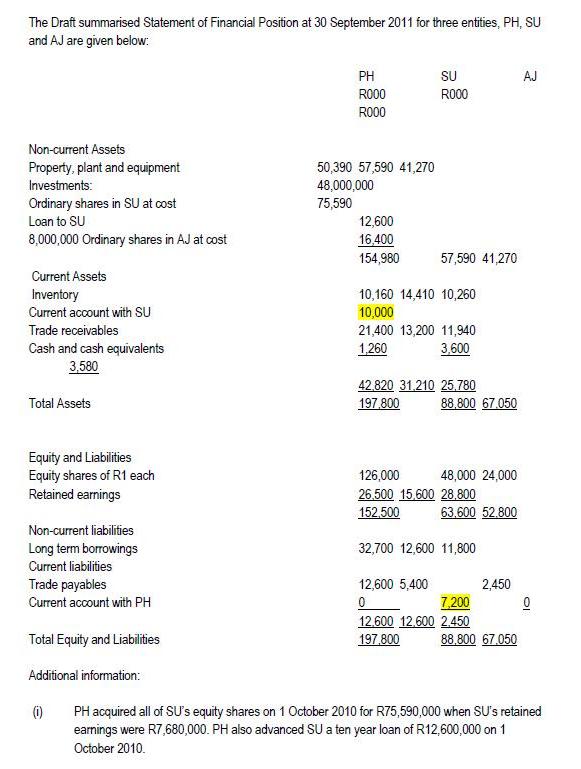

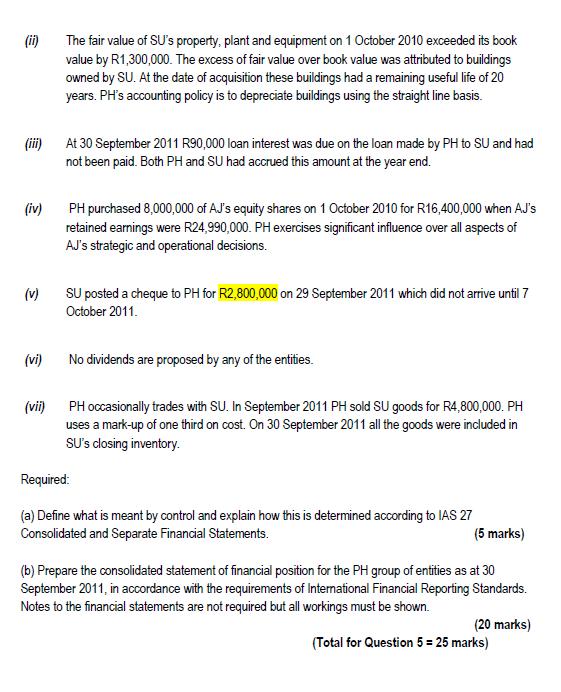

The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks) The Draft summarised Statement of Financial Position at 30 September 2011 for three entities, PH, SU and AJ are given below: PH SU AJ RO00 R000 RO00 Non-current Assets Property, plant and equipment 50,390 57,590 41,270 Investments: 48,000,000 75,590 Ordinary shares in SU at cost Loan to SU 12,600 8,000,000 Ordinary shares in AJ at cost 16,400 154,980 57,590 41,270 Current Assets Inventory Current account with SU 10,160 14,410 10,260 10,000 Trade receivables 21,400 13,200 11,940 Cash and cash equivalents 3,580 1,260 3,600 42.820 31.210 25.780 197.800 Total Assets 88,800 67.050 Equity and Liabilities Equity shares of R1 each Retained earnings 126,000 48,000 24,000 26.500 15.600 28.800 152,500 63.600 52.800 Non-current liabilities Long term borrowings Current liabilities 32,700 12,600 11,800 Trade payables 12,600 5,400 2,450 Current account with PH 7.200 12.600 12.600 2.450 Total Equity and Liabilities 197,800 88.800 67.050 Additional information: (i) PH acquired all of SU's equity shares on 1 October 2010 for R75,590,000 when SU's retained earnings were R7,680,000. PH also advanced SU a ten year loan of R12,600,000 on 1 October 2010. (ii) The fair value of SU's property, plant and equipment on 1 October 2010 exceeded its book value by R1,300,000. The excess of fair value over book value was attributed to buildings owned by SU. At the date of acquisition these buildings had a remaining useful life of 20 years. PH's accounting policy is to depreciate buildings using the straight line basis. (ii) At 30 September 2011 R90,000 loan interest was due on the loan made by PH to SU and had not been paid. Both PH and SU had accrued this amount at the year end. (iv) PH purchased 8,000,000 of AJ's equity shares on 1 October 2010 for R16,400,000 when AJ's retained earnings were R24,990,000. PH exercises significant influence over all aspects of AJ's strategic and operational decisions. SU posted a cheque to PH for R2,800,000 on 29 September 2011 which did not arrive until 7 October 2011. (v) (vi) No dividends are proposed by any of the entities. (vii) PH occasionally trades with SU. In September 2011 PH sold SU goods for R4,800,000. PH uses a mark-up of one third on cost. On 30 September 2011 all the goods were included in SƯs dosing inventory. Required: (a) Define what is meant by control and explain how this is determined according to IAS 27 Consolidated and Separate Financial Statements. (5 marks) (b) Prepare the consolidated statement of financial position for the PH group of entities as at 30 September 2011, in accordance with the requirements of International Financial Reporting Standards. Notes to the financial statements are not required but all workings must be shown. (20 marks) (Total for Question 5 = 25 marks)

Expert Answer:

Answer rating: 100% (QA)

AnsaControl is defined by IFRS 10 as follows An investor controls an investee when the investor is e... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The comparative consolidated statement of financial position at December 31, Year 2, and the consolidated income statement for Year 2, of Parent Ltd. and its 70%-owned subsidiary are shown below....

-

Ayayai tnc. reported the following partial income statement data for the years ended December 31, 2018, and 2017: 2010 2017 Sales $267,000 $242,000 Cost of gonds sold 208,000 189,244 Gruss profit...

-

The comparative unclassified statement of financial position for Puffy Ltd. follows: Additional information: 1. Net income was $115,000. 2. Sales were $978,000. 3. Cost of goods sold was $751,000. 4....

-

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the inception Of the lease. Title does not transfer to the lessee and there is no bargain purchase...

-

What is organizational culture, what role does it play in organizations, and how is it created?

-

Joanne is a seventy-five-year-old widow who survives on her husbands small pension. Joanne has become increasingly forgetful, and her family worries that she may have Alzheimers disease (a brain...

-

Unless otherwise specified, which rule will always be processed?

-

For the year ended December 31, 2010, Blasing Electrical Repair Company reports the following summary payroll data. Blasing Companys payroll taxes are: FICA 8%, state unemployment 2.5% (due to a...

-

4. Consider that you are a manager at a local Chick-fil-a. You have been approved for a loan to make improvements to your store. Provide examples of costs/receipts for the variables we covered in...

-

1. How is performance management at DMG world media different from traditional performance management systems at other companies? 2. What was the impetus for developing a different performance...

-

Clayton McNulty, owner of McNultys Muscular Materials (MMM), is sitting in his dim office located at the top of an old brown brick building, in an industrial area of South Boston. Clayton had just...

-

1. Why is insurance important? Choose two types of insurance and discuss their characteristics. 2. What questions should you ask yourself before you choose a life insurance policy? 3. What factors...

-

On June 1, Waterway Company borrows $111,000 from First Bank on a 6-month, $111,000, 8% note. Prepare the entry on June 1. (Credit account titles are automatically indented when amount is entered. Do...

-

If Western Civilization was to begin recognizing and honoring the Divine Feminine, what woman (or women) would you suggest as a model for figurines, paintings, statues, and/or pictures on a coin?...

-

a CFO of a hospital need to reduce its budget and The CFO's first step for budget reduction is identifying the areas where the hospital needs budget reduction and developing a plan that outlines the...

-

A refrigerator uses 40.0 of work to exhaust 90.0 J from a heat reservoir at 0.00C. What is the coefficient of performance for the refrigerator?

-

Currently, the primary source of sulfur dioxide emissions into the atmosphere is a . diesel trucks. b . plastic manufacturing. c . coal burning power plants. d . gasoline - powered lawnmowers.

-

A business had revenues of $280,000 and operating expenses of $315,000. Did the business (a) Incur a net loss (b) Realize net income?

-

Identify the phases in the joint conceptual framework project. What two phases are expect to be completed earliest?

-

What are the basic elements of the framework? Briefly describe the relationship between the moment in time and period of time elements?

-

Explain the role of the international financial Reporting Interpretations Committee.

-

What ethical issues might arise during the fact-finding process, and how should they be handled?

-

Why are conventional files easy to design and implement?

-

Determine the business's or organization's requirements through interviews, forms, surveys, JAD, and the like, and create the appropriate models and studies for the Web site. Don't forget to consider...

Study smarter with the SolutionInn App