Question: Suppose there are two assets under the single-factor model, the model estimations are shown in the following table. b e 0 Asset 1 Asset 2

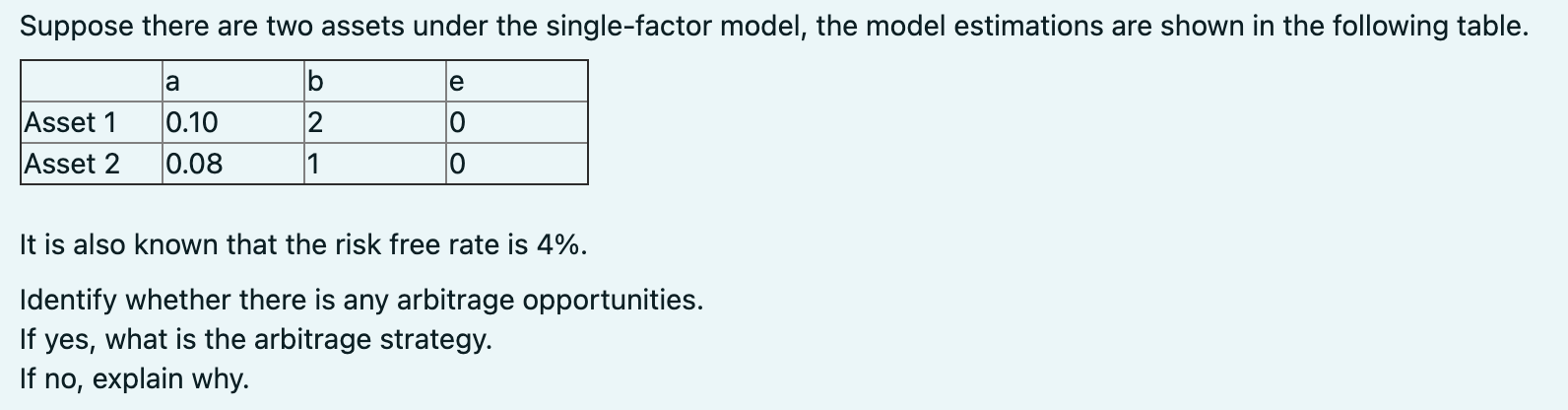

Suppose there are two assets under the single-factor model, the model estimations are shown in the following table. b e 0 Asset 1 Asset 2 0.10 0.08 1 0 It is also known that the risk free rate is 4%. Identify whether there is any arbitrage opportunities. If yes, what is the arbitrage strategy. If no, explain why. Suppose there are two assets under the single-factor model, the model estimations are shown in the following table. b e 0 Asset 1 Asset 2 0.10 0.08 1 0 It is also known that the risk free rate is 4%. Identify whether there is any arbitrage opportunities. If yes, what is the arbitrage strategy. If no, explain why

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock