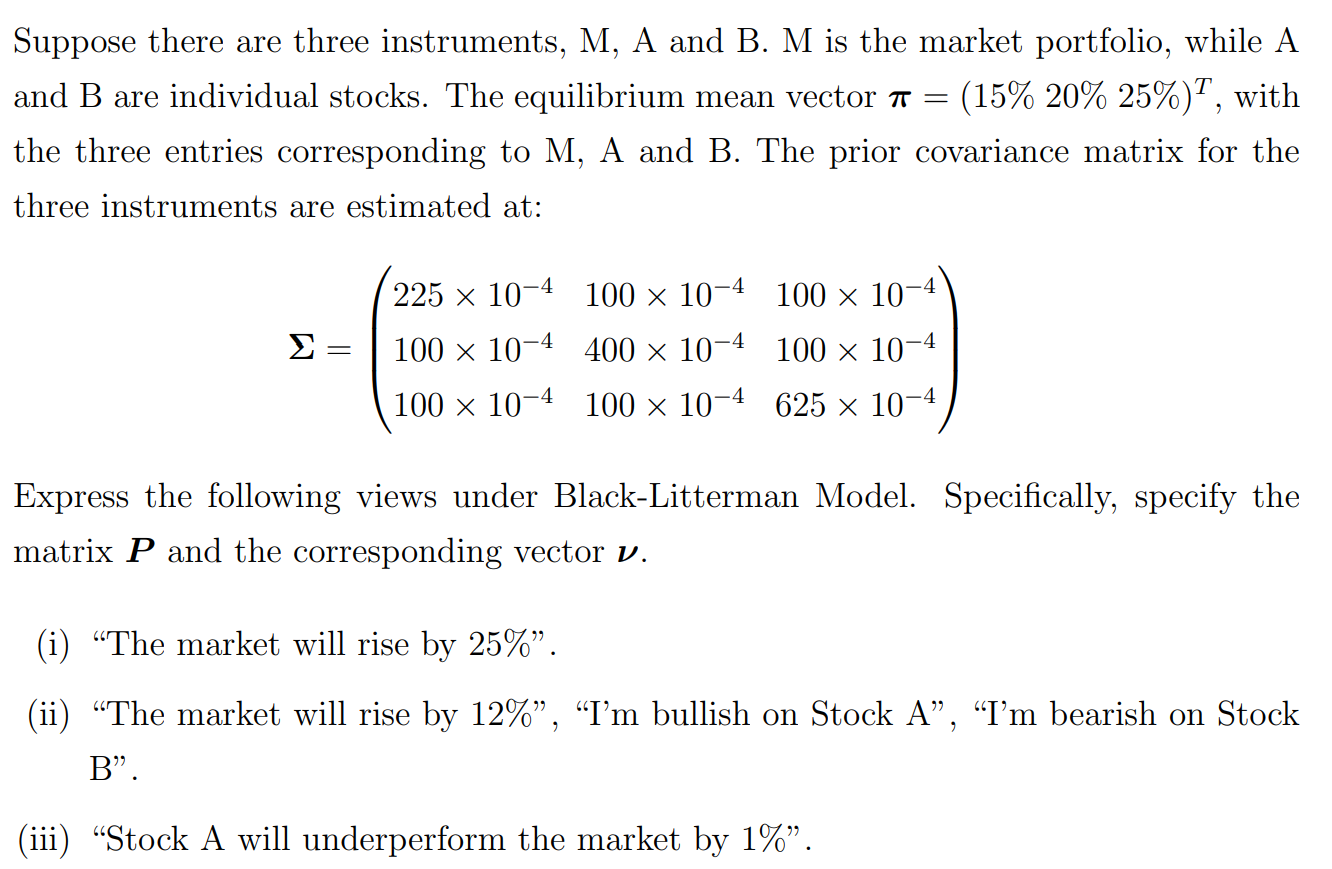

Suppose there are three instruments, M, A and B. M is the market portfolio, while A and B are individual stocks. The equilibrium mean vector a = (15% 20% 25%)", with the three entries corresponding to M, A and B. The prior covariance matrix for the three instruments are estimated at: = 225 x 10-4 100 x 10-4 100 x 10-4 100 x 10-4 400 x 10-4 100 x 10-4 100 x 10-4 100 x 10-4 625 x 10-4 Express the following views under Black-Litterman Model. Specifically, specify the matrix P and the corresponding vector v. (i) The market will rise by 25%. (ii) The market will rise by 12%, I'm bullish on Stock A, I'm bearish on Stock B. (iii) "Stock A will underperform the market by 1%. Suppose there are three instruments, M, A and B. M is the market portfolio, while A and B are individual stocks. The equilibrium mean vector a = (15% 20% 25%)", with the three entries corresponding to M, A and B. The prior covariance matrix for the three instruments are estimated at: = 225 x 10-4 100 x 10-4 100 x 10-4 100 x 10-4 400 x 10-4 100 x 10-4 100 x 10-4 100 x 10-4 625 x 10-4 Express the following views under Black-Litterman Model. Specifically, specify the matrix P and the corresponding vector v. (i) The market will rise by 25%. (ii) The market will rise by 12%, I'm bullish on Stock A, I'm bearish on Stock B. (iii) "Stock A will underperform the market by 1%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts