Question: + * Thark | 18 | E X 4-0 2 A-07-Ch P A-01-2h E A-07-C8 | 15 3 lg B af Thank Y noorstin Sign

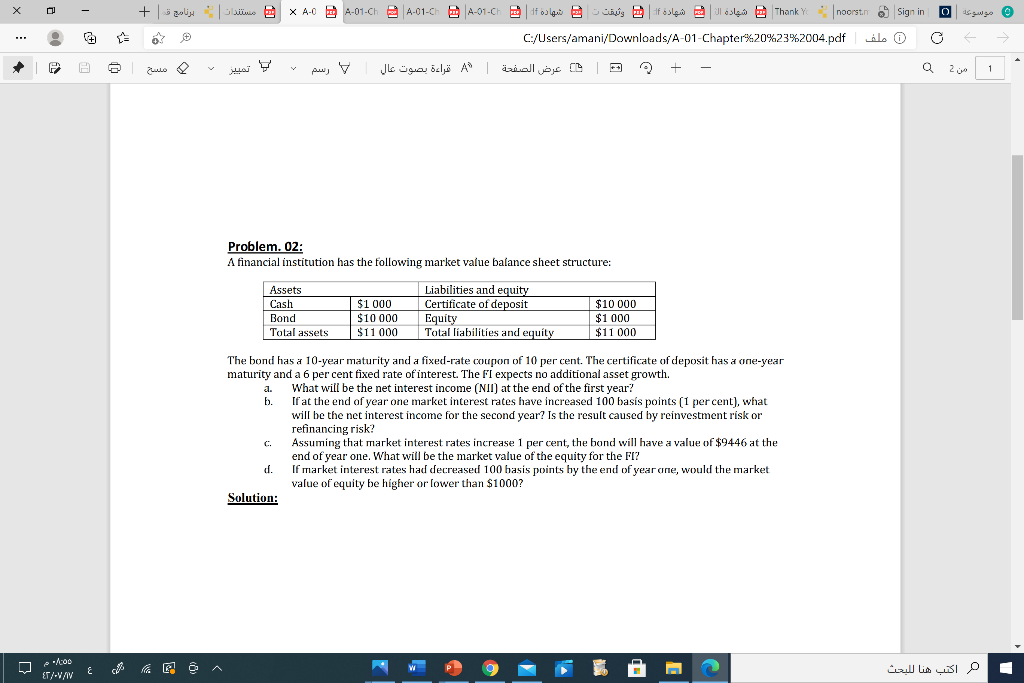

+ * Thark | 18 | E X 4-0 2 A-07-Ch P A-01-2h E A-07-C8 | 15 3 lg B af Thank Y noorstin Sign in C:/Users/amani/Downloads/A-01-Chapter%20%23%2004.pdf 1) > P | ft | 49 + 1 Problem. 02: A financial institution has the following market value balance sheet structure: Assets Cash Bond Total assets $1 000 $10 000 $11000 Liabilities and equity Certificate of deposit Equity Total liabilities and equity $10 000 $1 000 $11 000 a. h. The bond has a 10-year maturity and a fixed-rate coupon of 10 per cent. The certificate of deposit has a one-year maturity and a 6 per cent fixed rate of interest. The FI expects no additional asset growth. What will be the net interest income (NII) at the end of the first year? If at the end of year one market interest rates have increased 100 basis points (1 per cent), what will be the net interest income for the second year? Is the result caused by reinvestment risk or refinancing risk? Assuming that market interest rates increase 1 per cent, the bond will have a value of $9446 at the end of year one. What will be the market value of the equity for the FI? If market interest rates had decreased 100 basis points by the end of year one, would the market value of equity be higher or lower than $1000? Solution: -A OD ET/-V/IV E E

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts