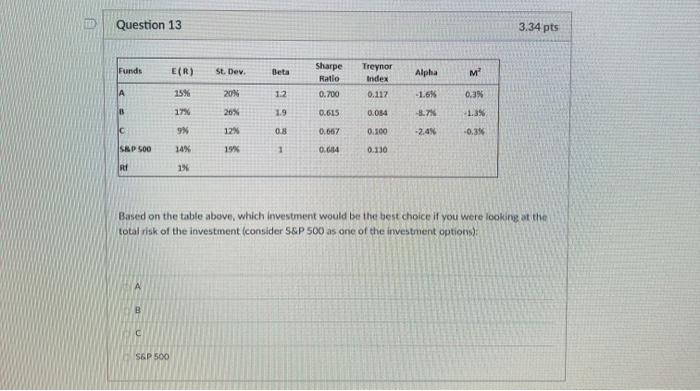

Question: TE Question 13 3.34 pts Funds E(R) st. Der Beta Alpha M Sharpe Ratio 0.700 Treynor Index 0.117 A 25% 20N 1.2 -1.6% 0.3% B

TE Question 13 3.34 pts Funds E(R) st. Der Beta Alpha M Sharpe Ratio 0.700 Treynor Index 0.117 A 25% 20N 1.2 -1.6% 0.3% B 17% 20% 1.9 0.615 0.054 -1.3 C 9X 12% 08 0.667 0.100 -2.4% -0.3% SAP 500 14% 19% 1 0.684 0.130 RI 1% Based on the table above, which investment would be the best choice if you were looking at the total risk of the investment consider S&P 500 as one of the investment options) B C S&P 500

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock