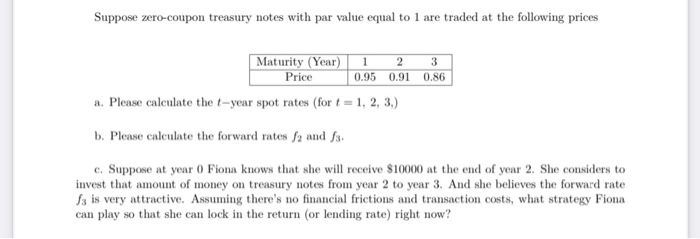

Question: Suppose zero-coupon treasury notes with par value equal to 1 are traded at the following prices 1 Maturity (Year) 2 3 Price 0.95 0.91 0.86

Suppose zero-coupon treasury notes with par value equal to 1 are traded at the following prices 1 Maturity (Year) 2 3 Price 0.95 0.91 0.86 a. Please calculate the t-year spot rates (for t = 1, 2, 3.) b. Please calculate the forward rates / and fs. c. Suppose at year 0 Fiona knows that she will receive $10000 at the end of year 2. She considers to invest that amount of money on treasury notes from year 2 to year 3. And she believes the forward rate 13 is very attractive. Assuming there's no financial frictions and transaction costs, what strategy Fiona can play so that she can lock in the return (or lending rate) right now

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts