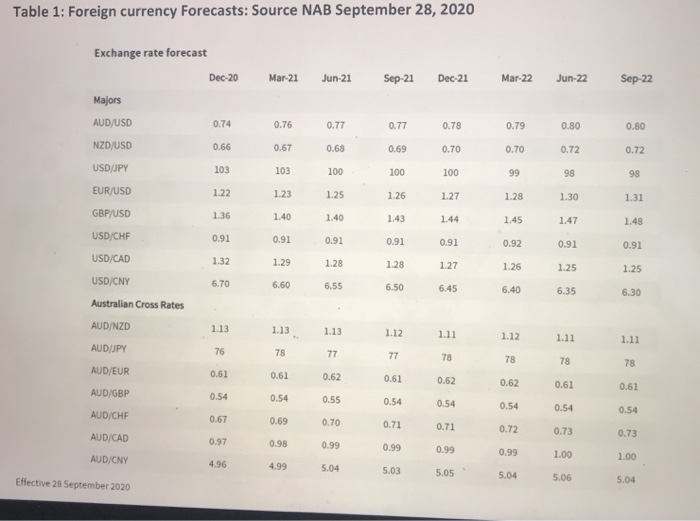

Question: Table 1: Foreign currency Forecasts: Source NAB September 28, 2020 Mar-21 Jun-21 Sep-21 Dec-21 Exchange rate forecast Dec-20 Majors AUD/USD Mar 22 Jun-22 Sep-22 0.74

Table 1: Foreign currency Forecasts: Source NAB September 28, 2020 Mar-21 Jun-21 Sep-21 Dec-21 Exchange rate forecast Dec-20 Majors AUD/USD Mar 22 Jun-22 Sep-22 0.74 0.76 0.77 0.77 0.78 0.79 0.80 0.80 NZD/USD 0.66 0.67 0.68 0.69 0.70 0.70 0.72 0.72 USD/JPY 103 103 100 100 100 99 98 98 EUR/USD 1.22 1.23 1.25 1.26 1.27 1.28 1.30 1.31 GBP/USD 1.36 1.40 1.40 1.43 1.44 1.45 1.47 1.48 USD/CHF 0.91 0.91 0.91 0.91 0.91 0.92 0.91 0.91 USD/CAD 1.32 1.29 1.28 1.28 1.27 1.26 1.25 1.25 USD/CNY 6.70 6.60 6.55 6.50 6.45 6.40 6.35 6.30 Australian Cross Rates AUD/NZD 1.13 1.13 1.13 1.12 1.11 1.12 1.11 1.11 AUD JPY 76 78 77 77 78 78 78 78 AUD/EUR 0.61 0.61 0.62 0.61 0.62 0.62 0.61 0.61 AUD/GBP 0.54 0.54 0.55 0.54 0.54 0.54 0.54 AUD/CHF 0.54 0.67 0.69 0.70 0.71 0.71 0.72 0.73 AUD/CAD 0.73 0.97 0.98 0.99 0.99 0.99 0.99 1.00 AUD/CNY 1.00 4.96 4.99 5.04 5.03 5.05 5.04 Effective 28 September 2020 5.06 5.04 Question 2 (20 marks) You are a CFO of an Australian company with a liability of USD 1 million due in December 2021. You have receivables of 10 million Japanese yen due in December 2021. Assuming that the forecasts given in table 1 are accurate and using the forward rates for AUD/USD and AUD/JPY, does it make sense to hedge a) your payable in USD; b) your receivable in JPY? Illustrate with data obtained from internet sources / IRESS trading room. You may use forwards/futures/options on the relevant currency pairs (if available). (20 marks) Table 1: Foreign currency Forecasts: Source NAB September 28, 2020 Mar-21 Jun-21 Sep-21 Dec-21 Exchange rate forecast Dec-20 Majors AUD/USD Mar 22 Jun-22 Sep-22 0.74 0.76 0.77 0.77 0.78 0.79 0.80 0.80 NZD/USD 0.66 0.67 0.68 0.69 0.70 0.70 0.72 0.72 USD/JPY 103 103 100 100 100 99 98 98 EUR/USD 1.22 1.23 1.25 1.26 1.27 1.28 1.30 1.31 GBP/USD 1.36 1.40 1.40 1.43 1.44 1.45 1.47 1.48 USD/CHF 0.91 0.91 0.91 0.91 0.91 0.92 0.91 0.91 USD/CAD 1.32 1.29 1.28 1.28 1.27 1.26 1.25 1.25 USD/CNY 6.70 6.60 6.55 6.50 6.45 6.40 6.35 6.30 Australian Cross Rates AUD/NZD 1.13 1.13 1.13 1.12 1.11 1.12 1.11 1.11 AUD JPY 76 78 77 77 78 78 78 78 AUD/EUR 0.61 0.61 0.62 0.61 0.62 0.62 0.61 0.61 AUD/GBP 0.54 0.54 0.55 0.54 0.54 0.54 0.54 AUD/CHF 0.54 0.67 0.69 0.70 0.71 0.71 0.72 0.73 AUD/CAD 0.73 0.97 0.98 0.99 0.99 0.99 0.99 1.00 AUD/CNY 1.00 4.96 4.99 5.04 5.03 5.05 5.04 Effective 28 September 2020 5.06 5.04 Question 2 (20 marks) You are a CFO of an Australian company with a liability of USD 1 million due in December 2021. You have receivables of 10 million Japanese yen due in December 2021. Assuming that the forecasts given in table 1 are accurate and using the forward rates for AUD/USD and AUD/JPY, does it make sense to hedge a) your payable in USD; b) your receivable in JPY? Illustrate with data obtained from internet sources / IRESS trading room. You may use forwards/futures/options on the relevant currency pairs (if available). (20 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts