SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

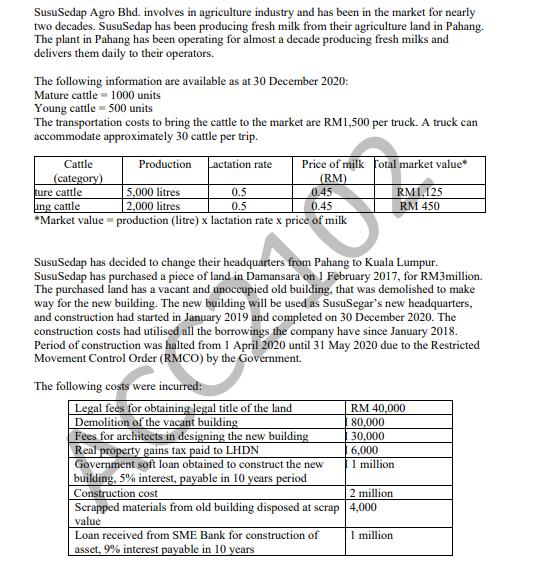

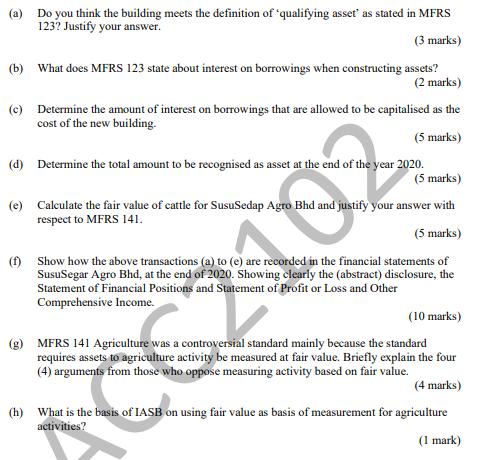

SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark) SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark) SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark) SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark) SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark) SusuSedap Agro Bhd. involves in agriculture industry and has been in the market for nearly two decades. SusuSedap has been producing fresh milk from their agriculture land in Pahang. The plant in Pahang has been operating for almost a decade producing fresh milks and delivers them daily to their operators. The following information are available as at 30 December 2020: Mature cattle - 1000 units Young cattle = 500 units The transportation costs to bring the cattle to the market are RM1,500 per truck. A truck can accommodate approximately 30 cattle per trip. Cattle (category) ture cattle ing cattle *Market value = production (litre) x lactation rate x price of milk Lactation rate Price of milk fotal market value (RM) 0.45 0.45 Production 5,000 litres 2,000 litres 0.5 RM1,125 RM 450 0.5 SusuSedap has decided to change their headquarters from Pahang to Kuala Lumpur. SusuSedap has purchased a piece of land in Damansara on 1 February 2017, for RM3million. The purchased land has a vacant and unoccupied old building, that was demolished to make way for the new building. The new building will be used as SusuSegar's new headquarters, and construction had started in January 20119 and completed on 30 December 2020. The construction costs had utilised all the borrowings the company have since January 2018. Period of construction was halted from 1 April 2020 until 31 May 2020 due to the Restricted Movement Control Order (RMCO) by the Government. The following costs were incurred: Legal fees for obtaining legal title of the land Demolition of the vacant building Fees for architects in designing the new building Real property gains tax paid to LHDN Government soft loan obtained to construct the new building, 5% interest, payable in 10 years period Construction cost Scrapped materials from old building disposed at scrap 4,000 RM 40,000 80,000 30,000 6,000 11 million 2 million value Loan received from SME Bank for construction of I million asset, 9% interest payable in 10 years (a) Do you think the building meets the definition of "qualifying asset as stated in MFRS 123? Justify your answer. (3 marks) (b) What does MFRS 123 state about interest on borrowings when constructing assets? (2 marks) (c) Determine the amount of interest on borrowings that are allowed to be capitalised as the cost of the new building. (5 marks) (d) Determine the total amount to be recognised as asset at the end of the year 2020. (5 marks) (e) Calculate the fair value of cattle for SusuSedap Agro Bhd and justify your answer with respect to MFRS 141. 102 (5 marks) (f) Show how the above transactions (a) to (e) are recorded in the financial statements of SusuSegar Agro Bhd, at the end of 2020. Showing clearly the (abstract) disclosure, the Statement of Financial Positions and Statement of Profit or Loss and Other Comprehensive Income. (10 marks) (g) MFRS 141 Agriculture was a controversial standard mainly because the standard requires assets to agriculture activity be measured at fair value. Briefly explain the four (4) arguments from those who oppose measuring activity based on fair value. (4 marks) (h) What is the basis of IASB on using fair value as basis of measurement for agriculture activities? (1 mark)

Expert Answer:

Related Book For

Statistics for Management and Economics Abbreviated

ISBN: 978-1285869643

10th Edition

Authors: Gerald Keller

Posted Date:

Students also viewed these accounting questions

-

Choose a product that has been on the market for a few years and describe how the product has evolved throughout its lifecycle. Describe the basic product in the introductory stage of the lifecycle....

-

Home blood-pressure monitors have been on the market for several years. This device allows people with high blood pressure to measure their own and determine whether additional medication is...

-

Problem 4 1. Fig. 2 is a solution of differential equation orde-2 with the initial condition y(0) = 1 and y (0) = 0. 0.5 1.5 2.5 3. 3.5 y(t) w(t) = e z(t) = -et 4 4.5 1 5.5 6 6.5 7 7.5 8 8.5 9 Fig.2...

-

Ruff, Tuff, and Duff are parners sharing profits and losses 30/30/40 respectively. Their balance sheet is below: Cash Receivable from Ruff Property & Equipment $200,000 10,000 500,000 $710,000...

-

Suppose that observations on a stock price (in dollars) at the end of each of 15 consecutive days are as follows: 30.2, 32.0, 31.1, 30.1, 30.2, 30.3, 30.6, 30.9, 30.5, 31.1, 31.3, 30.8, 30.3, 29.9,...

-

Assume that Ann Wood wants her managers and associates to be the foundation for her departments competitive advantages. Use the framework summarized in Exhibit 1-2 in the chapter text to assess the...

-

Create recommendations for an organization that is facing resistance to change from its own HR department. What are some of the likely causes of this resistance? How can they be overcome?

-

This exercise is an extension of Exercise 2-3B. Assume Jon Wallace completed the following additional transactions during March. Show the effect of each transaction on the basic elements of the...

-

If the beginning retained earnings balance is $5,900, net income is $4,000, and ending retained earnings is $6,700, what is the amount of dividends paid?

-

The balance sheets of Forest Company and Garden Company are presented below as at December 31, Year 8. Additional Information Forest acquired 90% of Garden for $207,900 on July 1, Year 1, and...

-

Solve for the unknown number of years in each of the following (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.): $ Present Value Years Interest Rate...

-

Study each of the cases below. Indicate whether the contract is executed, executory, or neither, and whether it is valid, voidable, or void, by placing an X in the space provided. Arslantian, a...

-

The prevailing legal view of a newspaper advertisement. a. acceptance b. counteroffer c. invitation to tra de d. lapse of time e. mailbox r ule f. offeree g. offeror h. public of fer i. request f or...

-

Evidence of ownership provided by a storage facility. a. bill of sale b. certifi cate of title c. condition s ubsequent d. condition pr ecedent e. estoppel f. fungible goods g. order bill of lading...

-

A call for a bid or estimate for materials to be furnished or work to be done. a. acceptance b. counteroffer c. invitation to tra de d. lapse of time e. mailbox r ule f. offeree g. offeror h. public...

-

A contract characterized by unequal bargaining power of the parties. a. contract of adhesion b. duress c. fraud d. intentional c oncealment e. misrepresentation f. mistake g. mutual a greement h....

-

Determine the transfer function from U(s) to Y(s) for the following block diagram. Provided are some recommended steps to take: a. Label each signal (line with arrow) b. Write the equation for each...

-

Planning: Creating an Audience Profile; Collaboration: Team Projects. Compare the Facebook pages of three companies in the same industry. Analyze the content on all available tabs. What can you...

-

Many automotive experts believe that speed limits on highways are too low. One particular expert has stated that he thinks that most drivers drive at speeds that they consider safe. He suggested that...

-

Can we infer from the data that married and never married people differ in their completion of a graduate degree (DEGREE: 4 = Graduate degree, 1-3 = Other)?

-

According to FBI statistics, there were 342,000 robberies in the United States in 2009 (latest statistics available). A random sample of robberies was drawn and the amount of loss was recorded....

-

Demonstrate that for a closed path \(\operatorname{Tr} U_{\gamma}(x, x)\) is gauge invariant, where \(U_{\gamma}\left(x_{0}, x_{1} ight)\) is defined by Eq. (26.9).

-

Use Stokes' theorem [Eq. (27.5)] to prove that Eq. (27.4) leads to Eq. (27.6). Data from Eq. 27.4 Data from Eq. 27.5 Data from Eq. 27.6 = z ) ); A dr. - SA dr) = f A dr.

-

Prove the result of Eq. (26.10) that a path-dependent representation of a gauge group is sensitive to a gauge transformation only at the endpoints of the path.

Study smarter with the SolutionInn App