Question: The attached are Finance problems regarding CAPM, Option pricing, Bond pricing. I know how to calculate alpha, beta for Question 1. However, please help with

The attached are Finance problems regarding CAPM, Option pricing, Bond pricing.

I know how to calculate alpha, beta for Question 1.

However, please help with the question B and D (I don't understand what the question is asking)

But please help me with the question 2.

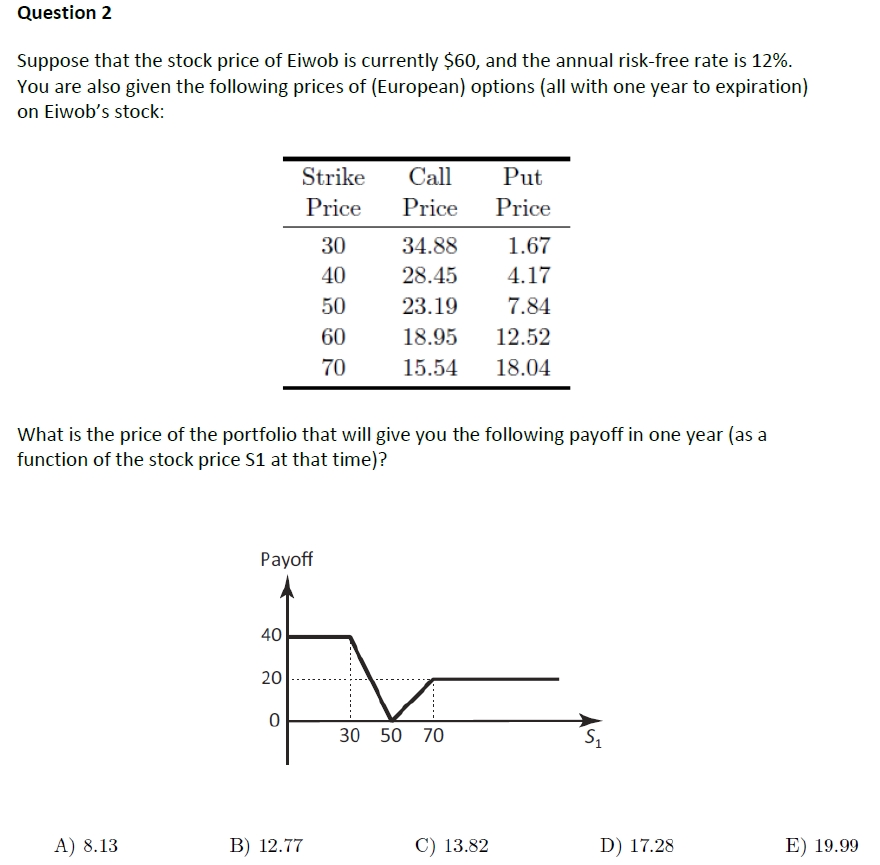

I don't understand how I can get the portfolio as it is shown in the graph, and how i can calculate the price of the portfolio.

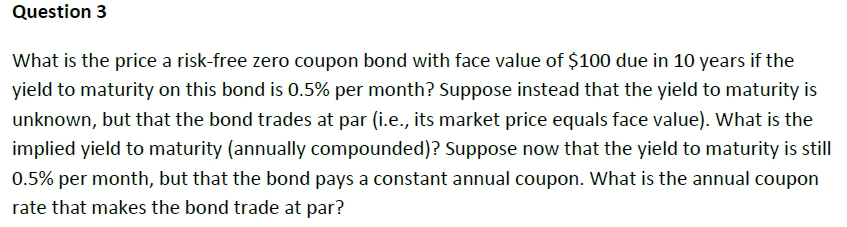

Please help me with the question 3 as well.

Thank you.

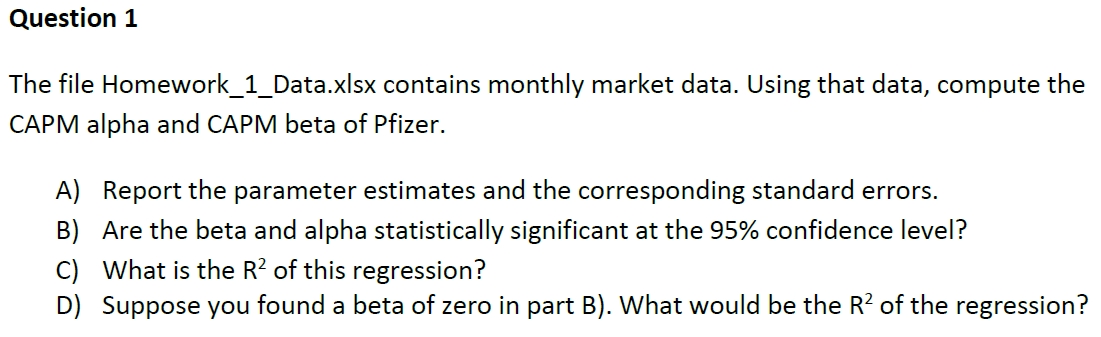

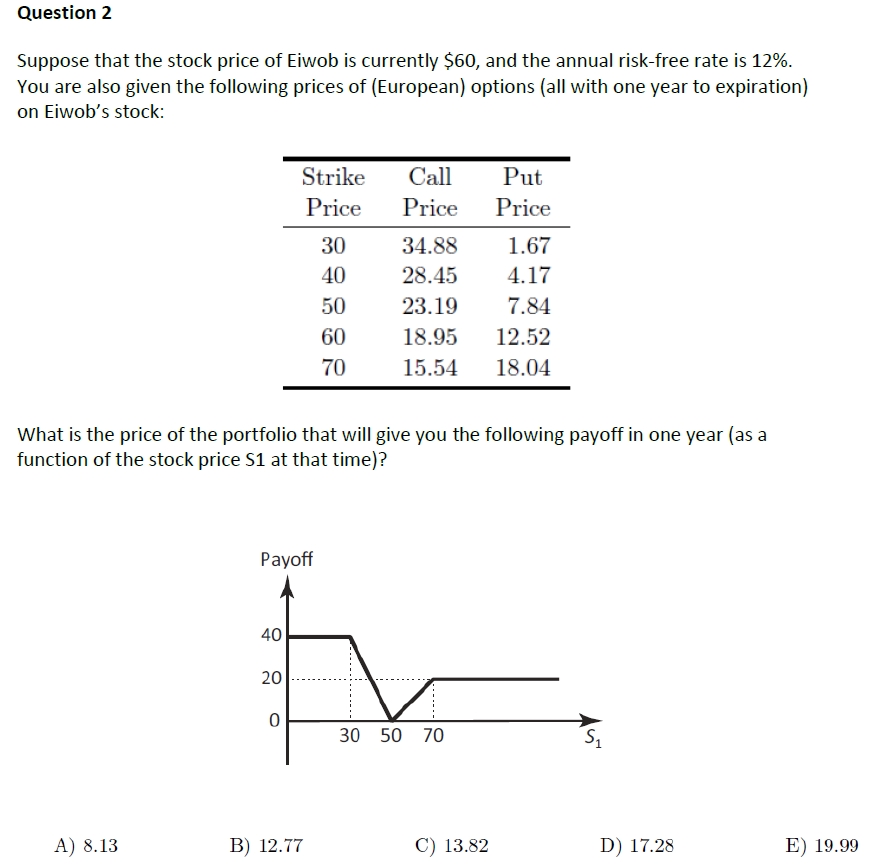

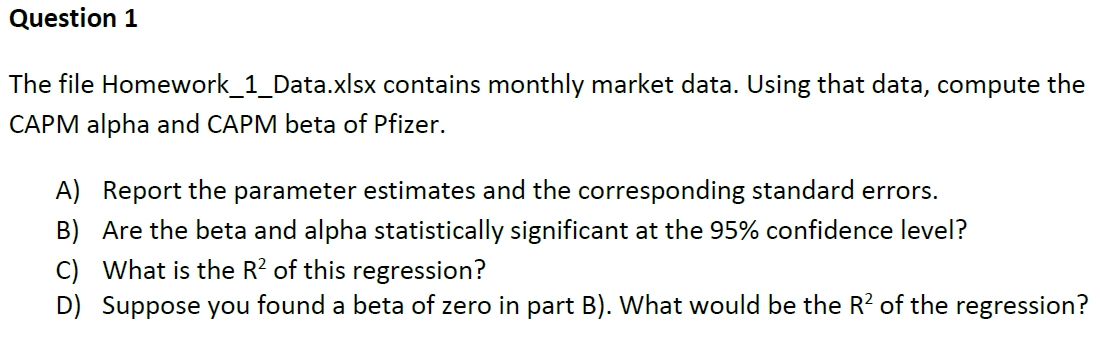

Question 1 The file Homework_1_Data.xlsx contains monthly market data. Using that data, compute the CAPM alpha and CAPM beta of Pfizer. A) Report the parameter estimates and the corresponding standard errors. B) Are the beta and alpha statistically significant at the 95% confidence level? C) What is the R2 of this regression? D) Suppose you found a beta of zero in part B). What would be the R2 of the regression? Question 2 Suppose that the stock price of Eiwob is currently 560, and the annual riskfree rate is 12%. You are also given the following prices of {European} options (all with one year to expiration] on Eiwob's stock: Strike Call P111: Price Price Price 30 34.88 1.67 40 28-45 4-17 50 23.19 7.84 60 18.95 12.52 70 15.54 18.04 What is the price of the portfolio that will give you the following payoff in one year {as a function of the stock price 51 at that time]? Payoff 40 20 ---------- : 3E} 50 70 A] 8.13 B] 12.77 C) 13.32 D) 17.23 E) 19.99 Question 3 What is the price a riskfree zero coupon bond with face value of $100 due in 10 years ifthe yield to maturity on this bond is 0.5% per month? Suppose instead that the yield to maturity is unknown, but that the bond trades at par {i.e., its market price equals face value). What is the implied yield to maturity {annually compounded)? Suppose now that the yield to maturity is still 0.5% per month, but that the bond pays a constant annual coupon. What is the annual coupon rate that makes the bond trade at par

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts