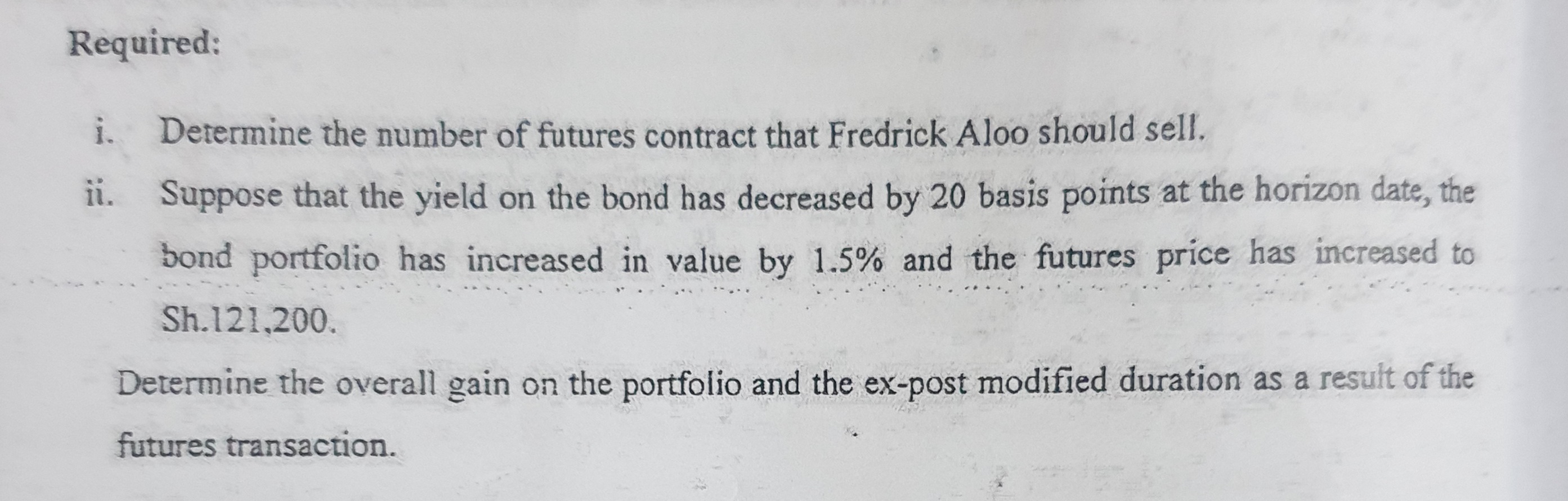

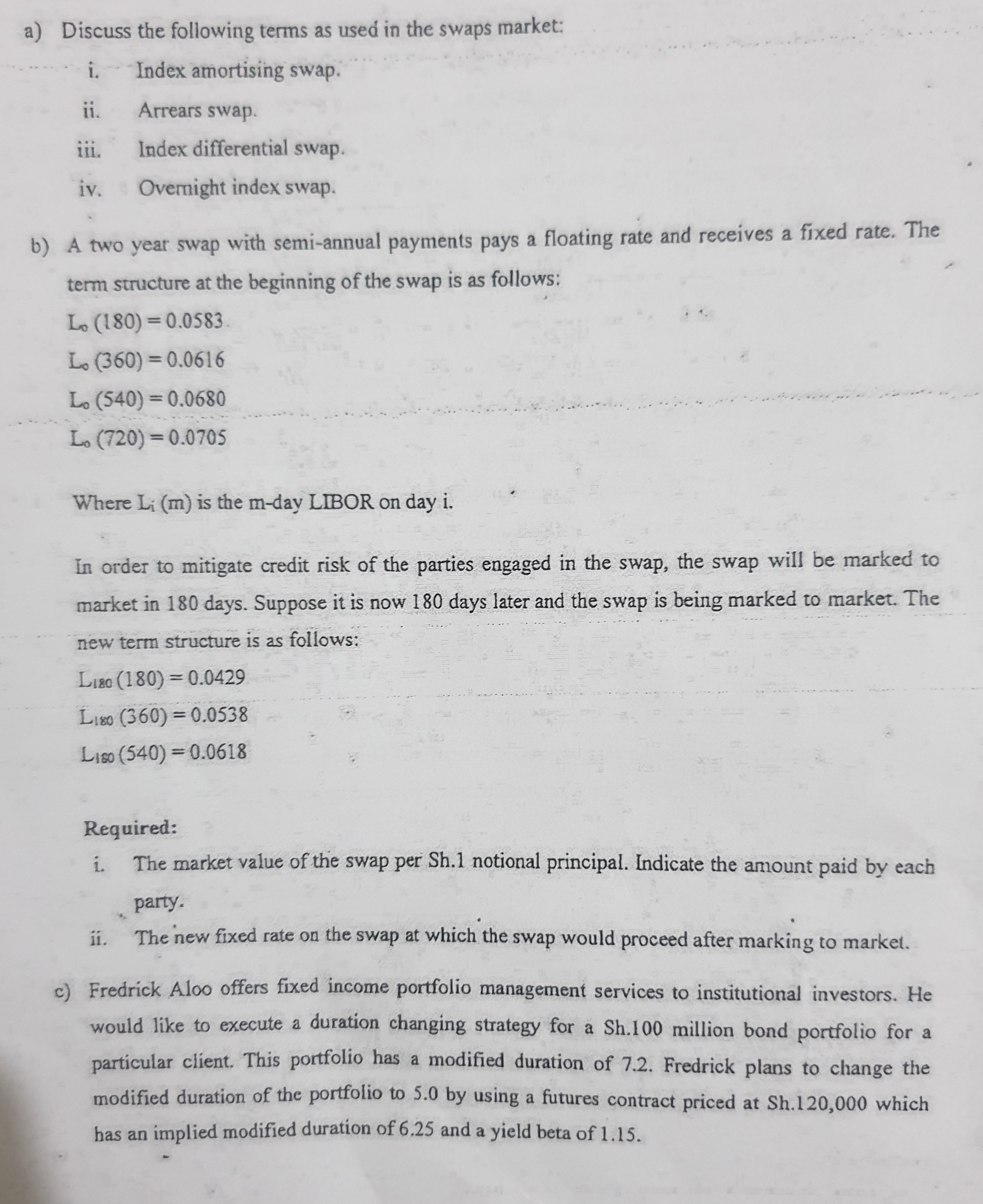

Question: The attachment below contains questions,please answer them Correctly Required: i. Determine the number of futures contract that Fredrick Aloo should sell. ii. Suppose that the

The attachment below contains questions,please answer them Correctly

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock