Question: Suppose there is a second traded option with a Delta of 0.65, a Gamma of 0.4, and a Vega of 0.8. What position in the

Suppose there is a second traded option with a Delta of 0.65, a Gamma of 0.4, and a Vega of 0.8. What position in the traded option and in Minstagram shares would make the portfolio Delta-Gamma-Vega neutral?

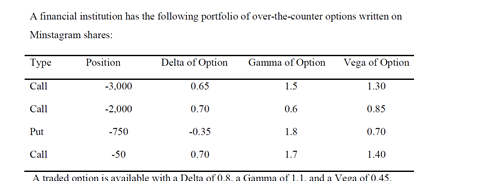

A financial institution has the following portfolio of over-the-counter options written on Minstagram shares: Type Position Delta of Option Gamma of Option Vega of Option Call -3,000 0.65 1.5 1.30 Call -2.000 0.70 0.6 0.85 Put -750 -0.35 1.8 0.70 Call -50 0.70 1.7 1.40 A traded option is available with a Delta of 0.8.a Gamma of 1.1. and a Vega of 0.45 A financial institution has the following portfolio of over-the-counter options written on Minstagram shares: Type Position Delta of Option Gamma of Option Vega of Option Call -3,000 0.65 1.5 1.30 Call -2.000 0.70 0.6 0.85 Put -750 -0.35 1.8 0.70 Call -50 0.70 1.7 1.40 A traded option is available with a Delta of 0.8.a Gamma of 1.1. and a Vega of 0.45

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts