Question: The correct answer is 7.063. Could you please show some details about soluyion. 4. A share price is currently 196.25, and over each of the

The correct answer is 7.063.

Could you please show some details about soluyion.

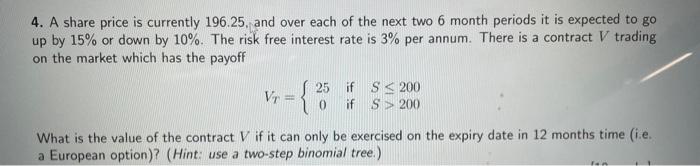

4. A share price is currently 196.25, and over each of the next two 6 month periods it is expected to go up by 15% or down by 10%. The risk free interest rate is 3% per annum. There is a contract V trading on the market which has the payoff 25 if S 200 VT = 0 if S> 200 What is the value of the contract V if it can only be exercised on the expiry date in 12 months time (i.e. a European option)? (Hint: use a two-step binomial tree.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock