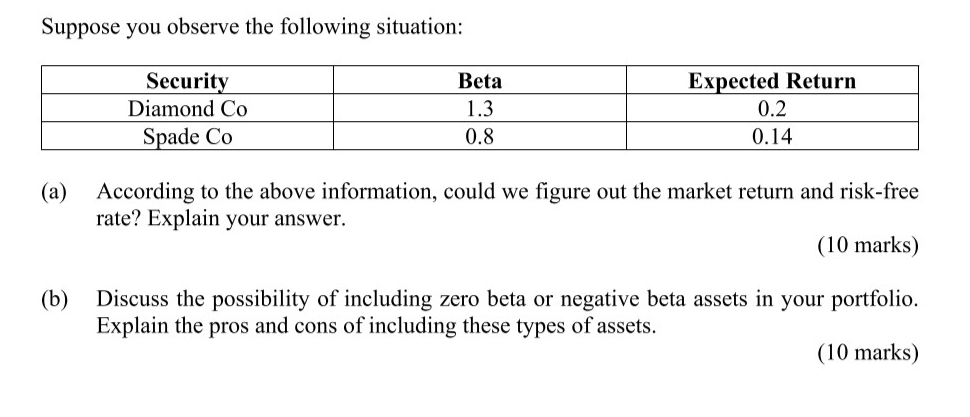

Question: Suppose you observe the following situation: Security Beta Expected Return Diamond Co 1.3 0.2 Spade Co 0.8 0.14 (:1) According to the aboVe information. could

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock