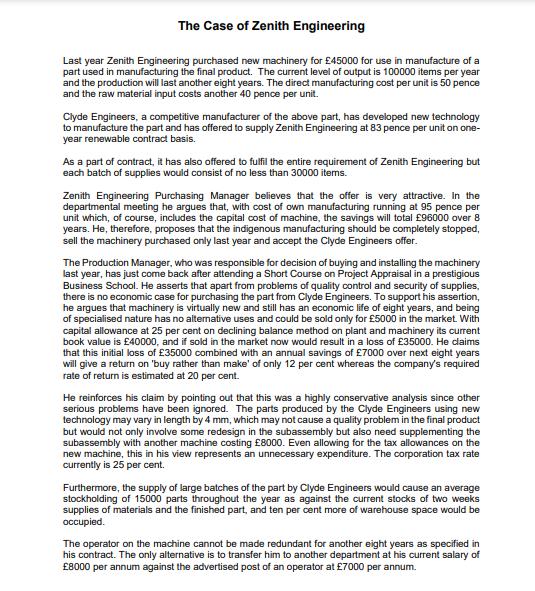

The Case of Zenith Engineering Last year Zenith Engineering purchased new machinery for 45000 for use...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

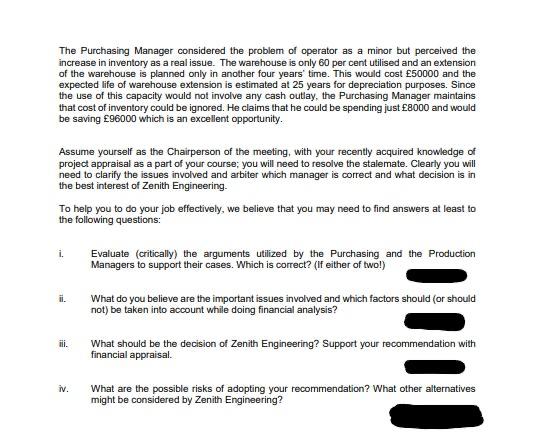

The Case of Zenith Engineering Last year Zenith Engineering purchased new machinery for £45000 for use in manufacture of a part used in manufacturing the final product. The current level of output is 100000 items per year and the production will last another eight years. The direct manufacturing cost per unit is 50 pence and the raw material input costs another 40 pence per unit. Clyde Engineers, a competitive manufacturer of the above part, has developed new technology to manufacture the part and has offered to supply Zenith Engineering at 83 pence per unit on one- year renewable contract basis. As a part of contract, it has also offered to fulfil the entire requirement of Zenith Engineering but each batch of supplies would consist of no less than 30000 items. Zenith Engineering Purchasing Manager believes that the offer is very attractive. In the departmental meeting he argues that, with cost of own manufacturing running at 95 pence per unit which, of course, includes the capital cost of machine, the savings will total £96000 over 8 years. He, therefore, proposes that the indigenous manufacturing should be completely stopped, sell the machinery purchased only last year and accept the Clyde Engineers offer. The Production Manager, who was responsible for decision of buying and installing the machinery last year, has just come back after attending a Short Course on Project Appraisal in a prestigious Business School. He asserts that apart from problems of quality control and security of supplies, there is no economic case for purchasing the part from Clyde Engineers. To support his assertion, he argues that machinery is virtually new and still has an economic life of eight years, and being of specialised nature has no aitermative uses and could be sold only for £5000 in the market. With capital allowance at 25 per cent on declining balance method on plant and machinery its current book value is £40000, and if sold in the market now would result in a loss of £35000. He claims that this initial loss of £35000 combined with an annual savings of £7000 over next eight years will give a return on 'buy rather than make' of only 12 per cent whereas the company's required rate of return is estimated at 20 per cent. He reinforces his claim by pointing out that this was a highly conservative analysis since other serious problems have been ignored. The parts produced by the Clyde Engineers using new technology may vary in length by 4 mm, which may not cause a quality problem in the final product but would not only involve some redesign in the subassembly but also need supplementing the subassembly with another machine costing £8000. Even allowing for the tax allowances on the new machine, this in his view represents an unnecessary expenditure. The corporation tax rate currently is 25 per cent. Furthermore, the supply of large batches of the part by Clyde Engineers would cause an average stockholding of 15000 parts throughout the year as against the current stocks of two weeks supplies of materials and the finished part, and ten per cent more of warehouse space would be occupied. The operator on the machine cannot be made redundant for another eight years as specified in his contract. The only alternative is to transfer him to another department at his current salary of £8000 per annum against the advertised post of an operator at £7000 per annum. The Purchasing Manager considered the problem of operator as a minor but perceived the increase in inventory as a real issue. The warehouse is only 60 per cent utilised and an extension of the warehouse is planned only in another four years' time. This would cost £50000 and the expected life of warehouse extension is estimated at 25 years for depreciation purposes. Since the use of this capacity would not involve any cash outlay, the Purchasing Manager maintains that cost of inventory could be ignored. He claims that he could be spending just £8000 and would be saving £96000 which is an excellent opportunity. Assume yourself as the Chairperson of the meeting, with your recently acquired knowledge of project appraisal as a part of your course; you will need to resolve the stalemate. Clearly you will need to clarify the issues involved and arbiter which manager is correct and what decision is in the best interest of Zenith Engineering. To help you to do your job effectively, we believe that you may need to find answers at least to the following questions: i. Evaluate (critically) the arguments utilized by the Purchasing and the Production Managers to support their cases. Which is correct? (If either of two!) ii. What do you believe are the important issues involved and which factors should (or should not) be taken into account while doing financial analysis? ili. What should be the decision of Zenith Engineering? Support your recommendation with financial appraisal. iv. What are the possible risks of adopting your recommendation? What other alternatives might be considered by Zenith Engineering? The Case of Zenith Engineering Last year Zenith Engineering purchased new machinery for £45000 for use in manufacture of a part used in manufacturing the final product. The current level of output is 100000 items per year and the production will last another eight years. The direct manufacturing cost per unit is 50 pence and the raw material input costs another 40 pence per unit. Clyde Engineers, a competitive manufacturer of the above part, has developed new technology to manufacture the part and has offered to supply Zenith Engineering at 83 pence per unit on one- year renewable contract basis. As a part of contract, it has also offered to fulfil the entire requirement of Zenith Engineering but each batch of supplies would consist of no less than 30000 items. Zenith Engineering Purchasing Manager believes that the offer is very attractive. In the departmental meeting he argues that, with cost of own manufacturing running at 95 pence per unit which, of course, includes the capital cost of machine, the savings will total £96000 over 8 years. He, therefore, proposes that the indigenous manufacturing should be completely stopped, sell the machinery purchased only last year and accept the Clyde Engineers offer. The Production Manager, who was responsible for decision of buying and installing the machinery last year, has just come back after attending a Short Course on Project Appraisal in a prestigious Business School. He asserts that apart from problems of quality control and security of supplies, there is no economic case for purchasing the part from Clyde Engineers. To support his assertion, he argues that machinery is virtually new and still has an economic life of eight years, and being of specialised nature has no aitermative uses and could be sold only for £5000 in the market. With capital allowance at 25 per cent on declining balance method on plant and machinery its current book value is £40000, and if sold in the market now would result in a loss of £35000. He claims that this initial loss of £35000 combined with an annual savings of £7000 over next eight years will give a return on 'buy rather than make' of only 12 per cent whereas the company's required rate of return is estimated at 20 per cent. He reinforces his claim by pointing out that this was a highly conservative analysis since other serious problems have been ignored. The parts produced by the Clyde Engineers using new technology may vary in length by 4 mm, which may not cause a quality problem in the final product but would not only involve some redesign in the subassembly but also need supplementing the subassembly with another machine costing £8000. Even allowing for the tax allowances on the new machine, this in his view represents an unnecessary expenditure. The corporation tax rate currently is 25 per cent. Furthermore, the supply of large batches of the part by Clyde Engineers would cause an average stockholding of 15000 parts throughout the year as against the current stocks of two weeks supplies of materials and the finished part, and ten per cent more of warehouse space would be occupied. The operator on the machine cannot be made redundant for another eight years as specified in his contract. The only alternative is to transfer him to another department at his current salary of £8000 per annum against the advertised post of an operator at £7000 per annum. The Purchasing Manager considered the problem of operator as a minor but perceived the increase in inventory as a real issue. The warehouse is only 60 per cent utilised and an extension of the warehouse is planned only in another four years' time. This would cost £50000 and the expected life of warehouse extension is estimated at 25 years for depreciation purposes. Since the use of this capacity would not involve any cash outlay, the Purchasing Manager maintains that cost of inventory could be ignored. He claims that he could be spending just £8000 and would be saving £96000 which is an excellent opportunity. Assume yourself as the Chairperson of the meeting, with your recently acquired knowledge of project appraisal as a part of your course; you will need to resolve the stalemate. Clearly you will need to clarify the issues involved and arbiter which manager is correct and what decision is in the best interest of Zenith Engineering. To help you to do your job effectively, we believe that you may need to find answers at least to the following questions: i. Evaluate (critically) the arguments utilized by the Purchasing and the Production Managers to support their cases. Which is correct? (If either of two!) ii. What do you believe are the important issues involved and which factors should (or should not) be taken into account while doing financial analysis? ili. What should be the decision of Zenith Engineering? Support your recommendation with financial appraisal. iv. What are the possible risks of adopting your recommendation? What other alternatives might be considered by Zenith Engineering?

Expert Answer:

Answer rating: 100% (QA)

The main issue here is whether or not to outsource the production of the part in question to Clyde Engineers The Purchasing Manager believes that this ... View the full answer

Related Book For

Accounting For Cambridge International AS And A Level

ISBN: 9780198399711

1st Edition

Authors: Jacqueline Halls Bryan, Peter Hailstone

Posted Date:

Students also viewed these finance questions

-

Last year Precision Engineering purchased new machinery for 45000 for use in the manufacture of a part used in manufacturing the final product. The current level of output is 100000 items per year...

-

On April 1, 2013, Verlin Co. purchased new machinery for $300,000. The machinery has an estimated useful life of five years, and depreciation is computed by the sum-of-the-years'-digits method. The...

-

John purchased new machinery for his small business factory on 1st June 2018 for $8,000. The effective life of the machinery is determined to be five years. John sold his old business machinery for...

-

Mary Wells Lawrence once said, In this business, you can never wash the dinner dishes and say they are done. You have to keep doing them constantly. If you were a business executive or information...

-

Nikita Companys financial statements show the following. The company recently discovered that in making physical counts of inventory, it had made the following errors: Inventory on December 31, 2008,...

-

Solve. x 4 - 8x 2 = 9

-

A & L Mechanics is operated by Adrian and Len in partnership. Financial data for the partnership follow. Additional information 1. All profits/losses are shared equally by Adrian and Len who also...

-

Minturn Enterprises, Inc., operates as three autonomous companies, each with a chief executive officer who oversees its operations. At a recent corporate meeting, the company CEOs agreed to adopt...

-

Calculate and interpret the present value of growth opportunities (PVGO): Here is a company's information: Share price $80 Expected earnings $5 Required return on shares 10%. Choose the best answer:...

-

Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek as of May 1, 2018 (unless otherwise indicated), are as follows: During...

-

MA 2 B 2 is a molecule where M is the central atom bonded to 2 atoms of A and 2 atoms of B. The fact that it exists in only one form (no isomers) suggests its geometry is Select one: a. octahedral b....

-

Provide a brief introduction to the connection pooling API.

-

The placeholder used in the setXXX() and the registerOUTParameter() methods is used to ___________________. a. Indicate the location of the input or output parameters b. Reserve spaces for input or...

-

Both interfaces, PreparedStatement and CallableStatement, are used to perform dynamic Oracle statements; however, performs queries with only parameters, but calls stored procedures with both and...

-

The ResultSet object can be created by either executing the or method, which means that the ResultSet instance cannot be created or used without executing a query operation first. a. executeQuery(),...

-

The ____________ interface allows you to discover the structure of Tables and properties of columns, but the _______________ interface enables you to dynamically determine properties of the RDBMS. a....

-

In a newspaper poll, 52% of respondents say they will vote for a certain presidential candidate. The range of the actual percentage can be expressed by the expression |x - 4|, where x is the actual...

-

QUESTION 2 The CEO of Farisha Hijab Sdn Bhd insisted on further investigation to be carried out that he also required Mr Muaz to conduct the analysis of variance for the material and labour of the...

-

Bobby is in business as a market stallholder. He has not kept full accounting records. His statement of affairs at 1 April 2014 showed his capital was $86 000; his statement of affairs at 31 March...

-

If capital expenditure was incorrectly treated as revenue expenditure, what would be the effect on the business's profit for the year?

-

The following information is available for S. Ramjeet Lid, a manufacturer of toys, for the year ended 31 March 2015. Prepare an extract from the manufacturing account to show the prime cost for the...

-

(a) Express the magnitude of the electric field inside the strip in Figure 27.43 in terms of the width \(w\) of the strip and the potential difference \(V_{\mathrm{RL}}\). (b) Given the magnitude...

-

A compass sits on a table with its needle pointing to Earth's North Pole. A bar magnet with its long axis oriented along an east-west line is brought toward the compass from the east. If the needle...

-

Explain why the \(1 / r\) dependence expressed in Eq. 27.38 is consistent with the symmetry of the wire causing the magnetic field. B = = 2kI rco 2k I (27.38) &

Study smarter with the SolutionInn App