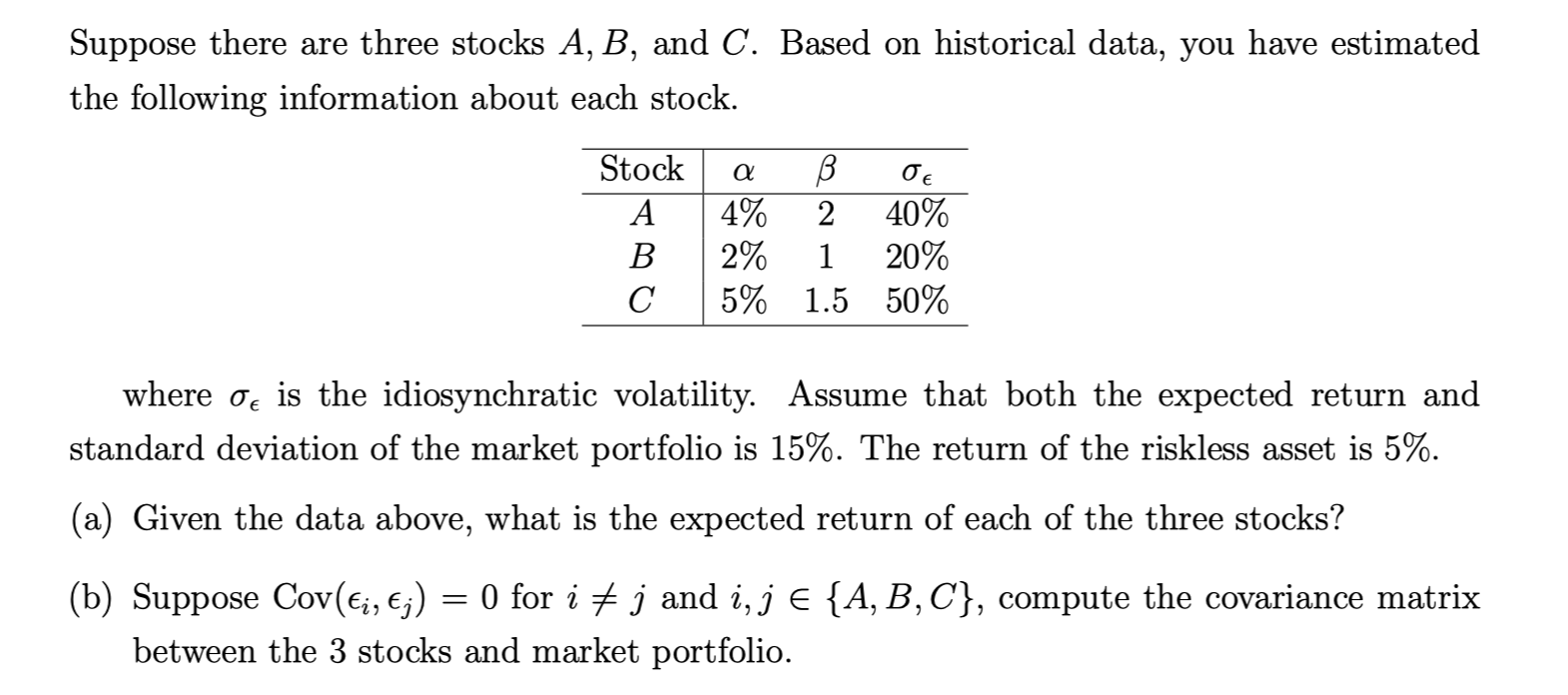

Question: Suppose there are three stocks A, B, and C. Based on historical data, you have estimated the following information about each stock. a Stock A

Suppose there are three stocks A, B, and C. Based on historical data, you have estimated the following information about each stock. a Stock A B 4% 2 40% 2% 1 20% 5% 1.5 50% where oe is the idiosynchratic volatility. Assume that both the expected return and standard deviation of the market portfolio is 15%. The return of the riskless asset is 5%. (a) Given the data above, what is the expected return of each of the three stocks? = (b) Suppose Cov(Ej, ;) O for i # j and i, j E {A, B, C), compute the covariance matrix between the 3 stocks and market portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock