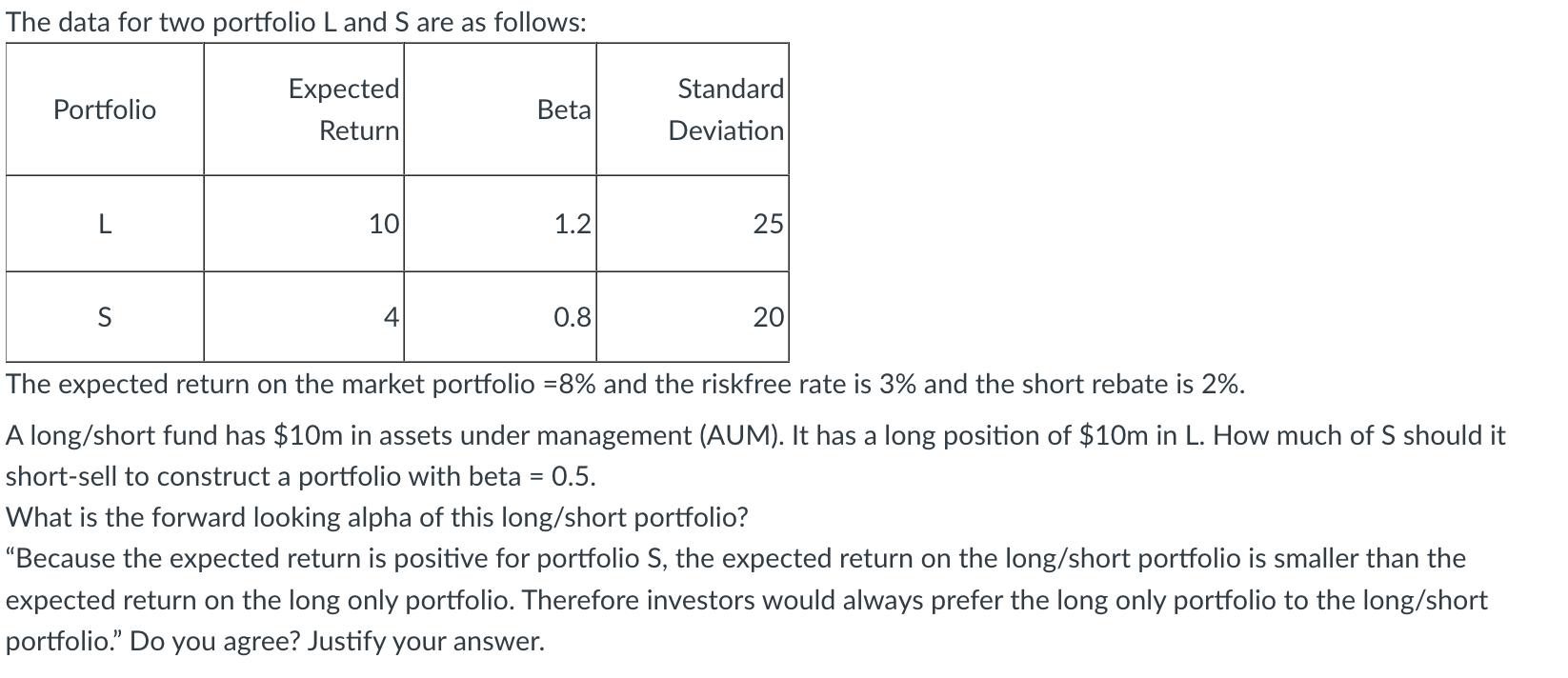

The data for two portfolio L and S are as follows: Expected Return Portfolio L S...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Lets start by calculating how much of portfolio S the longshort fund should shortsell to construct a portfolio with a beta of 05 The formula to calcul... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: