Suppose you are forming a portfolio with Company A and Company B, which have expected returns and

Question:

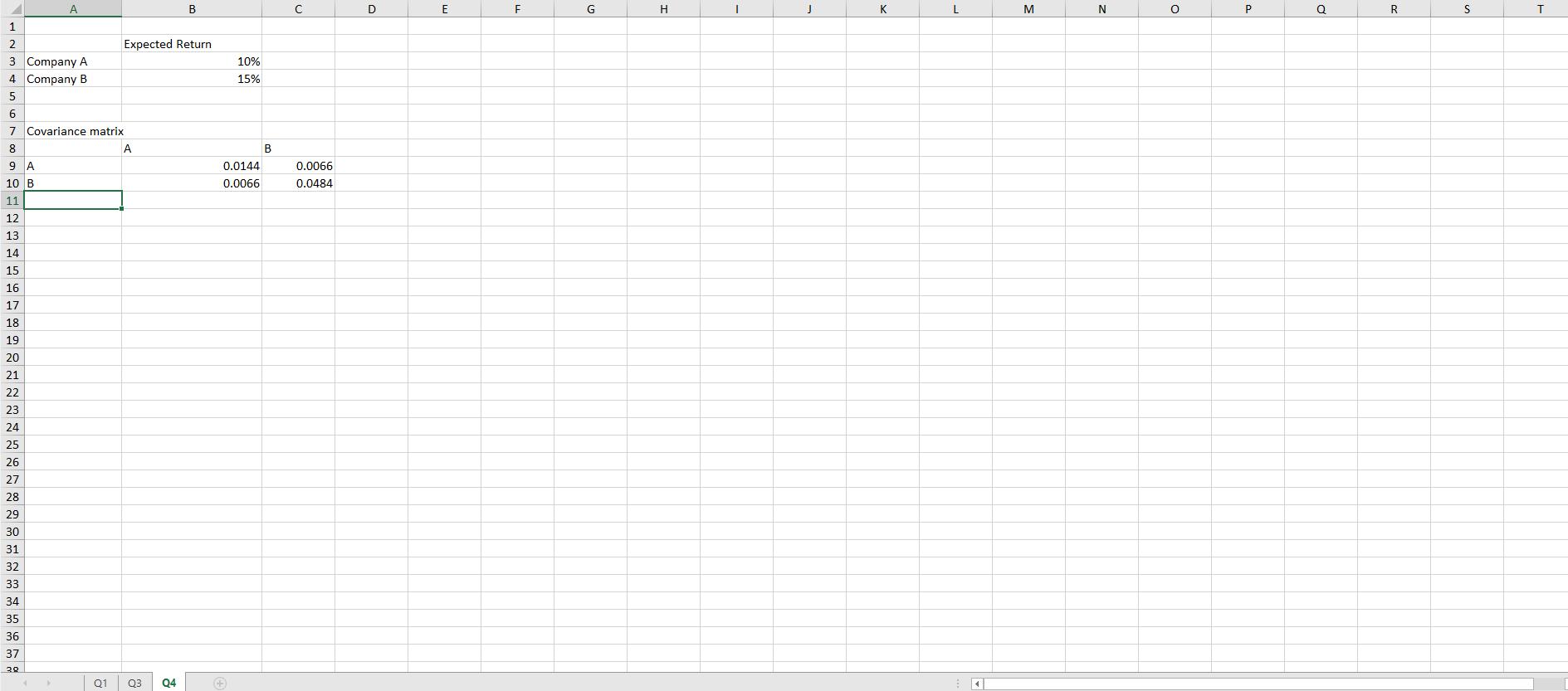

Suppose you are forming a portfolio with Company A and Company B, which have expected returns and covariance matrix as in “Q4” tab of hw2.xls.

a. Construct portfolios consisting of the two stocks with a wide range of portfolio weights (e.g., 10%:90%, 20%:80%, etc.) Plot the portfolios on a chart with expected return on the y-axis and volatility on the x-axis.

b. What are the portfolio weights of your minimum-variance portfolio?

c. What range of portfolio weights produces inefficient portfolios?

d. Now, suppose you can save/borrow at the risk-free rate of 3%. What is the expected return and volatility of the tangent portfolio, and what are its portfolio weights?

Expert Answer:

a Constructing Portfolios and Plotting Chart Expected returns and volatilities for several p... View the full answer

Foundations of Finance The Logic and Practice of Financial Management

ISBN: 978-0132994873

8th edition

Authors: Arthur J. Keown, John D. Martin, J. William Petty