Sylvie Lafountaine, a Canadian resident, owns all of the issued and outstanding shares of Lafountaine Cuisine Inc.

Question:

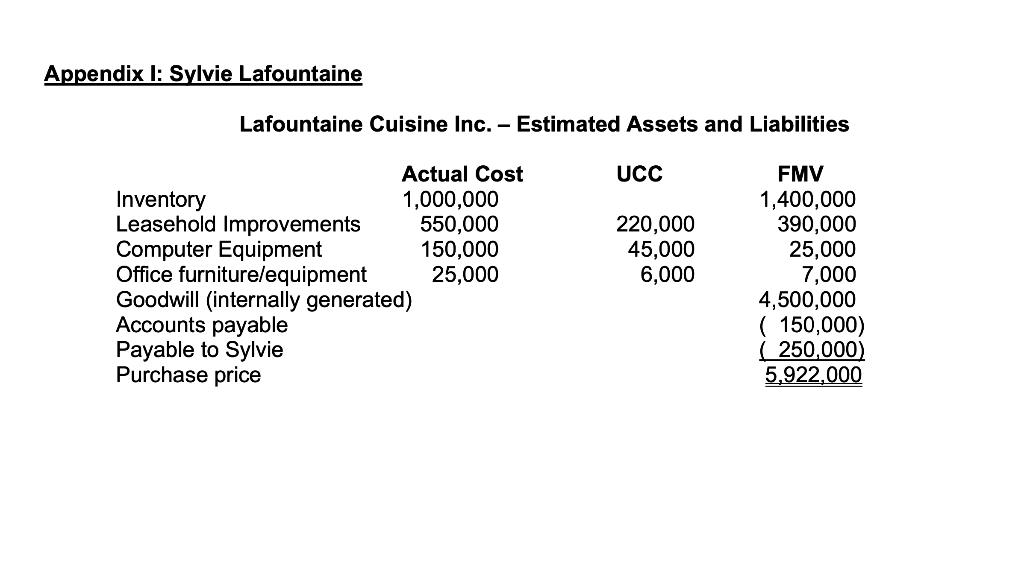

Sylvie Lafountaine, a Canadian resident, owns all of the issued and outstanding shares of Lafountaine Cuisine Inc. (“Cuisine”), which is an importer and wholesaler of French specialty foodstuffs, cooking equipment and utensils and the like. Cuisine also sells to the general public on-line. The business has thrived over the course of the pandemic as a result of renewed interest in cooking with so many staying at home. It has not been overly affected by supply chain issues. The company, which was founded by Sylvie’s father, operates out of a leased warehouse in Toronto. There are 100 common shares outstanding with a total paid-up capital of $100 ($1 per share). Sylvie’s adjusted cost base of the shares is $200,000 in total, which was the fair market value of the shares when she inherited them from her father many years ago. Sylvie has decided it is time to retire. Sylvie has no children, none of her family have any interest in taking over the business and, frankly, she is exhausted from the demands of running a business during the pandemic. She is therefore considering selling the company. She is aware that she could sell assets or shares. Sylvie has estimated the value of Cuisine’s assets at $6,322,000. On the assumption that the purchaser would assume the liabilities of Cuisine, the company would receive $5,922,000 on an asset sale. If the assets are sold, Cuisine will pay its corporate taxes and invest the after-tax proceeds in marketable securities. Cuisine has a December 31 year-end for tax purposes. Sylvie anticipates a sale would take place on December 31, 2021. Sylvie has provided projected financial information on the assets and liabilities of the company (see Appendix I). The cost and UCC amounts are based on Cuisine’s projected December 31, 2021 information. It is projected that Cuisine’s 2021 taxable income, excluding the income/taxable capital gains generated from the asset sale, will be approximately $350,000 before CCA. Assume that this $350,000 taxable income figure is computed correctly and all of it will be eligible for the small business deduction. Sylvie does not currently own shares of any other private corporations. Sylvie wants to know how much money Cuisine will have to invest from the sale if the assets are sold. She would also like to know how much she could take out of the company as capital dividends and as eligible dividends. Per CRA, Cuisine has no general rate income pool (GRIP) or capital dividend account (CDA) or eligible or non- eligible refundable dividend on hand (ERDTOH or NERDTOH) accounts as at December 31, 2020. Sy/vie is willing to accept an asset sale at the values in Appendix I. However, as Cuisine is a qualified small business corporation (“QSBC”) and Sylvie has used only $100,000 of her lifetime QSBC capital gains exemption entitlement, she would like to sell shares, if possible, to get her “free” capital gain. She knows that she will receive a lower price for a share sale than for an asset sale. Sylvie thinks she might be able to sell the shares for $5,300,000. She would like to know if she would be better off selling the shares for $5,300,000 rather than selling the net assets for $5,922,000. Assume the combined federal/provincial corporate tax rate is 13% for active business income eligible for the small business deduction, 25% on active income not eligible for the small business deduction and 50.67% on investment income. Also, you can assume that the top combined federal/provincial personal marginal rate is 50% and that Sylvie has sufficient other income to be in the top bracket. Also assume that the combined federal/provincial dividend tax credit is equal to the gross-up.

Expert Answer:

Answer If Sylvie chooses to sell the assets of Lafountaine Cuisine Inc the company will receive 5922000 on the asset sale After paying taxes and assum... View the full answer