Question: Task One Equilibrium for an economy occurs where the quantity of aggregate output demanded is equal to the quantity of output supplied. In the short

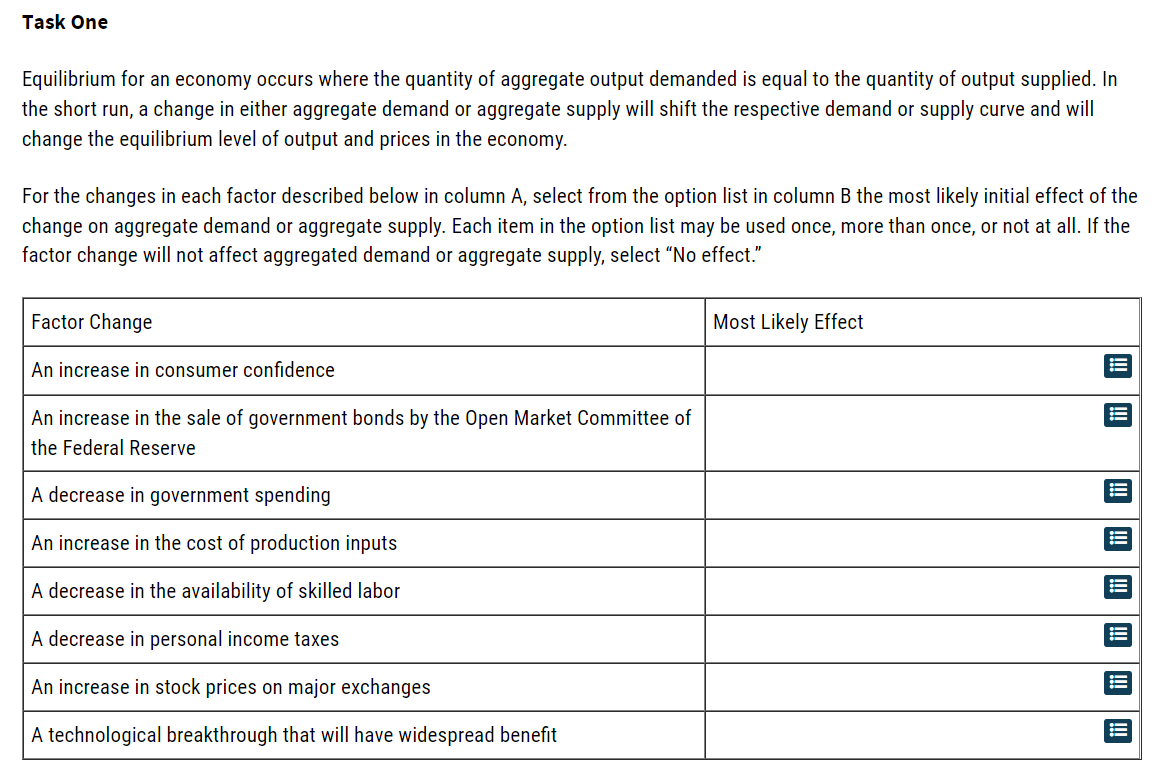

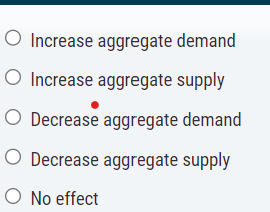

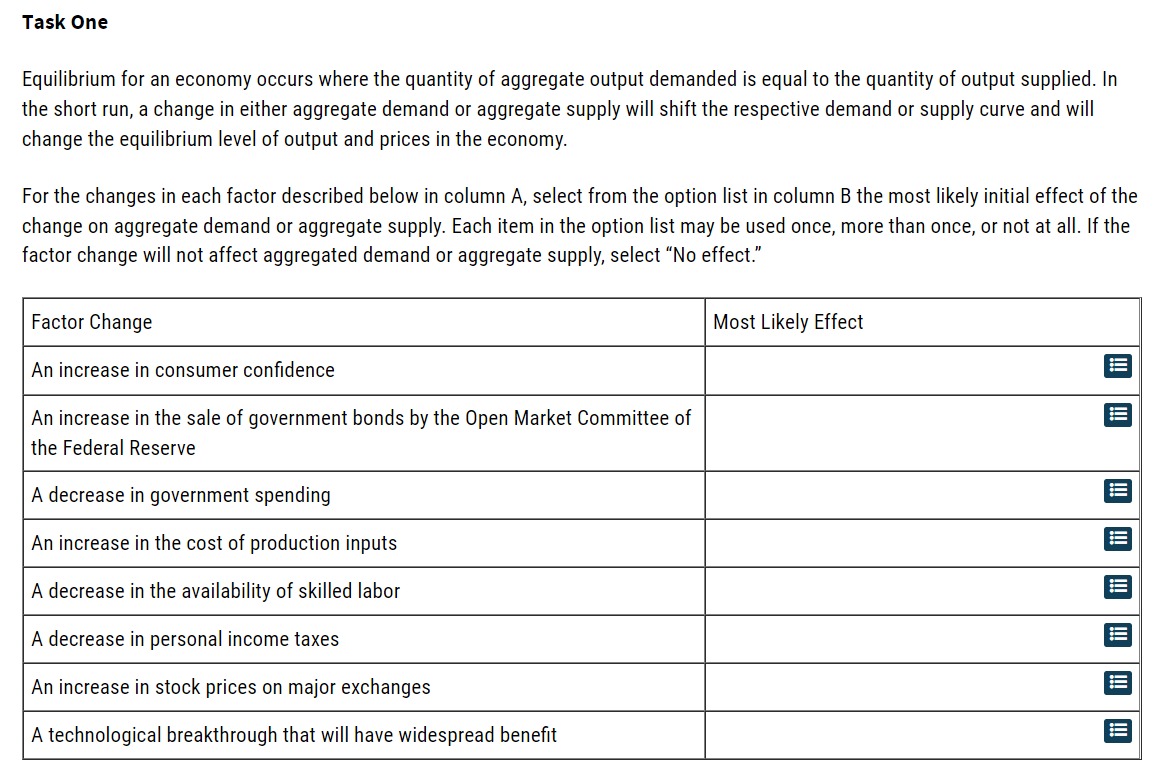

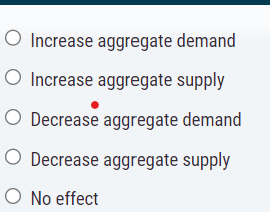

Task One Equilibrium for an economy occurs where the quantity of aggregate output demanded is equal to the quantity of output supplied. In the short run, a change in either aggregate demand or aggregate supply will shift the respective demand or supply curve and will change the equilibrium level of output and prices in the economy. For the changes in each factor described below in column A, select from the option list in column B the most likely initial effect of the change on aggregate demand or aggregate supply. Each item in the option list may be used once, more than once, or not at all. lfthe factor change will not affect aggregated demand or aggregate supply, select \"No effect." Factor Change Most Likely Effect An increase in consumer condence An increase in the sale of government bonds by the Open Market Committee of the Federal Reserve A decrease in government spending An increase in the cost of production inputs A decrease in the availability of skilled labor A decrease in personal income taxes An increase in stock prices on major exchanges A technological breakthrough that will have widespread benefit O Increase aggregate demand O Increase aggregate supply O Decrease aggregate demand O Decrease aggregate supply O No effect

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts