Question: Sweet Company has the following two temporary differences between its income tax expense and income taxes payable. 2017 2018 2019 Pretax financial income $849.000 $883.000

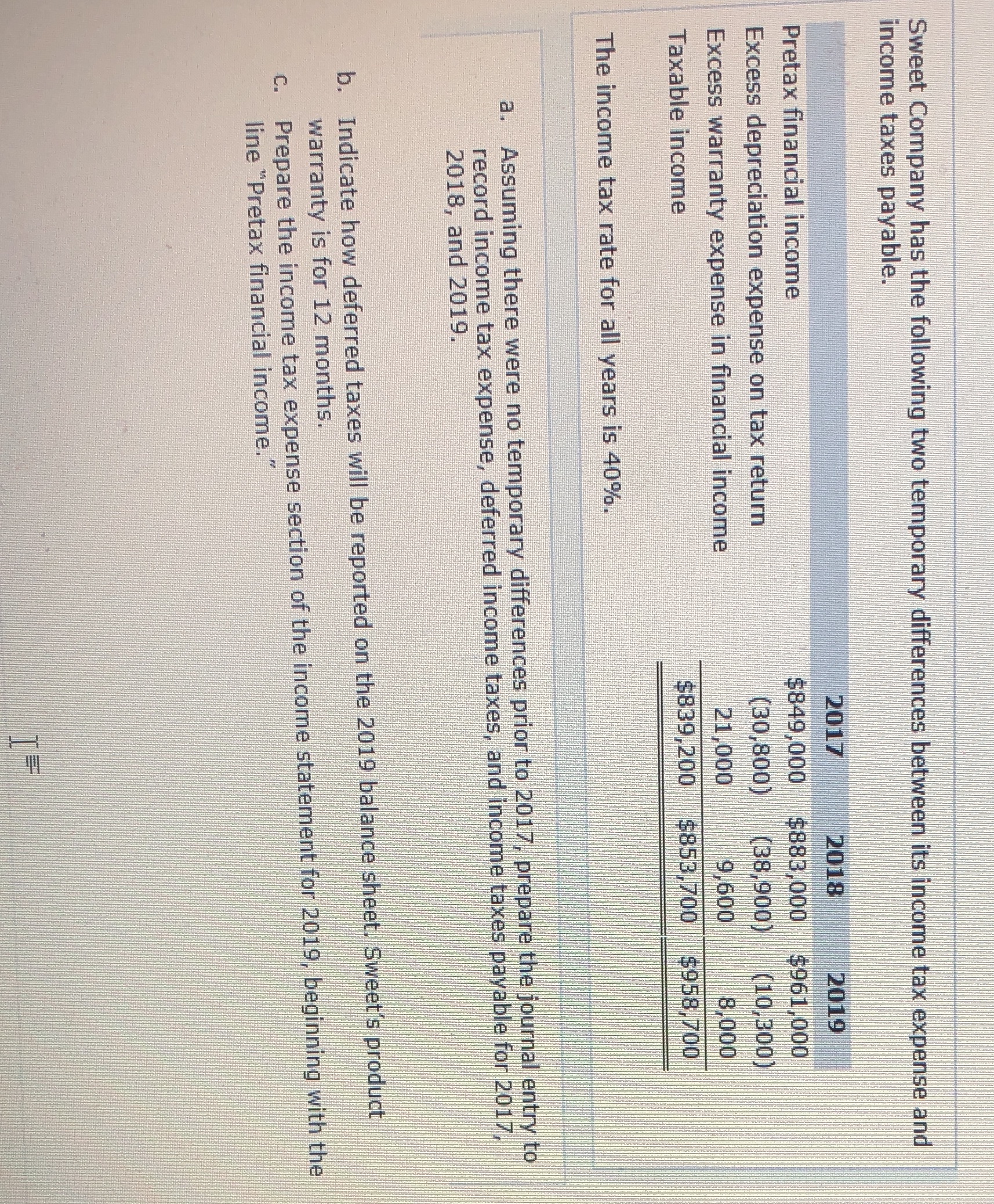

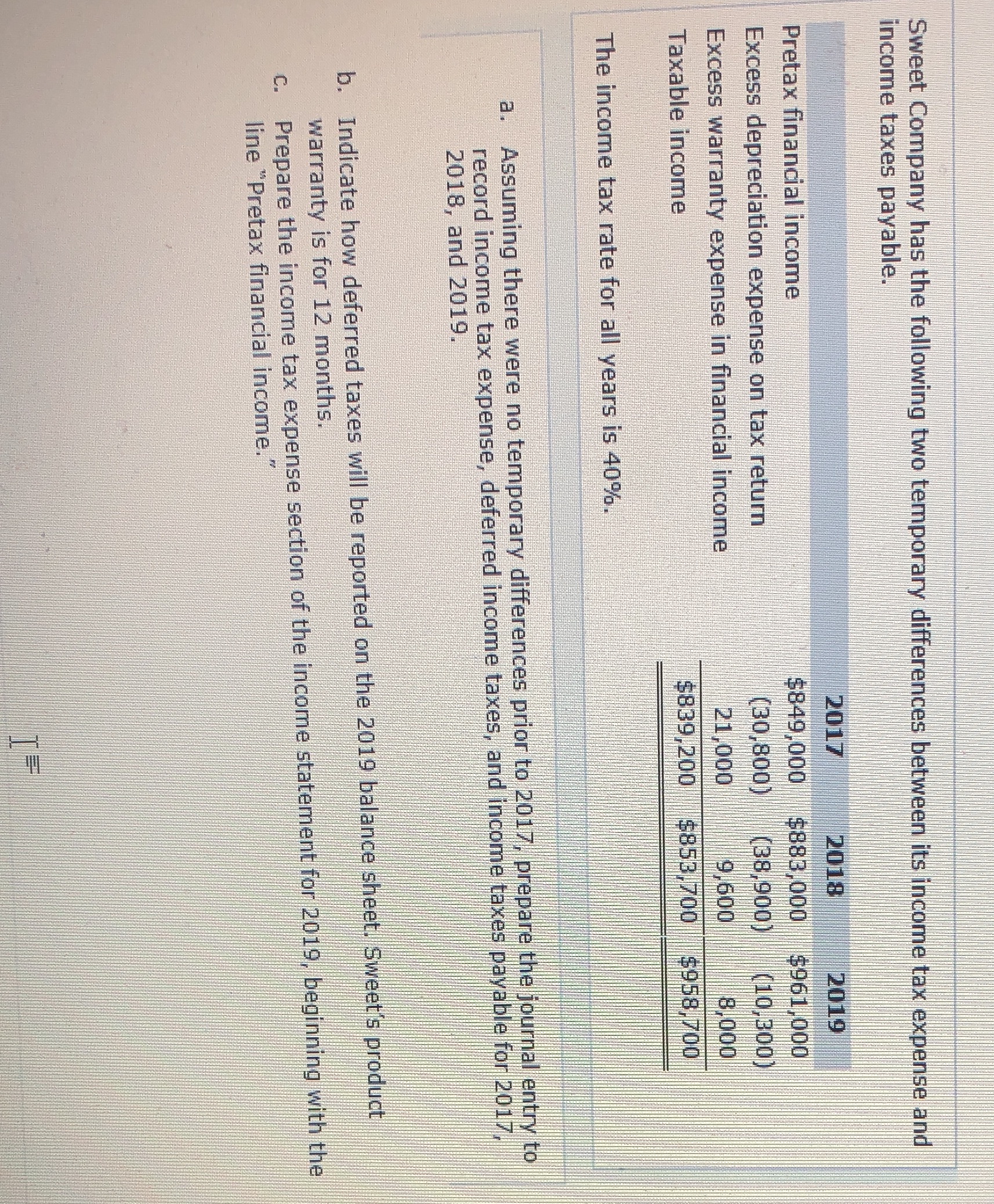

Sweet Company has the following two temporary differences between its income tax expense and income taxes payable. 2017 2018 2019 Pretax financial income $849.000 $883.000 $961.000 Excess depreciation expense on tax return (30.800) (38.900) (10.300) Excess warranty expense in financial income 21,000 9.600 8,000 Taxable income $839,200 $853.700 $958,700 The income tax rate for all years is 40%. a. Assuming there were no temporary differences prior to 2017, prepare the journal entry to record income tax expense, deferred income taxes, and income taxes payable for 2017. 2018, and 2019. b. Indicate how deferred taxes will be reported on the 2019 balance sheet. Sweet's product warranty is for 12 months. Prepare the income tax expense section of the income statement for 2019, beginning with the line "Pretax financial income."

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts