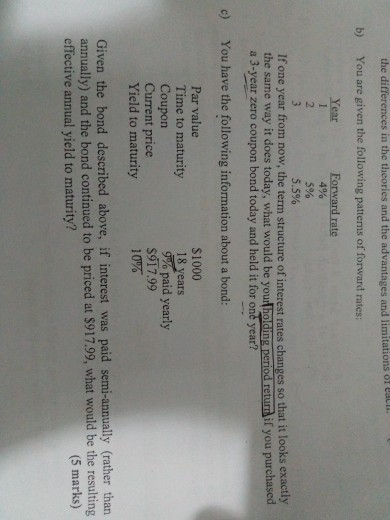

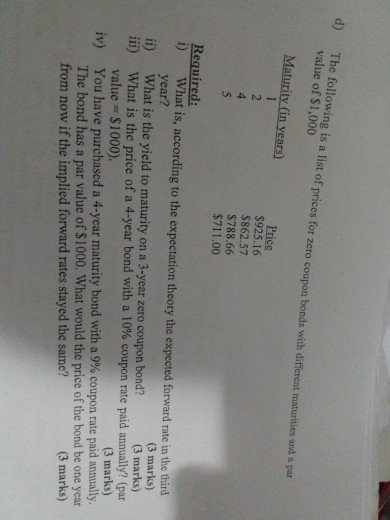

Question: the differences in the td b) You are given the following pattens of forward rates: Year Forward rate 4% 5% 5.5% If one year from

the differences in the td b) You are given the following pattens of forward rates: Year Forward rate 4% 5% 5.5% If one year from now, the term structure of interest rates changes so that it looks exactly the same way it does today, what would be your holding period return if you purchased a 3-year zero coupon bond today and held it for one year? c) You have the following information about a bond: $1000 18 years Par value Time to maturity Coupon Current price Yield to maturity paid yearly $917.99 10% Given the bond described above, if interest was paid semi-annually (rather than annually) and the bond continued to be priced at $917.99, what would be the resulting effective annual yield to maturity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts