Question: Table 1: Stock price data for Problem 5.4. Index 11 Index 1 2 3 4 5 6 7 8 9 ST 53.58 52.80 54.92 55.84

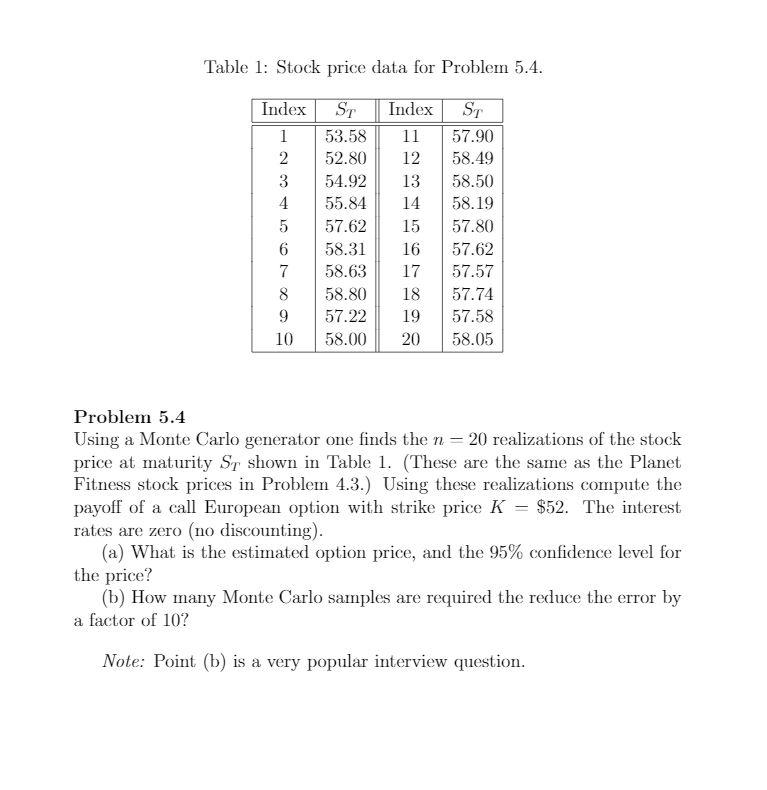

Table 1: Stock price data for Problem 5.4. Index 11 Index 1 2 3 4 5 6 7 8 9 ST 53.58 52.80 54.92 55.84 57.62 58.31 58.63 58.80 57.22 58.00 12 13 14 15 16 17 18 19 ST 57.90 58.49 58.50 58.19 57.80 57.62 57.57 57.74 57.58 58.05 10 20 Problem 5.4 Using a Monte Carlo generator one finds the n = 20 realizations of the stock price at maturity Sy shown in Table 1. (These are the same as the Planet Fitness stock prices in Problem 4.3.) Using these realizations compute the payoff of a call European option with strike price K = $52. The interest rates are zero (no discounting). (a) What is the estimated option price, and the 95% confidence level for the price? (b) How many Monte Carlo samples are required the reduce the error by a factor of 10? Note: Point (b) is a very popular interview question. Table 1: Stock price data for Problem 5.4. Index 11 Index 1 2 3 4 5 6 7 8 9 ST 53.58 52.80 54.92 55.84 57.62 58.31 58.63 58.80 57.22 58.00 12 13 14 15 16 17 18 19 ST 57.90 58.49 58.50 58.19 57.80 57.62 57.57 57.74 57.58 58.05 10 20 Problem 5.4 Using a Monte Carlo generator one finds the n = 20 realizations of the stock price at maturity Sy shown in Table 1. (These are the same as the Planet Fitness stock prices in Problem 4.3.) Using these realizations compute the payoff of a call European option with strike price K = $52. The interest rates are zero (no discounting). (a) What is the estimated option price, and the 95% confidence level for the price? (b) How many Monte Carlo samples are required the reduce the error by a factor of 10? Note: Point (b) is a very popular interview

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts