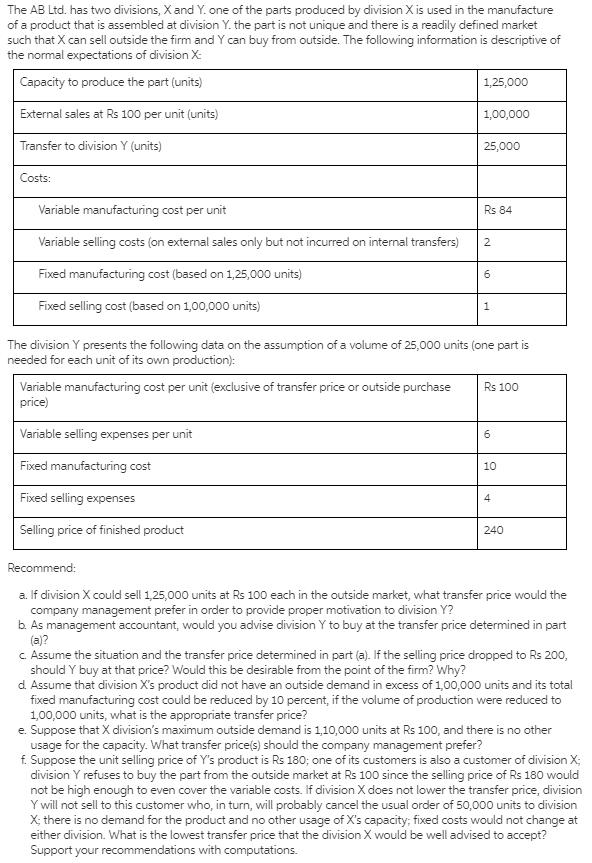

The AB Ltd. has two divisions, X and Y. one of the parts produced by division...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations. The AB Ltd. has two divisions, X and Y. one of the parts produced by division X is used in the manufacture of a product that is assembled at division Y. the part is not unique and there is a readily defined market such that X can sell outside the firm and Y can buy from outside. The following information is descriptive of the normal expectations of division X: Capacity to produce the part (units) External sales at Rs 100 per unit (units) Transfer to division Y (units) Costs: Variable manufacturing cost per unit Variable selling costs (on external sales only but not incurred on internal transfers) Fixed manufacturing cost (based on 1,25,000 units) Fixed selling cost (based on 1,00,000 units) 1,25,000 Variable manufacturing cost per unit (exclusive of transfer price or outside purchase price) Variable selling expenses per unit Fixed manufacturing cost Fixed selling expenses Selling price of finished product 1,00,000 25,000 Rs 84 2 6 1 The division Y presents the following data on the assumption of a volume of 25,000 units (one part is needed for each unit of its own production): Rs 100 6 10 4 240 Recommend: a. If division X could sell 1,25,000 units at Rs 100 each in the outside market, what transfer price would the company management prefer in order to provide proper motivation to division Y? b. As management accountant, would you advise division Y to buy at the transfer price determined in part (a)? c. Assume the situation and the transfer price determined in part (a). If the selling price dropped to Rs 200, should Y buy at that price? Would this be desirable from the point of the firm? Why? d. Assume that division X's product did not have an outside demand in excess of 1,00,000 units and its total fixed manufacturing cost could be reduced by 10 percent, if the volume of production were reduced to 1,00,000 units, what is the appropriate transfer price? e. Suppose that X division's maximum outside demand is 1,10,000 units at Rs 100, and there is no other usage for the capacity. What transfer price(s) should the company management prefer? f. Suppose the unit selling price of Y's product is Rs 180; one of its customers is also a customer of division X; division Y refuses to buy the part from the outside market at Rs 100 since the selling price of Rs 180 would not be high enough to even cover the variable costs. If division X does not lower the transfer price, division Y will not sell to this customer who, in turn, will probably cancel the usual order of 50,000 units to division X; there is no demand for the product and no other usage of X's capacity; fixed costs would not change at either division. What is the lowest transfer price that the division X would be well advised to accept? Support your recommendations with computations.

Expert Answer:

Answer rating: 100% (QA)

Requirement a If division X could sell 125000 units in the external market the transfer price ... View the full answer

Related Book For

Management and Cost Accounting

ISBN: 978-1405888202

4th edition

Authors: Alnoor Bhimani, Charles T. Horngren, Srikant M. Datar, George Foster

Posted Date:

Students also viewed these accounting questions

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

The Manes Company has two products. Product 1 is manufactured entirely in Division X. Product 2 is manufactured entirely in Division Y. To produce these two products, the Manes Company has two...

-

Tasman Teleco Ltd has two divisions and operates out of Auckland, New Zealand. The Express Division manufactures and transfers a range of computer circuit boards to the Harris Division, which uses...

-

Top executive officers of Preston Company, a merchandising firm, are preparing the next years budget. The controller has provided everyone with the current years projected income statement. Current...

-

The following figures were taken from the 2011 and 2012 Balance Sheet 2011 2012 Cash 30 A/R Inventory Supplies PP&E Accumulated Depreciation Total assets You can make up numbers here AP 2012 2011...

-

Switching to International Financial Reporting Standards (IFRS) will require companies to incur significant costs. What are the benefits of countries adopting IFRS?

-

What the differences are between arbitration and mediation?

-

Cash flow analysis, chapter appendix. (CMA, adapted) TabComp, Inc., is a retail distributor for MZB-33 computer hardware and related software and support services. TabComp prepares annual sales...

-

1. Identify and evaluate Wal-Mart's strategies. What Wal-Mart strategies led to success? 2. What were the strengths and weaknesses of Wal-Mart from the perspective of (a) Wegmans and (b) Costco?...

-

Solve this in python. **[70 pts]** You will be writing code for recording the menuitems and daily sales of a lemonade stand. It will have theseclasses: MenuItem, SalesForDay, and LemonadeStand. All...

-

If autonomous investment increases by $100 billion, equilibrium real GDP demanded will O increase by $100 billion O not change O increase by ($100 billion)/MPC O increase by $100 billion x MPC...

-

On August 17, 2022, MV Jefferson Flute Corp. signed a one-year service lease with Madison Orchestra Supplies to repair and maintain flutes and other wind instruments for a fee of $8,200 per month...

-

A 10.5% coupon bond, semi-annual payments, ten years to maturity is callable in three years at a call price of $1,150. If the bond is selling today for $1120, what is the yield to call ?

-

If the taxpayer is a Filipino engineer and an employee of a domestic corporation in the Philippines. He is assigned to render services in USA. He will stay abroad for a maximum period of 15 months....

-

Assume that you can borrow and lend at a riskless rate of 3.6%. If you invest 60% un 30 IWM and 40% in the risk free asset. The mean of your portfolio is A 2.16% B 1.44% C 1.80% D None of the above...

-

2. Draw the UML class diagram relationships for the program. LAB 3.3: Composition PROGRAM 3 // Java program to illustrate the concept of Composition // Class 1 public public String author; //...

-

Issues and questions to considerwhen writing the paper You should first start your assignment with a general paragraph or two about your overarching philosophy about global problems and what you feel...

-

(a) Explain why the concentration of dissolved oxygen in freshwater is an important indicator of the quality of the water. (b) How is the solubility of oxygen in water affected by increasing...

-

'Accountants have placed stocks on the wrong side of the balance sheet. They are a liability, not an asset.' Comment on this statement by a plant manager.

-

Jskinen Oy has just today paid for and installed a special machine for polishing cars at one of its several outlets. It is the first day of the company's fiscal year. The machine cost 20 000. Its...

-

Why might a company prefer the adjusted allocation rate approach over a proration approach to under- or over allocated indirect costs?

-

Which type of business organization is owned by its stockholders? a. Proprietorship b. Partnership C. Corporation d. All the above are owned by stockholders.

-

Consider the overall effects of transactions in questions 5, 6, and 7 on Boardmaster. What is Boardmasters net income or net loss? a. Net income of \($57,000 b. \) Net loss of \($3,000\) C. Net...

-

The income statement reports a. financial position on a specific date. b. results of operations on a specific date. C. financial position for a specific period. d. results of operations for a...

Study smarter with the SolutionInn App