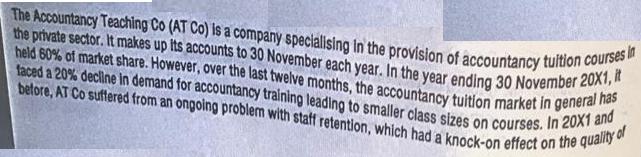

The Accountancy Teaching Co (AT Co) is a company specialising in the provision of accountancy tuition...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

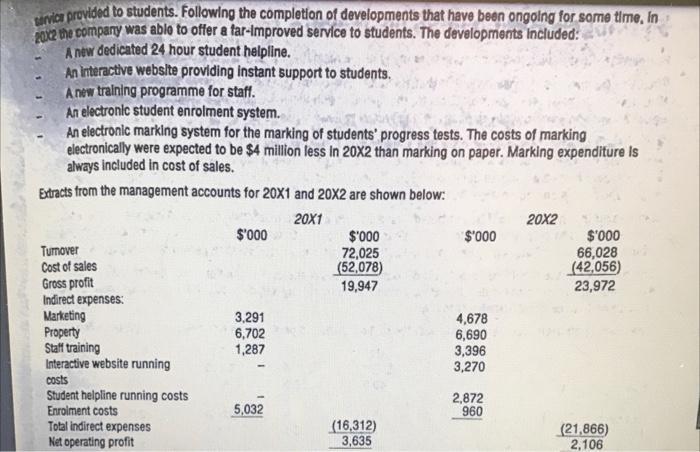

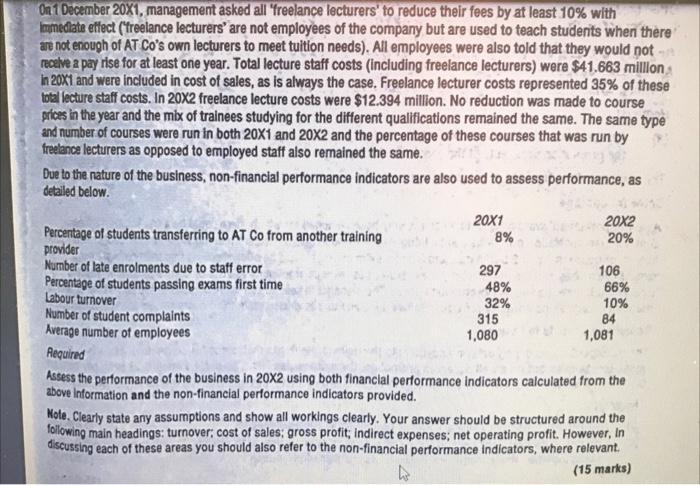

The Accountancy Teaching Co (AT Co) is a company specialising in the provision of accountancy tuition courses in the private sector. It makes up its accounts to 30 November each year. In the year ending 30 November 20X1, #t held 60% of market share. However, over the last twelve months, the accountancy tuition market in general has faced a 20% decline in demand for accountancy training leading to smaller class sizes on courses. In 20X1 and before, AT Co suffered from an ongoing problem with staff retention, which had a knock-on effect on the quality of service provided to students. Following the completion of developments that have been ongoing for some time. In 2012 the company was able to offer a far-improved service to students. The developments included: A new dedicated 24 hour student helpline. An interactive website providing instant support to students. A new training programme for staff. An electronic student enrolment system. An electronic marking system for the marking of students' progress tests. The costs of marking electronically were expected to be $4 million less in 20X2 than marking on paper. Marking expenditure is always included in cost of sales. Extracts from the management accounts for 20X1 and 20X2 are shown below: 20X1 Turnover Cost of sales Gross profit Indirect expenses: Marketing Property Staff training Interactive website running costs Student helpline running costs Enrolment costs Total indirect expenses Net operating profit $'000 3,291 6,702 1,287 5,032 $'000 72,025 (52,078) 19,947 (16,312) 3,635 $'000 4,678 6,690 3,396 3,270 2,872 960 20X2 $'000 66,028 (42,056) 23,972 (21,866) 2,106 On 1 December 20X1, management asked all 'freelance lecturers' to reduce their fees by at least 10% with Immediate effect (freelance lecturers' are not employees of the company but are used to teach students when there are not enough of AT Co's own lecturers to meet tuition needs). All employees were also told that they would not receive a pay rise for at least one year. Total lecture staff costs (including freelance lecturers) were $41.663 million in 20X1 and were included in cost of sales, as is always the case. Freelance lecturer costs represented 35% of these total lecture staff costs. In 20X2 freelance lecture costs were $12.394 million. No reduction was made to course prices in the year and the mix of trainees studying for the different qualifications remained the same. The same type and number of courses were run in both 20X1 and 20X2 and the percentage of these courses that was run by freelance lecturers as opposed to employed staff also remained the same. Due to the nature of the business, non-financial performance indicators are also used to assess performance, as detailed below. Percentage of students transferring to AT Co from another training provider Number of late enrolments due to staff error Percentage of students passing exams first time Labour turnover Number of student complaints Average number of employees Required 20X1 8% 297 48% 32% 315 1,080 20X2 20% 106 66% 10% 84 1,081 Assess the performance of the business in 20X2 using both financial performance indicators calculated from the above information and the non-financial performance indicators provided. Note. Clearly state any assumptions and show all workings clearly. Your answer should be structured around the following main headings: turnover; cost of sales; gross profit; indirect expenses; net operating profit. However, in discussing each of these areas you should also refer to the non-financial performance Indicators, where relevant. (15 marks) The Accountancy Teaching Co (AT Co) is a company specialising in the provision of accountancy tuition courses in the private sector. It makes up its accounts to 30 November each year. In the year ending 30 November 20X1, #t held 60% of market share. However, over the last twelve months, the accountancy tuition market in general has faced a 20% decline in demand for accountancy training leading to smaller class sizes on courses. In 20X1 and before, AT Co suffered from an ongoing problem with staff retention, which had a knock-on effect on the quality of service provided to students. Following the completion of developments that have been ongoing for some time. In 2012 the company was able to offer a far-improved service to students. The developments included: A new dedicated 24 hour student helpline. An interactive website providing instant support to students. A new training programme for staff. An electronic student enrolment system. An electronic marking system for the marking of students' progress tests. The costs of marking electronically were expected to be $4 million less in 20X2 than marking on paper. Marking expenditure is always included in cost of sales. Extracts from the management accounts for 20X1 and 20X2 are shown below: 20X1 Turnover Cost of sales Gross profit Indirect expenses: Marketing Property Staff training Interactive website running costs Student helpline running costs Enrolment costs Total indirect expenses Net operating profit $'000 3,291 6,702 1,287 5,032 $'000 72,025 (52,078) 19,947 (16,312) 3,635 $'000 4,678 6,690 3,396 3,270 2,872 960 20X2 $'000 66,028 (42,056) 23,972 (21,866) 2,106 On 1 December 20X1, management asked all 'freelance lecturers' to reduce their fees by at least 10% with Immediate effect (freelance lecturers' are not employees of the company but are used to teach students when there are not enough of AT Co's own lecturers to meet tuition needs). All employees were also told that they would not receive a pay rise for at least one year. Total lecture staff costs (including freelance lecturers) were $41.663 million in 20X1 and were included in cost of sales, as is always the case. Freelance lecturer costs represented 35% of these total lecture staff costs. In 20X2 freelance lecture costs were $12.394 million. No reduction was made to course prices in the year and the mix of trainees studying for the different qualifications remained the same. The same type and number of courses were run in both 20X1 and 20X2 and the percentage of these courses that was run by freelance lecturers as opposed to employed staff also remained the same. Due to the nature of the business, non-financial performance indicators are also used to assess performance, as detailed below. Percentage of students transferring to AT Co from another training provider Number of late enrolments due to staff error Percentage of students passing exams first time Labour turnover Number of student complaints Average number of employees Required 20X1 8% 297 48% 32% 315 1,080 20X2 20% 106 66% 10% 84 1,081 Assess the performance of the business in 20X2 using both financial performance indicators calculated from the above information and the non-financial performance indicators provided. Note. Clearly state any assumptions and show all workings clearly. Your answer should be structured around the following main headings: turnover; cost of sales; gross profit; indirect expenses; net operating profit. However, in discussing each of these areas you should also refer to the non-financial performance Indicators, where relevant. (15 marks)

Expert Answer:

Related Book For

Advanced Accounting

ISBN: 978-0538480284

11th edition

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

Posted Date:

Students also viewed these accounting questions

-

Natatshas friend, Sharleen, owns Sharleen Ahmed, a company specialising in low quality, high priced clothing. The material is purchased from Canada, made up into the finished garments in her own...

-

Q4. The Portable Garage Co (PGC) is a company specialising in the manufacture and sale of a range of products for motorists. It is split into two divisions: the battery division (Division B) and the...

-

Wiper democratic is a company specialising in the sale of high-quality bananas. The company sales representatives sell bananas to distributors all over the country. The basic price for each carton is...

-

What are the advantages and disadvantages of Qantass international cooperative alliances? The Qantas Group maintained its strong position in the Australian domestic market in 2016/17. Through a dual...

-

The Meyer Company must arrange financing for its working capital requirements for the coming year. Meyer can (a) Borrow from its bank on a simple interest basis (interest payable at the end of the...

-

Two objects are identical except that one is hotter than the other. Compare how they respond to identical forces.

-

In 2013, Thomas DePrince, a passenger aboard a cruise ship, visited the ships jewelry boutique, operated by Starboard Cruise Services, Inc. DePrince told the employees of the boutique that he was...

-

Entries for Acquisition of Assets Presented below are information related to Rommel Company. 1. On July 6 Rommel Company acquired the plant assets of Studebaker Company, which had discontinued...

-

A 47-kg pole vaulter running at 10 m/s vaults over the bar. Her speed when she is above the bar is 1.5 m/s. Neglect air resistance, as well as any energy absorbed by the pole, and determine her...

-

Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 20Y5. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter....

-

15. Draw and explain the I-V characteristics curve of a PN junction diode.

-

T owns a two-bedroom vacation home that T rents for 90 days and uses for personal purposes for 30 days during the taxable year. T receives gross rental income from the home of $3,000, pays deductible...

-

12.3. Calculate the IRR, given a discount rate of 10% and the table below: CFO CF1 CF2 CF3 Operating Cash Flow 0 120 155 195 Change in Net WC -25 0 25 25 Terminal Cash Flow 50 60 Initial Cost -375...

-

What specific characteristic of modernism does Venturi fundamentally contest or oppose?

-

Button Corp. sold its investment of 2 0 0 shares of a public company, which it measured at FVPL . How should the loss of the sale of the shares be treated by Button in its financial statements,...

-

How do the narrative devices of intertextuality and metafiction in Italo Calvino's "If on a winter's night a traveler" serve to challenge conventional understandings of authorship and reader...

-

A corporation issues 2,500 shares of common stock for 45,000. The stock has stated value of 10 per share. The journal entry to record the stock issuance would include a credit to ordinary shares for?

-

Grace is training to be an airplane pilot and must complete five days of flying training in October with at least one day of rest between trainings. How many ways can Grace schedule her flying...

-

The following determination and distribution of excess schedule is prepared on January 1, 2012, the date on which Parker Company purchases a 60% interest in Share Company: On December 31, 2013,...

-

On January 1, 2011, Pillar Company purchases an 80% interest in Stark Company for $890,000. On the date of acquisition, Stark has total owners equity of $800,000. Buildings, which have a 20-year...

-

Flom Company is considering the cash purchase of 100% of the outstanding stock of Vargas Company. The terms are not set, and alternative prices are being considered for negotiation. The balance sheet...

-

Prove Part 1 of Theorem 1.14 using induction. That is, prove that for any non-negative integer \(k\), \[H_{k}(x)=\sum_{i=0}^{\lfloor k / 2floor}(-1)^{i} \frac{(2 i) !}{2^{i} i...

-

Use Theorem 1.13 (Taylor) to find fourth and fifth order polynomials that are approximations to the standard normal distribution function \(\Phi(x)\). Is there a difference between the...

-

Prove Part 2 of Theorem 1.14. That is, prove that for any non-negative integer \(k \geq 2\), \[H_{k}(x)=x H_{k-1}(x)-(k-1) H_{k-2}(x) .\] The simplest approach is to use Definition 1.6. Theorem 1.14....

Study smarter with the SolutionInn App