Question: Table 2 below shows a risk budget report for an equally weighted portfolio of vfinx, vpacx and vbltx. The risk budget report shows the additive

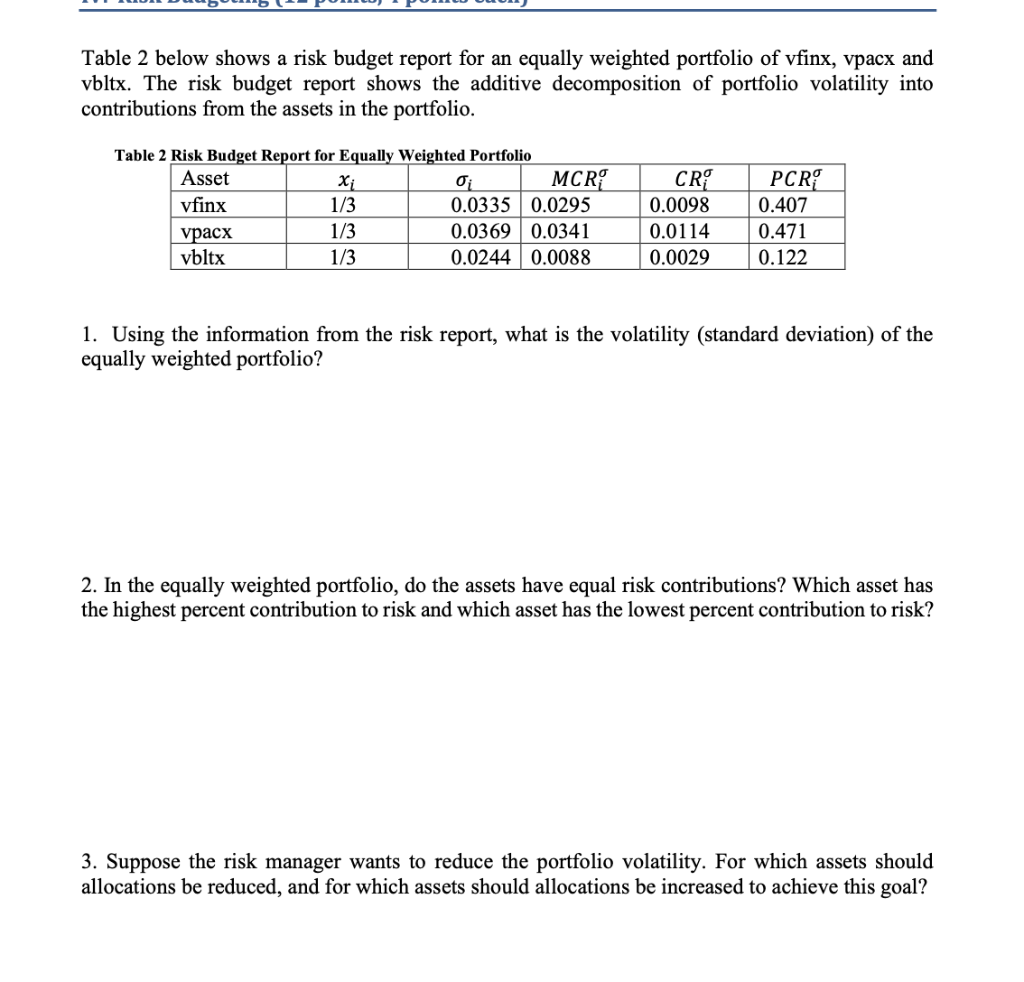

Table 2 below shows a risk budget report for an equally weighted portfolio of vfinx, vpacx and vbltx. The risk budget report shows the additive decomposition of portfolio volatility into contributions from the assets in the portfolio. 1. Using the information from the risk report, what is the volatility (standard deviation) of the equally weighted portfolio? 2. In the equally weighted portfolio, do the assets have equal risk contributions? Which asset has the highest percent contribution to risk and which asset has the lowest percent contribution to risk? 3. Suppose the risk manager wants to reduce the portfolio volatility. For which assets should allocations be reduced, and for which assets should allocations be increased to achieve this goal

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts