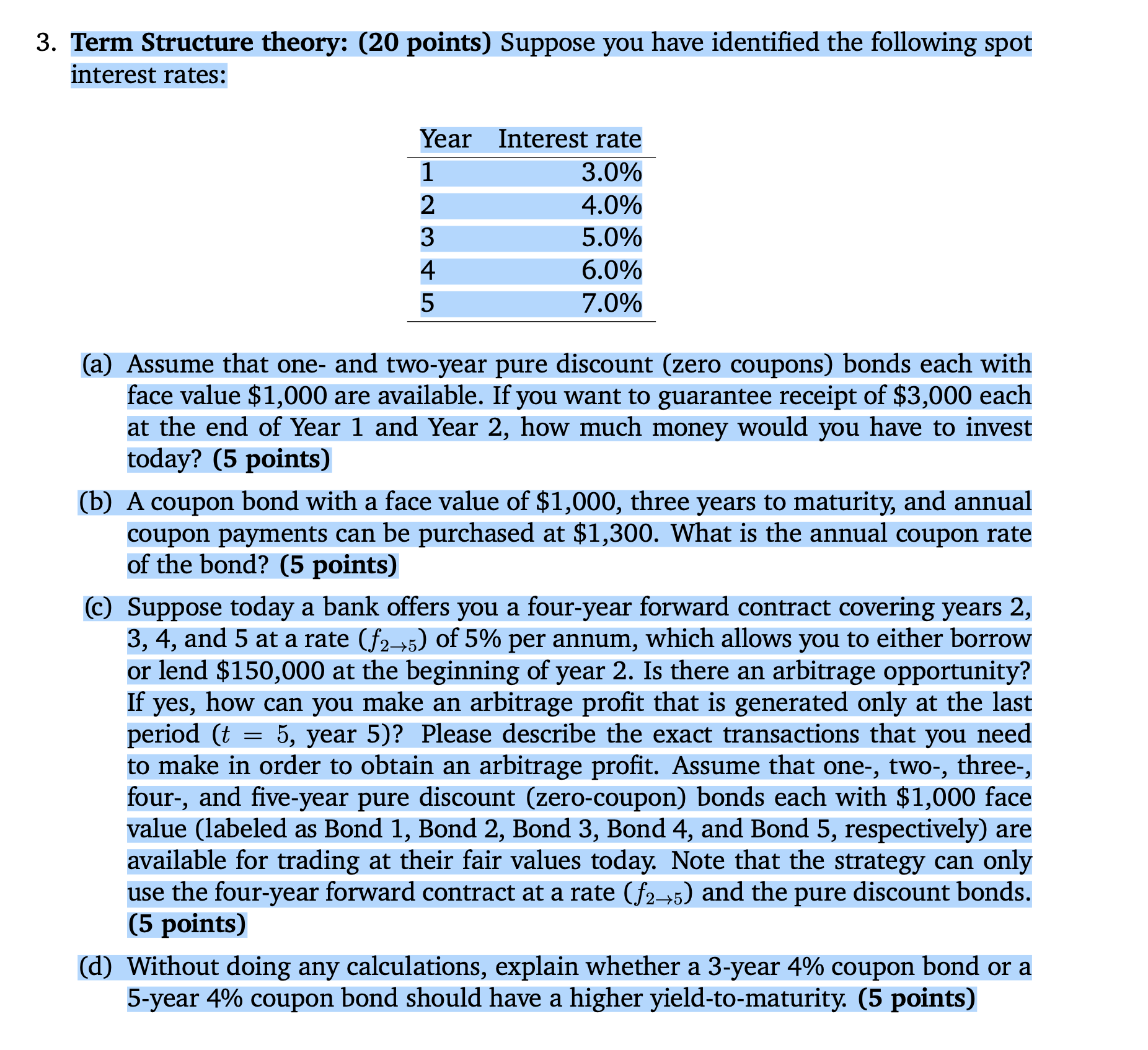

Question: Term Structure theory: ( 2 0 points ) Suppose you have identified the following spot interest rates: ( a ) Assume that one - and

Term Structure theory: points Suppose you have identified the following spot

interest rates:

a Assume that one and twoyear pure discount zero coupons bonds each with

face value $ are available. If you want to guarantee receipt of $ each

at the end of Year and Year how much money would you have to invest

today? points

b A coupon bond with a face value of $ three years to maturity, and annual

coupon payments can be purchased at $ What is the annual coupon rate

of the bond? points

c Suppose today a bank offers you a fouryear forward contract covering years

and at a rate of per annum, which allows you to either borrow

or lend $ at the beginning of year Is there an arbitrage opportunity?

If yes, how can you make an arbitrage profit that is generated only at the last

period year Please describe the exact transactions that you need

to make in order to obtain an arbitrage profit. Assume that one two three

four and fiveyear pure discount zerocoupon bonds each with $ face

value labeled as Bond Bond Bond Bond and Bond respectively are

available for trading at their fair values today. Note that the strategy can only

use the fouryear forward contract at a rate and the pure discount bonds.

points

d Without doing any calculations, explain whether a year coupon bond or a

year coupon bond should have a higher yieldtomaturity. points

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock