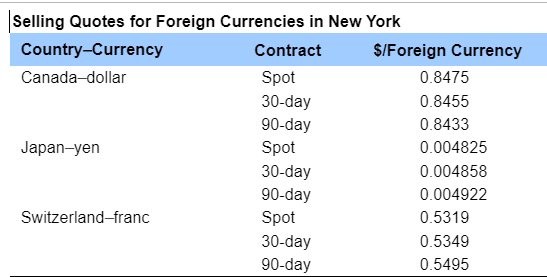

Question: The data for the following problem is given in the popup window: Compute the indirect quote for the spot and forward Canadian dollar, yen, and

The data for the following problem is given in the popup window:

Compute the indirect quote for the spot and forward Canadian dollar, yen, and Swiss franc contracts.

Question content area bottom

Part 1

a.The indirect quote for the spot Canadian dollar contract is __ C$/$.(Round to four decimal places.)

b. yen

c. francs

\begin{tabular}{|lll} \hline Selling Quotes for Foreign Currencies in New York \\ Country-Currency & Contract & S/Foreign Currency \\ Canada-dollar & Spot & 0.8475 \\ & 30-day & 0.8455 \\ & 90-day & 0.8433 \\ Japan-yen & Spot & 0.004825 \\ & 30-day & 0.004858 \\ & 90-day & 0.004922 \\ Switzerland-franc & Spot & 0.5319 \\ & 30-day & 0.5349 \\ & 90-day & 0.5495 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts