Question: The case is attached, please refer to the documents Please provide the following: 1) PEST-EL Analysis (Political, Economic, Social, Technological, Environmental, Legal) 2) Porter's 5

The case is attached, please refer to the documents

Please provide the following:

1) PEST-EL Analysis (Political, Economic, Social, Technological, Environmental, Legal)

2) Porter's 5 forces (Threat of new entry, buyer power, threat of substitution, supplier power, competitive rivalry)

You can zoom in when reading the case

Thank you

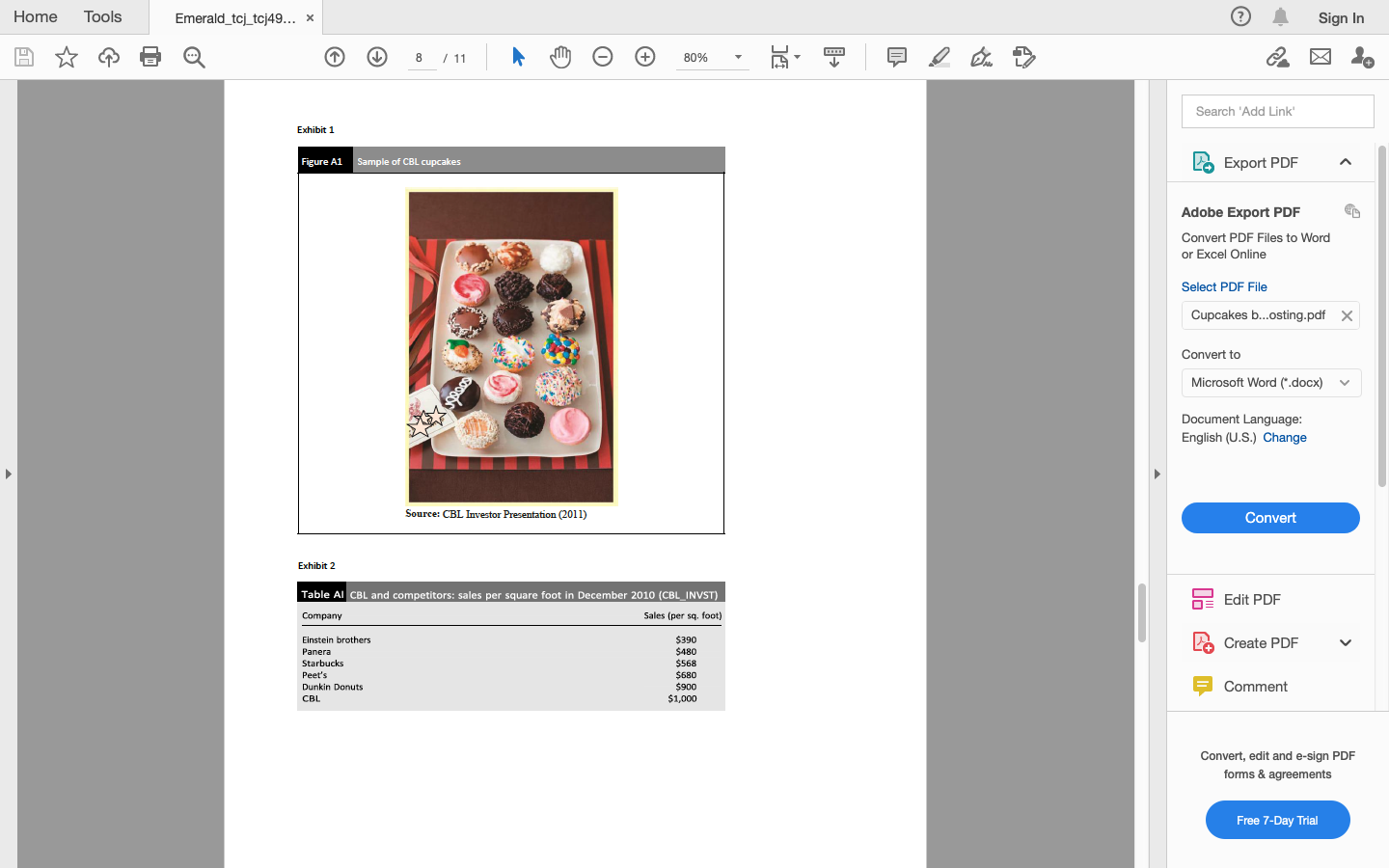

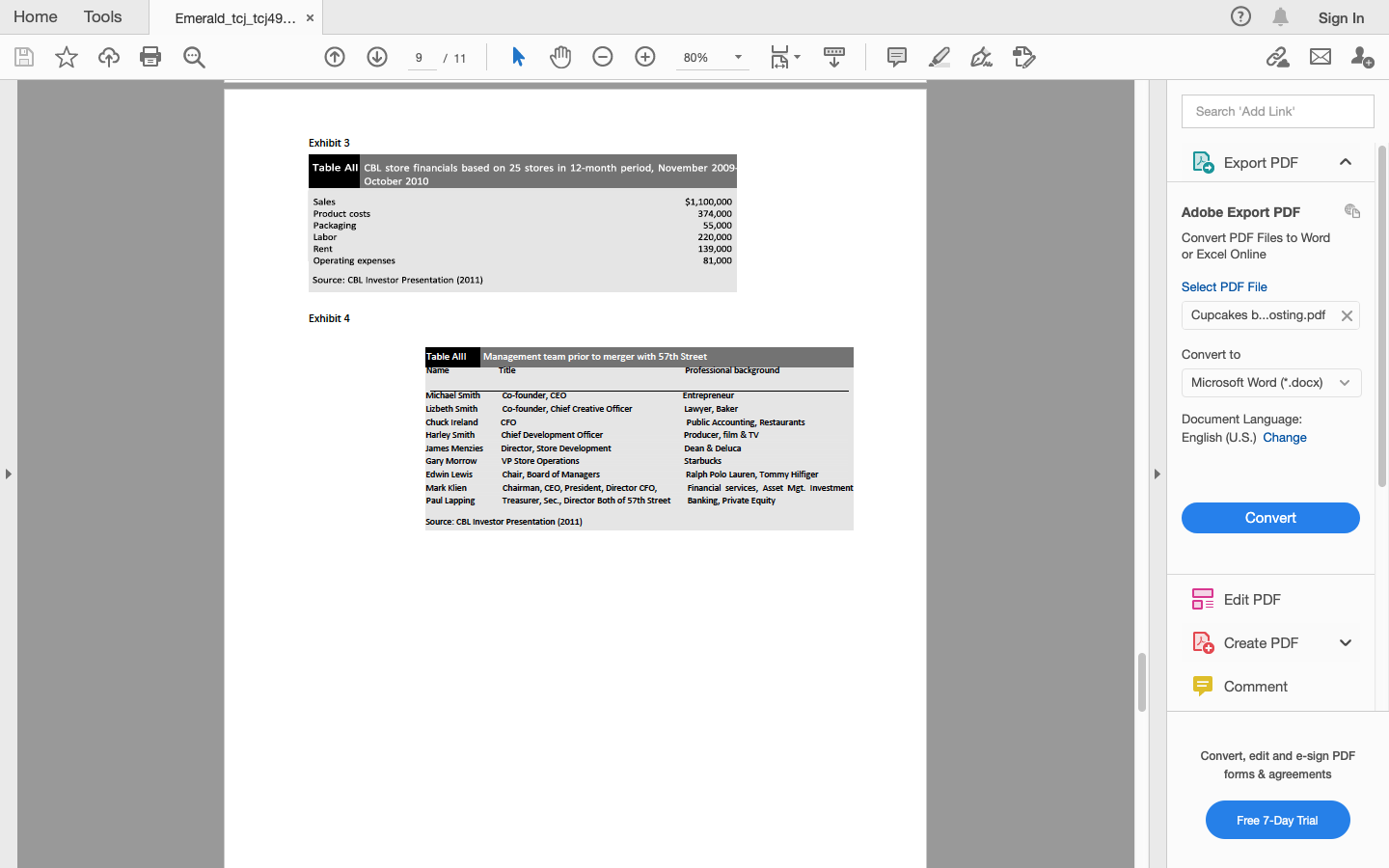

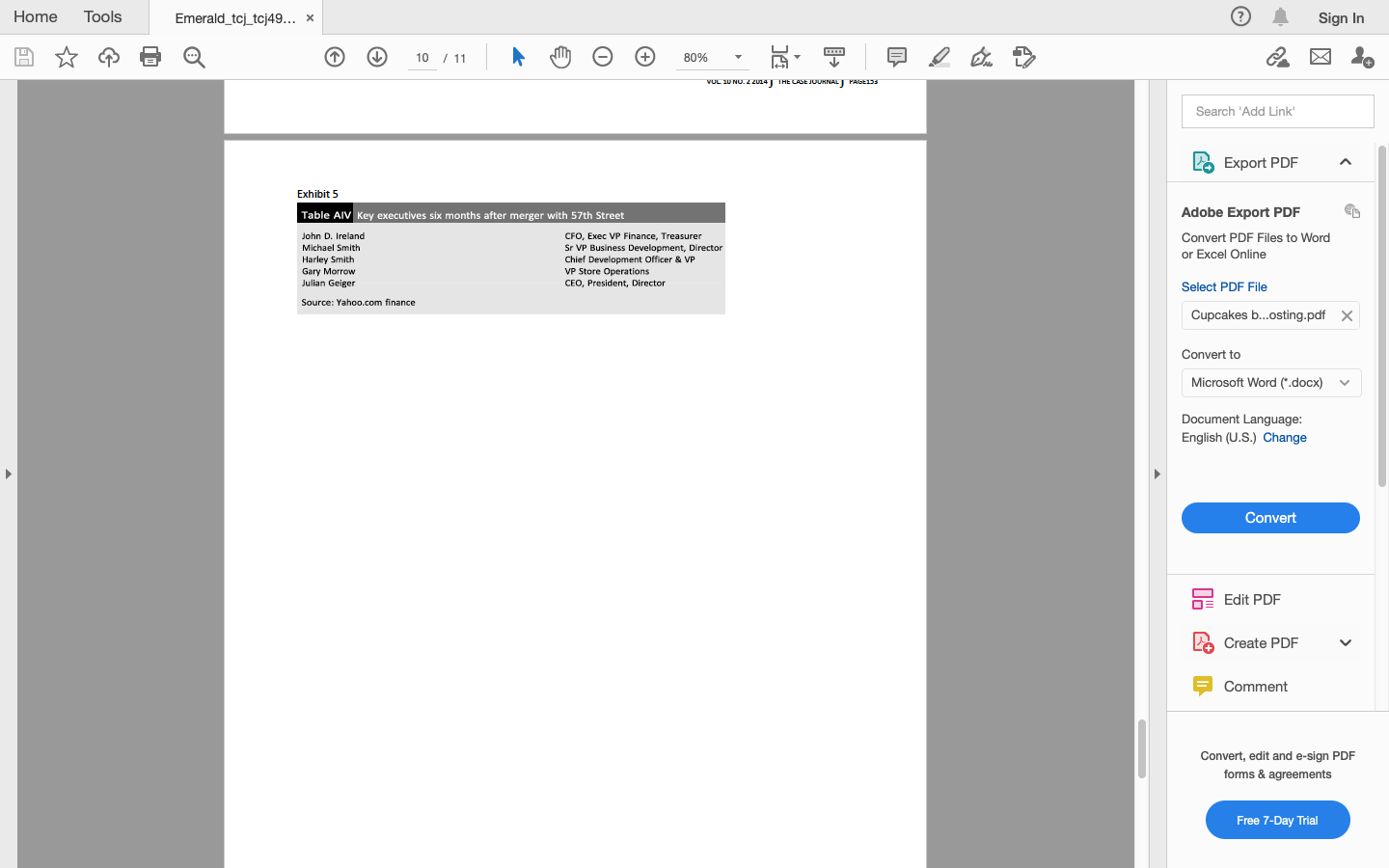

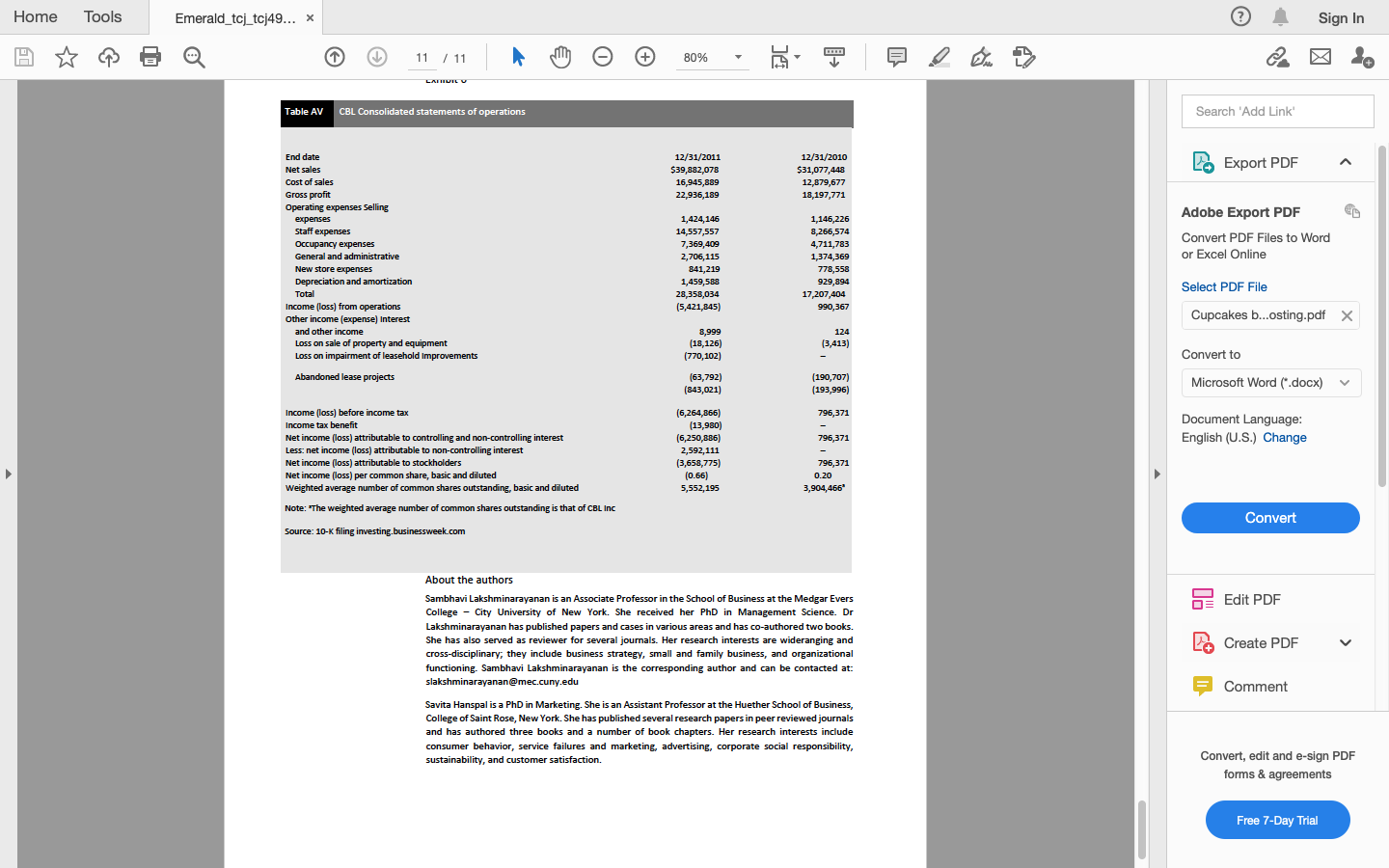

Home Tools Emerald_tcj_tcj49... * Sign In A 1 / 11 mo 90% 9 I Search 'Add Link Cupcakes by Lizbeth: flash in the baking pan or here to stay Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Sambhavi Lakshminarayanan and Savita Hanspal Sambhavi Lakshminarayanan A sweet history is an Associate Professor, Could anything have said "childhood" and brought back memories of a carefree time better than a based at Medgar Evers College/CUNY - Business simple sugary treat? Only something sweet, but also colorful and in a new and unexpected flavor Administration, Brooklyn, New could surpass it! York, USA. The "Cupcakes by Lizbeth" (CBL)[1] story embodied the desire of every person who ever dreamed Savita Hanspal is based at of converting a passionate hobby into a successful business enterprise. Michael and Lizbeth Smith College of St Rose-Heuther opened the first CBL location on New York's Upper West side in 2003. The store quickly became School of Business, Albany, New York, USA. popular for its cupcakes made from Lizbeth's old family recipes. With the registered trademark Made by Hand, Baked with Loves, the product appeared to tap into a yearning for nostalgia and comfort. Customers flocked to buy the lavishly decorated cupcakes, some with whimsical names. A reporter described CBL's offerings as "really big, delicious cupcakes with amazing icing toppings[2]." The company experienced success early, and the Smiths seemed determined to build CBL into a large competitor within the cupcake marketplace. Eight years after the first store was opened, CBL became a publicly traded company. In interviews with media prior to this event, the founders always mentioned plans to scale up and expand to multiple locations. Traditionally, becoming a publicly traded company was a step by which a business signaled intent to expand significantly. Rather than issuing an IPO, CBL chose an unusual "reverse merger[3]" route to becoming public (see section titled "A reverse merger and going public"). CBL's stock price debuted at a little over $13 and remained at that level for about eight months. Two years after going public, the company was in a situation that could be viewed as challenging. Significant changes had occurred in top management and the company had missed previously stated growth goals. The stock price had crashed down to near $4, hovering there for almost a year[4]. However, CBL was still a strong competitor in the marketplace, and analysts had noted that it had a good business model. These factors, mixed bag when put together, suggested that CBL was at a transitional phase of its existence. The CASE Association What happened at CBL in the near-term could well decide its long-term future. Internal pressures were pushing toward change and external forces driving toward growth. The company seemed faced with existential questions of success and survival. This included the essential question Disclaimer. This case is written solely regarding whether CBL had merely been a flash in the baking pan or if it was here to stay, a winner for educational purposes and is not intended to represent successful or in the cupcake wars. unsuccessful managerial decision making. The authors may have disguised names; financial and other Cupcakes for everyone: the marketplace recognizable information to protect confidentiality Cupcakes were not a new food item, having been around for many years. By some accounts cupcakes were invented in the nineteenth century[5]. In recent years, more than one industry Edit PDF Create PDF TCASE Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 4 / 11 mg 0 80% BC Search 'Add Link P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) CBL's stores were bright, well-lit and colorful. CBL's cupcakes came in a variety of flavors and decorative esigns (see Exhibit 1). CBL offered several innovative and distinctive types of cupcakes - such as "Blackbottom Cheesecake" and "Caramel Apple." Sizes of cupcakes sold at CBL ranged from small to large; a small cupcake was almost a miniature and could be eaten in a bite or two whereas a large cupcake was huge and could easily be shared. A box of a dozen small cupcakes, which measured about an inch across, was priced at $18. A medium, called "classic" by CBL, was comparable to the size usually sold in mass retail. It measured about two and half inches across and was priced at a little under four dollars. A large cupcake, called the "signature" size, was about three inches across and four inches tall. This size was priced at about six dollars. According to the company, customers spent an average of $18-$20 per sale at a CBL store. Almost 80 percent of total sales revenue was reported to come from sales of cupcakes[18]. CBL made a strategic choice to use contract manufacturing for producing its cupcakes. CBL had agreements with several regional commercial baked goods manufacturers to supply cupcakes to various retail store locations. In manufacturing contracts the manufacturer produced, and sometimes shipped, products for the client; the client company did not need to maintain manufacturing facilities, purchase raw materials or employ a production workforce. CBL's production strategy was in sharp contrast to that of its rivals. Steve Abrams, owner of Magnolia Bakery, had this to say regarding CBL's use of contract manufacturing: "CBL is not a bakery. They are a retail store for baked goods made somewhere else by third parties" (see footnote 13). The food reporter Helm (see footnote 7) said something similar: "not one of CBL's bakeries is really a bakery" and that "not one has, or ever has had, an oven," adding that the business was "built for efficiency." Thus, CBL's store operations would be geared toward placing orders, receiving deliveries and displaying items for sale. The strategic choice of not baking in-store had certain important functional implications: for instance, there was no need to have baking equipment inside stores nor to install special venting equipment that might be required legally were cooking to be done. CBL did not advertise in the media, relying instead on word-of-mouth publicity and free cupcake giveaways at new store openings as means to promote the product. CBL positioned itself as a business that offered a special product that almost everyone wanted. In the initial presentation to investors, CBL's management identified several segments of the general population as customers, listing them as "moms/strollers, tastemakers, office workers and managers, celebrities, everyone in between." The company's claim that CBL's cupcakes appealed to a variety of consumers was supported by data showing steady store traffic almost through the day, with a small bump in the afternoon (see footnote 18). Apart from cupcakes, CBL also sold beverages like coffees, teas and homemade sodas. Like many entrepreneurs, Lizbeth Smith had entered the business with interest born out of passion - in her case, for baking cupcakes (see footnote 2). She had been professionally trained as a lawyer and had worked for the city of New York before starting CBL Michael Smith had worked in his family owned food distribution business. He gained further experience in the food industry starting a venture called "Famous Fixins" in 1995(19). Seven years after the first CBL store opened, Inc Magazine listed CBL as one of the fastestgrowing companies in the food and beverage industry in 2010[20]. In an interview, Michael Smith stated that based on revenue growth of the business, his view was that demand for gourmet cupcakes was not just a fad or a trend but likely to be long-lasting[21]. He cited this as a rationale for justifying the company's expansion plans. In 2011 the Smiths were named Ernst and Young Entrepreneur of the Year 2011 New York Award winners[22]. Such public endorsements and favorable publicity in the media contributed to increasing name recognition and brand equity. It seemed that CBL could leverage this to its advantage and use a strategy of rapid expansion to gain a first mover advantage in untapped markets. Document Language: English (U.S.) Change Convert Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements After opening the first store in 2003, CBL had added seven more stores by 2008 and was selling 75,000 cupcakes per week [23]. In an interview in 2009, Michael Smith claimed that the business had a high growth rate of 20 percent post-recession and planned to expand to 25 stores by year-end, with entry into new markets like Boston, Philadelphia and South Jersey in 2010[24]. In fact, CBL had Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In BORE I 5 / 11 my 0 80% IDL Search 'Add Link P. Export PDF 23 outlets functioning by the end of the year: 18 on the East Coast and five on the West[25]. Also in 2010, CBL had sold about 13 million cupcakes, and had revenues of more than $30 million with an EBITDA of $2.5 million (see footnote 21). By the beginning of 2011 CBL had 34 outlets spread over six states and Washington, DC. Additionally, CBL ran a mail-order service that was recommended as making "perfect gifts for the holidays, a nice dessert for a special dinner party or a treat to send a college student[26]." The company expanded further to 45 locations by the end of 2011[27] and announced a strategic goal of growing to 200 outlets by the year 2014[28]. In the stated strategy, CBL identified locations such as train and air terminals as first round sites. There were plans to open more stores in current areas as well and subsequent expansion would include other states, particularly in the South and Southwest USA (see footnote 21). All CBL outlets were company owned. Eight years after opening, the company indicated that there were no immediate plans to offer franchise opportunities, issue licenses or expand to international locations (see footnote 16). CBL promoted several advantages of its business model including the low cost of building stores, the relatively small size of stores and the higher sales per square foot. According to industry data as quoted in CBL's presentation to prospective investors, a comparison with rivals showed that sales-per-square-foot at CBL was almost double that at Starbucks and Panera's. Among the rivals considered, the closest competitor to CBL was Dunkin Donuts, with sales per square foot of $900, as compared to $1000 for CBL (see Exhibit 2). A comparable business, although not identified as a competitor by CBL, was Auntie Anne's Pretzels. Like CBL it was highly focussed on a single food item. Auntie Anne's store revenues per square foot were comparable to that of CBL, although they varied widely between $545 and $1200 and were highly location specific Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Edit PDF A reverse merger and going public As with most young businesses, the way to facilitate further, more rapid growth seemed to point to the direction for going public. Attached prestige of being traded on a well-known stock exchange would provide means to attract greater numbers of investors. The company would then have greater access to capital and could respond faster to take advantage of opportunities for growth. On the other hand, becoming public had the downside in that it meant being open to a greater degree of scrutiny. Private companies could keep information confidential, especially sensitive financial data, to an extent that public companies could not. CBL became a publicly traded company eight years after it was started. CBL chose to utilize the method of merging with a "blank check company" to facilitate that process. Michael Smith had used this technique in Famous Fixins, his earlier venture. Famous Fixins had developed concepts of celebrity related products and sold these specialty items through various retail outlets, including giant ones such as Walmart. It had started with a salad dressing whose recipe was provided by the actress Olympia Dukakis. This was reportedly an old recipe from her family and she was persuaded to commercialize it by Famous Fixins agreeing to donate part of the proceeds to a charity of her choice. Other celebrities that had associated specialty items marketed by the company included Derek Jeter and Cal Ripken [29]. In order for Famous Fixins to be traded on the stock market, under the symbol FIXN, and to fulfill certain requirements of the stock exchange, the company had first been sold to a "shell" company of a similar name. From all accounts, Famous Fixins appeared to have been successful, although it did have powerful competitors with the same basic concept, such as PLB based in Pittsburgh. In 2003, Famous Fixins had merged with Warning Model Management, an LLC that served as an agency for models. The name of Famous Fixins was then changed to the Warning Model Management Inc with a new trading symbol WNMI[30]. CBL followed a similar path to becoming public. By 2008, CBL had received an "eight figure investment" from an executive in the apparel business (see footnote 28). A blank check company called the 57th Street General Acquisition Corporation was created in Delaware in 2009. After its creation, 57th Street went through an IPO and raised more than $54 million from investors. In 2011, the private company CBL merged into the public company 57th Street and acquired all of the latter's stock. The name of the merged public company was changed to CBL. Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 6 / 11 mg 80% Search 'Add Link The board of directors of the merged company included board members from both 57th Street and CBL. Michael Smith was the new CEO. For the transaction that resulted in the establishment of the public company CBL, the Smiths reportedly received $27 million in cash along with stock[31]. The SEC defined a blank check company as a "development stage company that has no specific business plan or purpose or has indicated its business plan is to engage in a merger or acquisition with an unidentified company or companies, other entity, or person[32]." A blank check company was a corporate shell that did not have any assets or liabilities, its only purpose was to raise money. Following the merger into 57th Street the stock began trading the New York Stock Exchange. A reverse merger, such as this, provided means for a company to go public without doing an IPO using an underwriter. In a reverse merger process, the company would not have to go through certain regulatory scrutiny that was a required part of an IPO process[33]. P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online The road ahead Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert CBL was considered the "most corporate" among the specialty cupcake companies food writer Helm (see footnote 7). Historically, public announcements by CBL had always portrayed it as being poised for strong growth. In communications to (potential) investors, the company asserted that "we appeal to everyone from age 8-80 in every socio-economic class and that the business was a "proven success in urban, suburban, commercial and residential areas," with a strong track record of revenue growth. Further, the company's communication had stated that store transactions indicated that the business could have an "initial expansion to a planned 200 locations in the top 15 markets by year-end 2014" (see footnote 18). There was no publicly articulated vision or mission statement made available by the company. When CBL started being traded publicly, there were both supporters and detractors of the stock. Some market observers wondered if going public was a hasty move and whether the stock might go the way Krispy Kreme. A seemingly successful company, Krispy Kreme had a singular focus on donuts and an IPO in 2000. By 2003 Krispy Kreme had seen its shares rapidly rise to $49.75. However, the share price then fell precipitously and by 2009 Krispy Kreme had become a penny stock. The company's overly rapid expansion had been blamed for the downfall and the company never quite recovered from the crash of the stock price[34]. Observers also expressed doubts about the resilience of the overall cupcake market. An investment strategist stated lack of confidence in cupcake demand as a whole and said he would not invest in CBL even though he liked the product (see footnote 16). A restaurant analyst's opinion was that the CBL business model was interesting but had "a narrow focus," that in this industry it was "difficult build a business on a [y] single day-part occasion" and that CBL'S EBITDA was "very thin" (see footnote 28). In comments before becoming publicly traded, Michael Smith did announce a goal to improve EBITDA tenfold within three years, that is, by end of 2014 (see footnote 7). An investment advisor, Katje[35], identified CBL Holding as an overlooked stock and recommended it as a "speculative" buy. Restaurant consultant Arlene Spiegel was quoted as saying that the choice CBL made of becoming public would "capture the attention of the public market" and encourage other food businesses to go public (see footnote 31). CBL was said to have a "business model that works" by a business consultant and commentator[36]. The company's own presentation to prospective investors showed data to illustrate that most store space was revenue generating (see Exhibit 2), that stores financials were good (see Exhibit 3) and that the product had wide appeal. On June 30, 2011, CBL went public on Nasdaq and the stock opened at $13.10, giving the company a market valuation of $59 million (see footnote 16). Following the stock exchange debut, the stock price rose above $14 midyear, but had fallen to $4 by year-end. Third quarter earnings were announced in November, and shortly thereafter, the company announced that it would suspend guidance for 2011 net sales. In addition, there was an announcement about change in the top management position: Michael Smith, a co-founder of CBL, Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In BBBB I 7 / 11 mo 0 80% IL 9 Search 'Add Link P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X would no longer be CEO. He would instead assume responsibilities as Senior Vice President Business Development. The new CEO was Julian R. Geiger, who had led the clothing retailer Aeropostale in the past and had experience in merchandising. As outgoing CEO, Michael Smith acknowledged that the company had underperformed and that there was a need to improve[37]. In the third quarter of 2011, four new stores were opened, bringing the total number of outlets to 48. In all, 15 new stores were opened in 2011. The company's 10-K filing for the period ending December 31, 2011 stated that it planned to open around nine new stores in 2012. In announcements before becoming publicly traded, the company had stated plans to have 200 stores in operation by 2014. In terms of financial results, the company posted a loss during 2011. This was explained as being unavoidable since that year was a transition period [38]. There was no mention of a change in targets; the company continued to talk about growth[39]. When questioned at a scheduled conference call after announcement of quarterly financial results about disappointing financial performance and also change at the top position, the company spokesperson said that weather related disruptions caused by the Irene storm were the reason for the former and did not elaborate on reasons for the latter[40]. An announcement regarding suspension of guidance by a company could be interpreted as unwillingness to discuss details of performance. Typically, corporate communications to the investor community could be in the form of "guidance" or in terms of "forward looking information." Guidance included a set of specific and quantitative numbers that could serve targets for future performance. Forward looking information referred to broader goals and even strategies. Even as CBL negotiated its way with becoming public and expanding, direct and indirect competitors were busy making their moves. Although supermarkets and big grocery stores had seen little increase in consumer spending in stores, total food spending in the country was expected to increase by almost 10 percent[41]. Consumers were increasingly becoming used to getting differentiated, even customized food products[42]. Businesses with the ability to produce and distribute variety in food products were likely to experience good consumer response. With regard to cupcakes, groceries, big retailers and general bakeries continued to sell old-fashioned versions, but some added cheaper versions of the "gourmet" cupcakes sold by the specialists such as CBL and Sprinkles to their product lines. Cupcake-focussed businesses also continued to expand. Under these circumstances, and given that CBL was the largest among cupcake-focussed businesses, it was worth examining CBL's positioning in the market place and current business strategy. Was the strategy working out well for the business? What did the future look like for CBL? Finally, could CBL be the winner in the cupcake wars? Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 1 8 / 11 my o 80% DC 1 Search 'Add Link Exhibit 1 Figure A1 Sample of CBL cupcakes P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) V sooder Cat Document Language: English (U.S.) Change Source: CBL Investor Presentation (2011) Convert Exhibit 2 Table Al CBL and competitors: sales per square foot in December 2010 (CBL_INVST) Company Sales (per sq. foot) Edit PDF Po Create PDF Einstein brothers Panera Starbucks Peet's Dunkin Donuts CBL $390 $480 $568 $680 $900 $1,000 Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 9 / 11 cm o # 80% Den Search 'Add Link P. Export PDF Exhibit 3 Table All CBL store financials based on 25 stores in 12-month period, November 2009 October 2010 Sales $1,100,000 Product costs 374,000 Packaging 55,000 Labor 220,000 Rent 139,000 Operating expenses 81,000 Source: CBL Investor Presentation (2011) ) Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Exhibit 4 Cupcakes b...osting.pdf X Convert to Table All Management team prior to merger with 57th Street Name Title Professional background Microsoft Word (.docx) V Michael Smith Lizbeth Smith Chuck Ireland Harley Smith James Menzies Gary Morrow Edwin Lewis Mark Klien Paul Lapping Document Language: English (U.S.) Change Co-founder, CEO Co-founder, Chief Creative Officer CFO Chief Development Officer Director, Store Development VP Store Operations Chair, Board of Managers Chairman, CEO, President, Director CFO, Treasurer, Sec., Director Both of 57th Street Entrepreneur Lawyer, Baker Public Accounting, Restaurants Producer, film & TV Dean & Deluca Starbucks Ralph Polo Lauren, Tommy Hilfiger Financial services, Asset Mgt. Investment Banking, Private Equity Source: CBL Investor Presentation (2011) Convert Edit PDF Do Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 10 / 11 O 80% PL 1 VUL 20 NO. 2 2014) THE CASE JOURNAL PAGE235 Search 'Add Link P. Export PDF Exhibit 5 Table AIV Key executives six months after merger with 57th Street John D. Ireland CFO, Exec VP Finance, Treasurer Michael Smith Sr VP Business Development, Director Harley Smith Chief Development Officer & VP Gary Morrow VP Store Operations Julian Geiger CEO, President, Director Source: Yahoo.com finance Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) V Document Language: English (U.S.) Change Convert Edit PDF Po Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In A 11 / 11 o # 80% 9 LATHUILU Table AV CBL Consolidated statements of operations Search 'Add Link P. Export PDF 12/31/2011 $39,882,078 16,945,889 22,936,189 12/31/2010 $31,077,448 12,879,677 18,197,771 End date Net sales Cost of sales Gross profit Operating expenses Selling expenses Staff expenses Occupancy expenses General and administrative New store expenses Depreciation and amortization Total Income (loss) from operations Other income (expense) Interest and other income Loss on sale of property and equipment Loss on impairment of leasehold Improvements 1,424,146 14,557,557 7,369,409 2,706, 115 841,219 1,459,588 28,358,034 (5,421,845) Adobe Export PDF Convert PDF Files to Word or Excel Online 1,146,226 8,266,574 4,711,783 1,374,369 778,558 929,894 17,207,404 990,367 Select PDF File Cupcakes b...osting.pdf X 8,999 (18,126) (770,102) 124 (3,413) Convert to Abandoned lease projects 163,792) (843,021) (190,707) (193,996) Microsoft Word (.docx) V 796,371 Document Language: English (U.S.) Change 796,371 Income loss) before income tax Income tax benefit Net income (loss) attributable to controlling and non-controlling interest Less: net income (loss) attributable to non-controlling interest Net income (loss) attributable to stockholders Net income (loss) per common share, basic and diluted Weighted average number of common shares outstanding, basic and diluted : " Note: "The weighted average number of common shares outstanding is that of CBL Inc Source: 10-K filing investing.businessweek.com (6,264,866) (13,980) (6,250,886) 2,592,111 (3,658,775) (0.66) 5,552,195 796,371 0.20 3,904,466 Convert About the authors Edit PDF Po Create PDF Sambhavi Lakshminarayanan is an Associate Professor in the School of Business at the Medgar Evers College - City University of New York. She received her PhD in Management Science. Dr Lakshminarayanan has published papers and cases in various areas and has co-authored two books. She has also served as reviewer for several journals. Her research interests are wideranging and cross-disciplinary, they include business strategy, small and family business, and organizational functioning. Sambhavi Lakshminarayanan is the corresponding author and can be contacted at: slakshminarayanan@mec.cuny.edu Savita Hanspal is a PhD in Marketing. She is an Assistant Professor at the Huether School of Business, , College of Saint Rose, New York. She has published several research papers in peer reviewed journals and has authored three books and a number of book chapters. Her research interests include consumer behavior, service failures and marketing, advertising, corporate social responsibility, sustainability, and customer satisfaction. Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... * Sign In A 1 / 11 mo 90% 9 I Search 'Add Link Cupcakes by Lizbeth: flash in the baking pan or here to stay Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Sambhavi Lakshminarayanan and Savita Hanspal Sambhavi Lakshminarayanan A sweet history is an Associate Professor, Could anything have said "childhood" and brought back memories of a carefree time better than a based at Medgar Evers College/CUNY - Business simple sugary treat? Only something sweet, but also colorful and in a new and unexpected flavor Administration, Brooklyn, New could surpass it! York, USA. The "Cupcakes by Lizbeth" (CBL)[1] story embodied the desire of every person who ever dreamed Savita Hanspal is based at of converting a passionate hobby into a successful business enterprise. Michael and Lizbeth Smith College of St Rose-Heuther opened the first CBL location on New York's Upper West side in 2003. The store quickly became School of Business, Albany, New York, USA. popular for its cupcakes made from Lizbeth's old family recipes. With the registered trademark Made by Hand, Baked with Loves, the product appeared to tap into a yearning for nostalgia and comfort. Customers flocked to buy the lavishly decorated cupcakes, some with whimsical names. A reporter described CBL's offerings as "really big, delicious cupcakes with amazing icing toppings[2]." The company experienced success early, and the Smiths seemed determined to build CBL into a large competitor within the cupcake marketplace. Eight years after the first store was opened, CBL became a publicly traded company. In interviews with media prior to this event, the founders always mentioned plans to scale up and expand to multiple locations. Traditionally, becoming a publicly traded company was a step by which a business signaled intent to expand significantly. Rather than issuing an IPO, CBL chose an unusual "reverse merger[3]" route to becoming public (see section titled "A reverse merger and going public"). CBL's stock price debuted at a little over $13 and remained at that level for about eight months. Two years after going public, the company was in a situation that could be viewed as challenging. Significant changes had occurred in top management and the company had missed previously stated growth goals. The stock price had crashed down to near $4, hovering there for almost a year[4]. However, CBL was still a strong competitor in the marketplace, and analysts had noted that it had a good business model. These factors, mixed bag when put together, suggested that CBL was at a transitional phase of its existence. The CASE Association What happened at CBL in the near-term could well decide its long-term future. Internal pressures were pushing toward change and external forces driving toward growth. The company seemed faced with existential questions of success and survival. This included the essential question Disclaimer. This case is written solely regarding whether CBL had merely been a flash in the baking pan or if it was here to stay, a winner for educational purposes and is not intended to represent successful or in the cupcake wars. unsuccessful managerial decision making. The authors may have disguised names; financial and other Cupcakes for everyone: the marketplace recognizable information to protect confidentiality Cupcakes were not a new food item, having been around for many years. By some accounts cupcakes were invented in the nineteenth century[5]. In recent years, more than one industry Edit PDF Create PDF TCASE Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 4 / 11 mg 0 80% BC Search 'Add Link P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) CBL's stores were bright, well-lit and colorful. CBL's cupcakes came in a variety of flavors and decorative esigns (see Exhibit 1). CBL offered several innovative and distinctive types of cupcakes - such as "Blackbottom Cheesecake" and "Caramel Apple." Sizes of cupcakes sold at CBL ranged from small to large; a small cupcake was almost a miniature and could be eaten in a bite or two whereas a large cupcake was huge and could easily be shared. A box of a dozen small cupcakes, which measured about an inch across, was priced at $18. A medium, called "classic" by CBL, was comparable to the size usually sold in mass retail. It measured about two and half inches across and was priced at a little under four dollars. A large cupcake, called the "signature" size, was about three inches across and four inches tall. This size was priced at about six dollars. According to the company, customers spent an average of $18-$20 per sale at a CBL store. Almost 80 percent of total sales revenue was reported to come from sales of cupcakes[18]. CBL made a strategic choice to use contract manufacturing for producing its cupcakes. CBL had agreements with several regional commercial baked goods manufacturers to supply cupcakes to various retail store locations. In manufacturing contracts the manufacturer produced, and sometimes shipped, products for the client; the client company did not need to maintain manufacturing facilities, purchase raw materials or employ a production workforce. CBL's production strategy was in sharp contrast to that of its rivals. Steve Abrams, owner of Magnolia Bakery, had this to say regarding CBL's use of contract manufacturing: "CBL is not a bakery. They are a retail store for baked goods made somewhere else by third parties" (see footnote 13). The food reporter Helm (see footnote 7) said something similar: "not one of CBL's bakeries is really a bakery" and that "not one has, or ever has had, an oven," adding that the business was "built for efficiency." Thus, CBL's store operations would be geared toward placing orders, receiving deliveries and displaying items for sale. The strategic choice of not baking in-store had certain important functional implications: for instance, there was no need to have baking equipment inside stores nor to install special venting equipment that might be required legally were cooking to be done. CBL did not advertise in the media, relying instead on word-of-mouth publicity and free cupcake giveaways at new store openings as means to promote the product. CBL positioned itself as a business that offered a special product that almost everyone wanted. In the initial presentation to investors, CBL's management identified several segments of the general population as customers, listing them as "moms/strollers, tastemakers, office workers and managers, celebrities, everyone in between." The company's claim that CBL's cupcakes appealed to a variety of consumers was supported by data showing steady store traffic almost through the day, with a small bump in the afternoon (see footnote 18). Apart from cupcakes, CBL also sold beverages like coffees, teas and homemade sodas. Like many entrepreneurs, Lizbeth Smith had entered the business with interest born out of passion - in her case, for baking cupcakes (see footnote 2). She had been professionally trained as a lawyer and had worked for the city of New York before starting CBL Michael Smith had worked in his family owned food distribution business. He gained further experience in the food industry starting a venture called "Famous Fixins" in 1995(19). Seven years after the first CBL store opened, Inc Magazine listed CBL as one of the fastestgrowing companies in the food and beverage industry in 2010[20]. In an interview, Michael Smith stated that based on revenue growth of the business, his view was that demand for gourmet cupcakes was not just a fad or a trend but likely to be long-lasting[21]. He cited this as a rationale for justifying the company's expansion plans. In 2011 the Smiths were named Ernst and Young Entrepreneur of the Year 2011 New York Award winners[22]. Such public endorsements and favorable publicity in the media contributed to increasing name recognition and brand equity. It seemed that CBL could leverage this to its advantage and use a strategy of rapid expansion to gain a first mover advantage in untapped markets. Document Language: English (U.S.) Change Convert Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements After opening the first store in 2003, CBL had added seven more stores by 2008 and was selling 75,000 cupcakes per week [23]. In an interview in 2009, Michael Smith claimed that the business had a high growth rate of 20 percent post-recession and planned to expand to 25 stores by year-end, with entry into new markets like Boston, Philadelphia and South Jersey in 2010[24]. In fact, CBL had Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In BORE I 5 / 11 my 0 80% IDL Search 'Add Link P. Export PDF 23 outlets functioning by the end of the year: 18 on the East Coast and five on the West[25]. Also in 2010, CBL had sold about 13 million cupcakes, and had revenues of more than $30 million with an EBITDA of $2.5 million (see footnote 21). By the beginning of 2011 CBL had 34 outlets spread over six states and Washington, DC. Additionally, CBL ran a mail-order service that was recommended as making "perfect gifts for the holidays, a nice dessert for a special dinner party or a treat to send a college student[26]." The company expanded further to 45 locations by the end of 2011[27] and announced a strategic goal of growing to 200 outlets by the year 2014[28]. In the stated strategy, CBL identified locations such as train and air terminals as first round sites. There were plans to open more stores in current areas as well and subsequent expansion would include other states, particularly in the South and Southwest USA (see footnote 21). All CBL outlets were company owned. Eight years after opening, the company indicated that there were no immediate plans to offer franchise opportunities, issue licenses or expand to international locations (see footnote 16). CBL promoted several advantages of its business model including the low cost of building stores, the relatively small size of stores and the higher sales per square foot. According to industry data as quoted in CBL's presentation to prospective investors, a comparison with rivals showed that sales-per-square-foot at CBL was almost double that at Starbucks and Panera's. Among the rivals considered, the closest competitor to CBL was Dunkin Donuts, with sales per square foot of $900, as compared to $1000 for CBL (see Exhibit 2). A comparable business, although not identified as a competitor by CBL, was Auntie Anne's Pretzels. Like CBL it was highly focussed on a single food item. Auntie Anne's store revenues per square foot were comparable to that of CBL, although they varied widely between $545 and $1200 and were highly location specific Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Edit PDF A reverse merger and going public As with most young businesses, the way to facilitate further, more rapid growth seemed to point to the direction for going public. Attached prestige of being traded on a well-known stock exchange would provide means to attract greater numbers of investors. The company would then have greater access to capital and could respond faster to take advantage of opportunities for growth. On the other hand, becoming public had the downside in that it meant being open to a greater degree of scrutiny. Private companies could keep information confidential, especially sensitive financial data, to an extent that public companies could not. CBL became a publicly traded company eight years after it was started. CBL chose to utilize the method of merging with a "blank check company" to facilitate that process. Michael Smith had used this technique in Famous Fixins, his earlier venture. Famous Fixins had developed concepts of celebrity related products and sold these specialty items through various retail outlets, including giant ones such as Walmart. It had started with a salad dressing whose recipe was provided by the actress Olympia Dukakis. This was reportedly an old recipe from her family and she was persuaded to commercialize it by Famous Fixins agreeing to donate part of the proceeds to a charity of her choice. Other celebrities that had associated specialty items marketed by the company included Derek Jeter and Cal Ripken [29]. In order for Famous Fixins to be traded on the stock market, under the symbol FIXN, and to fulfill certain requirements of the stock exchange, the company had first been sold to a "shell" company of a similar name. From all accounts, Famous Fixins appeared to have been successful, although it did have powerful competitors with the same basic concept, such as PLB based in Pittsburgh. In 2003, Famous Fixins had merged with Warning Model Management, an LLC that served as an agency for models. The name of Famous Fixins was then changed to the Warning Model Management Inc with a new trading symbol WNMI[30]. CBL followed a similar path to becoming public. By 2008, CBL had received an "eight figure investment" from an executive in the apparel business (see footnote 28). A blank check company called the 57th Street General Acquisition Corporation was created in Delaware in 2009. After its creation, 57th Street went through an IPO and raised more than $54 million from investors. In 2011, the private company CBL merged into the public company 57th Street and acquired all of the latter's stock. The name of the merged public company was changed to CBL. Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 6 / 11 mg 80% Search 'Add Link The board of directors of the merged company included board members from both 57th Street and CBL. Michael Smith was the new CEO. For the transaction that resulted in the establishment of the public company CBL, the Smiths reportedly received $27 million in cash along with stock[31]. The SEC defined a blank check company as a "development stage company that has no specific business plan or purpose or has indicated its business plan is to engage in a merger or acquisition with an unidentified company or companies, other entity, or person[32]." A blank check company was a corporate shell that did not have any assets or liabilities, its only purpose was to raise money. Following the merger into 57th Street the stock began trading the New York Stock Exchange. A reverse merger, such as this, provided means for a company to go public without doing an IPO using an underwriter. In a reverse merger process, the company would not have to go through certain regulatory scrutiny that was a required part of an IPO process[33]. P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online The road ahead Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert CBL was considered the "most corporate" among the specialty cupcake companies food writer Helm (see footnote 7). Historically, public announcements by CBL had always portrayed it as being poised for strong growth. In communications to (potential) investors, the company asserted that "we appeal to everyone from age 8-80 in every socio-economic class and that the business was a "proven success in urban, suburban, commercial and residential areas," with a strong track record of revenue growth. Further, the company's communication had stated that store transactions indicated that the business could have an "initial expansion to a planned 200 locations in the top 15 markets by year-end 2014" (see footnote 18). There was no publicly articulated vision or mission statement made available by the company. When CBL started being traded publicly, there were both supporters and detractors of the stock. Some market observers wondered if going public was a hasty move and whether the stock might go the way Krispy Kreme. A seemingly successful company, Krispy Kreme had a singular focus on donuts and an IPO in 2000. By 2003 Krispy Kreme had seen its shares rapidly rise to $49.75. However, the share price then fell precipitously and by 2009 Krispy Kreme had become a penny stock. The company's overly rapid expansion had been blamed for the downfall and the company never quite recovered from the crash of the stock price[34]. Observers also expressed doubts about the resilience of the overall cupcake market. An investment strategist stated lack of confidence in cupcake demand as a whole and said he would not invest in CBL even though he liked the product (see footnote 16). A restaurant analyst's opinion was that the CBL business model was interesting but had "a narrow focus," that in this industry it was "difficult build a business on a [y] single day-part occasion" and that CBL'S EBITDA was "very thin" (see footnote 28). In comments before becoming publicly traded, Michael Smith did announce a goal to improve EBITDA tenfold within three years, that is, by end of 2014 (see footnote 7). An investment advisor, Katje[35], identified CBL Holding as an overlooked stock and recommended it as a "speculative" buy. Restaurant consultant Arlene Spiegel was quoted as saying that the choice CBL made of becoming public would "capture the attention of the public market" and encourage other food businesses to go public (see footnote 31). CBL was said to have a "business model that works" by a business consultant and commentator[36]. The company's own presentation to prospective investors showed data to illustrate that most store space was revenue generating (see Exhibit 2), that stores financials were good (see Exhibit 3) and that the product had wide appeal. On June 30, 2011, CBL went public on Nasdaq and the stock opened at $13.10, giving the company a market valuation of $59 million (see footnote 16). Following the stock exchange debut, the stock price rose above $14 midyear, but had fallen to $4 by year-end. Third quarter earnings were announced in November, and shortly thereafter, the company announced that it would suspend guidance for 2011 net sales. In addition, there was an announcement about change in the top management position: Michael Smith, a co-founder of CBL, Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In BBBB I 7 / 11 mo 0 80% IL 9 Search 'Add Link P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X would no longer be CEO. He would instead assume responsibilities as Senior Vice President Business Development. The new CEO was Julian R. Geiger, who had led the clothing retailer Aeropostale in the past and had experience in merchandising. As outgoing CEO, Michael Smith acknowledged that the company had underperformed and that there was a need to improve[37]. In the third quarter of 2011, four new stores were opened, bringing the total number of outlets to 48. In all, 15 new stores were opened in 2011. The company's 10-K filing for the period ending December 31, 2011 stated that it planned to open around nine new stores in 2012. In announcements before becoming publicly traded, the company had stated plans to have 200 stores in operation by 2014. In terms of financial results, the company posted a loss during 2011. This was explained as being unavoidable since that year was a transition period [38]. There was no mention of a change in targets; the company continued to talk about growth[39]. When questioned at a scheduled conference call after announcement of quarterly financial results about disappointing financial performance and also change at the top position, the company spokesperson said that weather related disruptions caused by the Irene storm were the reason for the former and did not elaborate on reasons for the latter[40]. An announcement regarding suspension of guidance by a company could be interpreted as unwillingness to discuss details of performance. Typically, corporate communications to the investor community could be in the form of "guidance" or in terms of "forward looking information." Guidance included a set of specific and quantitative numbers that could serve targets for future performance. Forward looking information referred to broader goals and even strategies. Even as CBL negotiated its way with becoming public and expanding, direct and indirect competitors were busy making their moves. Although supermarkets and big grocery stores had seen little increase in consumer spending in stores, total food spending in the country was expected to increase by almost 10 percent[41]. Consumers were increasingly becoming used to getting differentiated, even customized food products[42]. Businesses with the ability to produce and distribute variety in food products were likely to experience good consumer response. With regard to cupcakes, groceries, big retailers and general bakeries continued to sell old-fashioned versions, but some added cheaper versions of the "gourmet" cupcakes sold by the specialists such as CBL and Sprinkles to their product lines. Cupcake-focussed businesses also continued to expand. Under these circumstances, and given that CBL was the largest among cupcake-focussed businesses, it was worth examining CBL's positioning in the market place and current business strategy. Was the strategy working out well for the business? What did the future look like for CBL? Finally, could CBL be the winner in the cupcake wars? Convert to Microsoft Word (.docx) Document Language: English (U.S.) Change Convert Edit PDF Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 1 8 / 11 my o 80% DC 1 Search 'Add Link Exhibit 1 Figure A1 Sample of CBL cupcakes P. Export PDF Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) V sooder Cat Document Language: English (U.S.) Change Source: CBL Investor Presentation (2011) Convert Exhibit 2 Table Al CBL and competitors: sales per square foot in December 2010 (CBL_INVST) Company Sales (per sq. foot) Edit PDF Po Create PDF Einstein brothers Panera Starbucks Peet's Dunkin Donuts CBL $390 $480 $568 $680 $900 $1,000 Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 9 / 11 cm o # 80% Den Search 'Add Link P. Export PDF Exhibit 3 Table All CBL store financials based on 25 stores in 12-month period, November 2009 October 2010 Sales $1,100,000 Product costs 374,000 Packaging 55,000 Labor 220,000 Rent 139,000 Operating expenses 81,000 Source: CBL Investor Presentation (2011) ) Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Exhibit 4 Cupcakes b...osting.pdf X Convert to Table All Management team prior to merger with 57th Street Name Title Professional background Microsoft Word (.docx) V Michael Smith Lizbeth Smith Chuck Ireland Harley Smith James Menzies Gary Morrow Edwin Lewis Mark Klien Paul Lapping Document Language: English (U.S.) Change Co-founder, CEO Co-founder, Chief Creative Officer CFO Chief Development Officer Director, Store Development VP Store Operations Chair, Board of Managers Chairman, CEO, President, Director CFO, Treasurer, Sec., Director Both of 57th Street Entrepreneur Lawyer, Baker Public Accounting, Restaurants Producer, film & TV Dean & Deluca Starbucks Ralph Polo Lauren, Tommy Hilfiger Financial services, Asset Mgt. Investment Banking, Private Equity Source: CBL Investor Presentation (2011) Convert Edit PDF Do Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In I 10 / 11 O 80% PL 1 VUL 20 NO. 2 2014) THE CASE JOURNAL PAGE235 Search 'Add Link P. Export PDF Exhibit 5 Table AIV Key executives six months after merger with 57th Street John D. Ireland CFO, Exec VP Finance, Treasurer Michael Smith Sr VP Business Development, Director Harley Smith Chief Development Officer & VP Gary Morrow VP Store Operations Julian Geiger CEO, President, Director Source: Yahoo.com finance Adobe Export PDF Convert PDF Files to Word or Excel Online Select PDF File Cupcakes b...osting.pdf X Convert to Microsoft Word (.docx) V Document Language: English (U.S.) Change Convert Edit PDF Po Create PDF Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial Home Tools Emerald_tcj_tcj49... X Sign In A 11 / 11 o # 80% 9 LATHUILU Table AV CBL Consolidated statements of operations Search 'Add Link P. Export PDF 12/31/2011 $39,882,078 16,945,889 22,936,189 12/31/2010 $31,077,448 12,879,677 18,197,771 End date Net sales Cost of sales Gross profit Operating expenses Selling expenses Staff expenses Occupancy expenses General and administrative New store expenses Depreciation and amortization Total Income (loss) from operations Other income (expense) Interest and other income Loss on sale of property and equipment Loss on impairment of leasehold Improvements 1,424,146 14,557,557 7,369,409 2,706, 115 841,219 1,459,588 28,358,034 (5,421,845) Adobe Export PDF Convert PDF Files to Word or Excel Online 1,146,226 8,266,574 4,711,783 1,374,369 778,558 929,894 17,207,404 990,367 Select PDF File Cupcakes b...osting.pdf X 8,999 (18,126) (770,102) 124 (3,413) Convert to Abandoned lease projects 163,792) (843,021) (190,707) (193,996) Microsoft Word (.docx) V 796,371 Document Language: English (U.S.) Change 796,371 Income loss) before income tax Income tax benefit Net income (loss) attributable to controlling and non-controlling interest Less: net income (loss) attributable to non-controlling interest Net income (loss) attributable to stockholders Net income (loss) per common share, basic and diluted Weighted average number of common shares outstanding, basic and diluted : " Note: "The weighted average number of common shares outstanding is that of CBL Inc Source: 10-K filing investing.businessweek.com (6,264,866) (13,980) (6,250,886) 2,592,111 (3,658,775) (0.66) 5,552,195 796,371 0.20 3,904,466 Convert About the authors Edit PDF Po Create PDF Sambhavi Lakshminarayanan is an Associate Professor in the School of Business at the Medgar Evers College - City University of New York. She received her PhD in Management Science. Dr Lakshminarayanan has published papers and cases in various areas and has co-authored two books. She has also served as reviewer for several journals. Her research interests are wideranging and cross-disciplinary, they include business strategy, small and family business, and organizational functioning. Sambhavi Lakshminarayanan is the corresponding author and can be contacted at: slakshminarayanan@mec.cuny.edu Savita Hanspal is a PhD in Marketing. She is an Assistant Professor at the Huether School of Business, , College of Saint Rose, New York. She has published several research papers in peer reviewed journals and has authored three books and a number of book chapters. Her research interests include consumer behavior, service failures and marketing, advertising, corporate social responsibility, sustainability, and customer satisfaction. Comment Convert, edit and e-sign PDF forms & agreements Free 7-Day Trial

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts