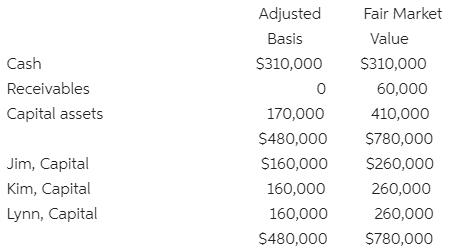

The December 31, 2019 balance sheet of the JKL Partnership appears below: Each partner shares in 1/3

Question:

The December 31, 2019 balance sheet of the JKL Partnership appears below: Each partner shares in 1/3 of the partnership capital, income, gains, losses, deductions and credits. The partnership provides consulting services to its clients (capital is not a material income-producing factor). On December 31, 2019, General Partner Lynn receives a distribution of $270,000 cash in retirement of her partnership interest. Nothing is stated in the partnership agreement about goodwill.

Each partner shares in 1/3 of the partnership capital, income, gains, losses, deductions and credits. The partnership provides consulting services to its clients (capital is not a material income-producing factor). On December 31, 2019, General Partner Lynn receives a distribution of $270,000 cash in retirement of her partnership interest. Nothing is stated in the partnership agreement about goodwill.

Required:

Assuming that Lynn’s outside basis for the partnership interest immediately before the distribution was $160,000, determine the amount and nature of her gain from the distribution.

What tax consequence does the $270,000 payment to Lynn have for the partnership?

What action or planning opportunity should the partnership consider and what effect would that action have?

Expert Answer:

Fundamental Accounting Principles Volume II

ISBN: 978-1260305838

16th Canadian edition

Authors: Kermit Larson, Tilly Jensen, Heidi Dieckmann