Question: The assignment is based on Illustration 1 5 - 6 on p . 6 3 0 . Your are required to determine which ( if

The assignment is based on Illustration on p Your are required to determine which if any of the potential componenty units BC or D must be included as part of the City of Lubburg's A financial reporting entity. Your solution must include a clear indication for each of the potential component units shown B Lubburg Independent School District; C Lubburg Building Authority; D Lubburg Transit Authority as to whether:

it should be included in As financial reporting entity and why it should be included, or

it should not be included in As financial reporting entity, and why it should not be included

Your answers should be based on the criteria discussed on pp

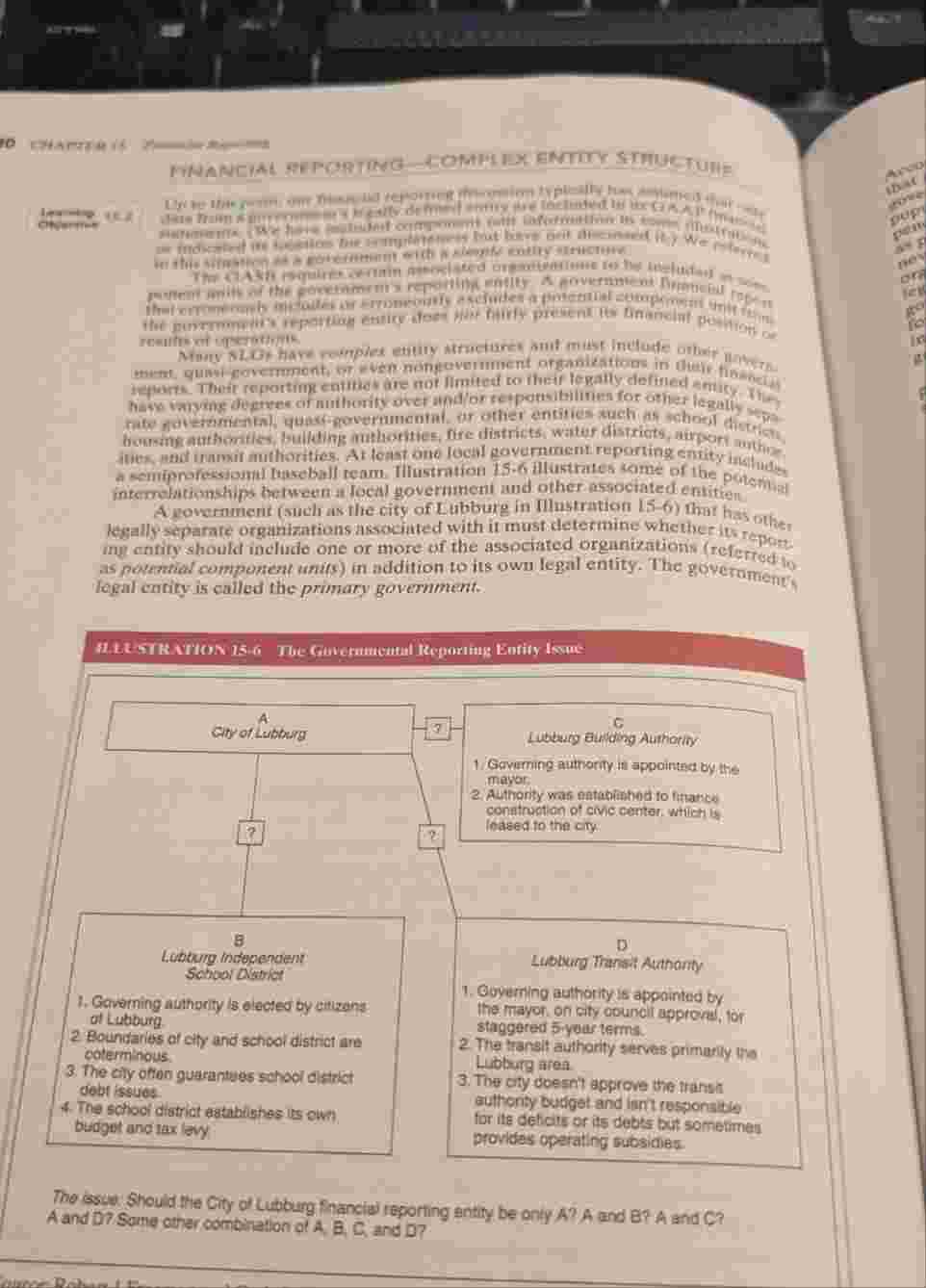

ve imdsmbe rewilferi has tw as poweraid compongeri amifs in addition to is own legal entity. The goveramenth legal concity is called the primary govermment.

Lubburg Bulding Authoriny

Gofvirming aumority in appointact by the mayor:

Althonty was ontacimbed to finance conitruction of civic ceerter whilichly lebsed to the cry

B

Lobturg indoperoien

Schbor Dismicer

Governing authprity is oleces by citluang of Lubburg.

Bounifaries of city and schicol district ane coterminous

The cily ofton guarantues school district dobr issues.

The school district engabtimes its own budget andiax lewy

D

Lublumg Thanact Authomity

Goyerning authority is appointed by the mayor, on aity council approre, for staggered Fiywur terms.

The transit authority serves primurly tho Lubturg area

The ory doesn't approve the transt authonty budget and fimt responalite for its defidets or its debts bit sometmen provides operating rubsimies.

Tho losut Should the City of tubburg financiej reporting entity be onty A A and B A and C A and D Same cher combiration of A B Ci and D

of necilitatint itie dellyery af gover trment sevice. ment' s financial statments miyrading

Financial accowntability is the brasdest, most coumes basis for an orgamize non to be a component unit. Financial accountability is explaned in thustration As the illustration indicates, a primary governmeth carnat be finazcinally cceuntable for an organization unless it either appoints in voting majority of the organization's governing body or has a financmi benefit or burden retationship with the organization. The primary government PG is financially acconatable for other organizations if the PG has:

Both appointment authority and a financial benefit or burden relstisusisp with wather entity, or

Appoinment authoriry over another entity upon which it has the abllity to impoxe its will see Illustration or

A financial benefit and burden relationship with another entity that is fiscully dependent on the PG as described in the illustration

If a PG is not financially accountable for another entity, il still may be required. or choose, to treat other entities as component units for other reasons.

Holding a majority equity interest in another entity is another important reporting entity definition criterion. Although it is unusual foragoverment to hold & majority equity interest in a business for the purpose of facilitating delivery of government services, it is very common for governments to enter into joint ventures with other governments. Airports, correctional centers, bus and rail transportation, antimal shelters, and economic development activities are only a few of the rypes of joint ventures conducted by governments around the country. The participating governments hold equity interests in many of these joint ventures. For other joint ventures, there are no equity interests. Even if a primary government is not financally accountable for an organization, it must include it as a component unit it it holds a majority equity interest in it for the purpose of delivering government services.

Fundraising organizations are addressed primarily in GASB Statement No "The Financial Reporting EntityAffliated Organizations." This statement requires component unit treatment for any affiliated, legally separate, taxexemps entity if all of the following are true.

THE FEVANCIAL ACCOUNTABILTY CRTTERLA any amponent unit's board or official, arany other uppointec of the PG

DNAVCIAL BENEFTI OR BERDEN REIATIONSHIPS: ane of the following is truc:

The PG has the ability lo access the resources of the entity without dissotation of the ontity, ar

The PG is legally or otherwise obligated to finance the deficits of or provide flumeiad support ather thin in oxchange or cxebangelike lrankactions to the organization, or

The PCI is abligated in some mannen for the debt of the organizstion

ABILITY TO IMPOSE WILL RELATIONSHIPS:

A primary government has the ubility to impose is will ie significantly influence the tspo and levels of services on a potential component unit if the primary government has the tubstantive authority to do any one of the following:

Remove appointed governing board members at will, or

Approve or require

Reporting Eutly Disclos

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock