Question: The correct answer is highlighted, just wondering how to work it out Question 8 1/1 pts Suppose that the two-year interest rates in Australia and

The correct answer is highlighted, just wondering how to work it out

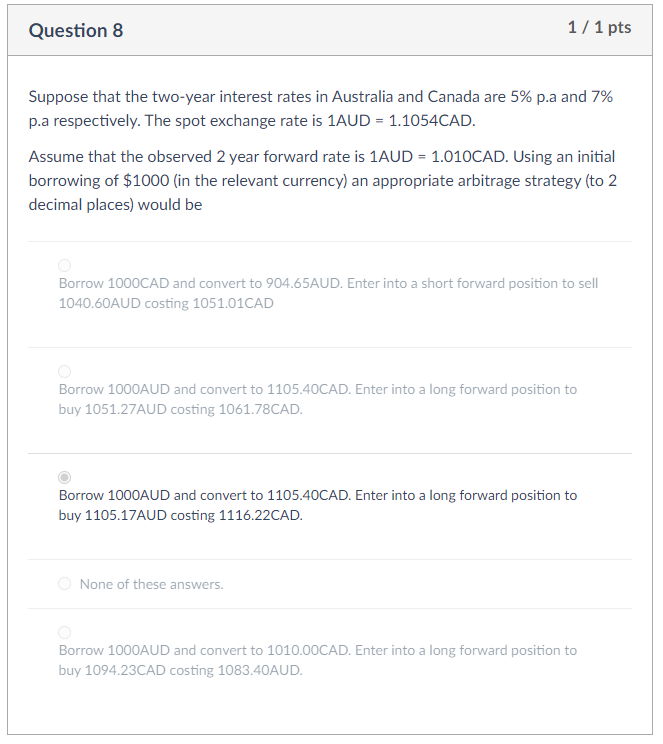

Question 8 1/1 pts Suppose that the two-year interest rates in Australia and Canada are 5% p.a and 7% p.a respectively. The spot exchange rate is 1AUD=1.1054CAD. Assume that the observed 2 year forward rate is 1AUD=1.010CAD. Using an initial borrowing of $1000 (in the relevant currency) an appropriate arbitrage strategy (to 2 decimal places) would be Borrow 1000CAD and convert to 904.65AUD. Enter into a short forward position to sell 1040.60AUD costing 1051.01CAD Borrow 1000AUD and convert to 1105.40CAD. Enter into a long forward position to buy 1051.27AUD costing 1061.78CAD. Borrow 1000AUD and convert to 1105.40CAD. Enter into a long forward position to buy 1105.17AUD costing 1116.22CAD. None of these answers. Borrow 1000AUD and convert to 1010.00CAD. Enter into a long forward position to buy 1094.23CAD costing 1083.40AUD

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts