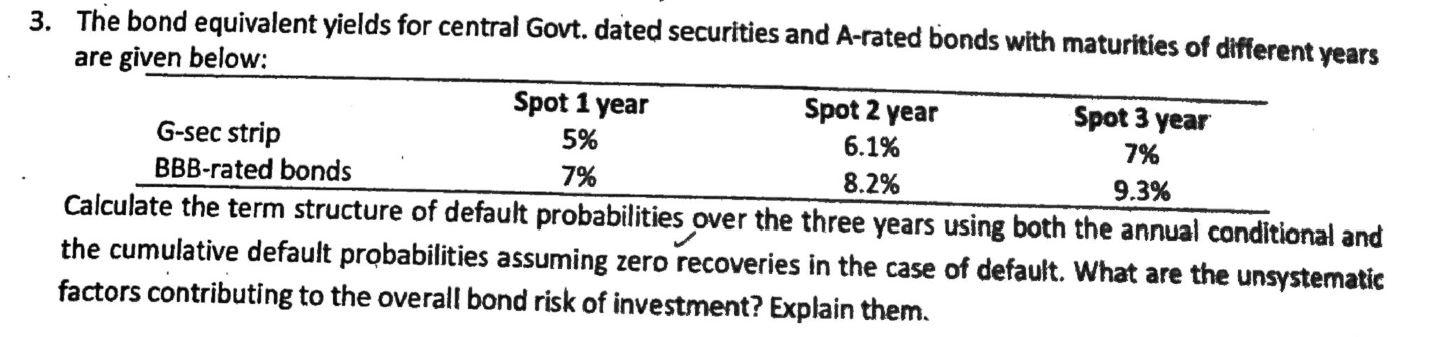

Question: The bond equivalent yields for central Govt. dated securities and A-rated bonds with maturities of different years are given below: Calculate tne term structure of

The bond equivalent yields for central Govt. dated securities and A-rated bonds with maturities of different years are given below: Calculate tne term structure of default probabilities over the three years using both the annual conditional and the cumulative default probabilities assuming zero recoveries in the case of default. What are the unsystematic factors contributing to the overall bond risk of investment? Explain them. The bond equivalent yields for central Govt. dated securities and A-rated bonds with maturities of different years are given below: Calculate tne term structure of default probabilities over the three years using both the annual conditional and the cumulative default probabilities assuming zero recoveries in the case of default. What are the unsystematic factors contributing to the overall bond risk of investment? Explain them

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts