Question: The final part is to convert the risk class derived from the financial ratio analysis into a number by which the net worth can

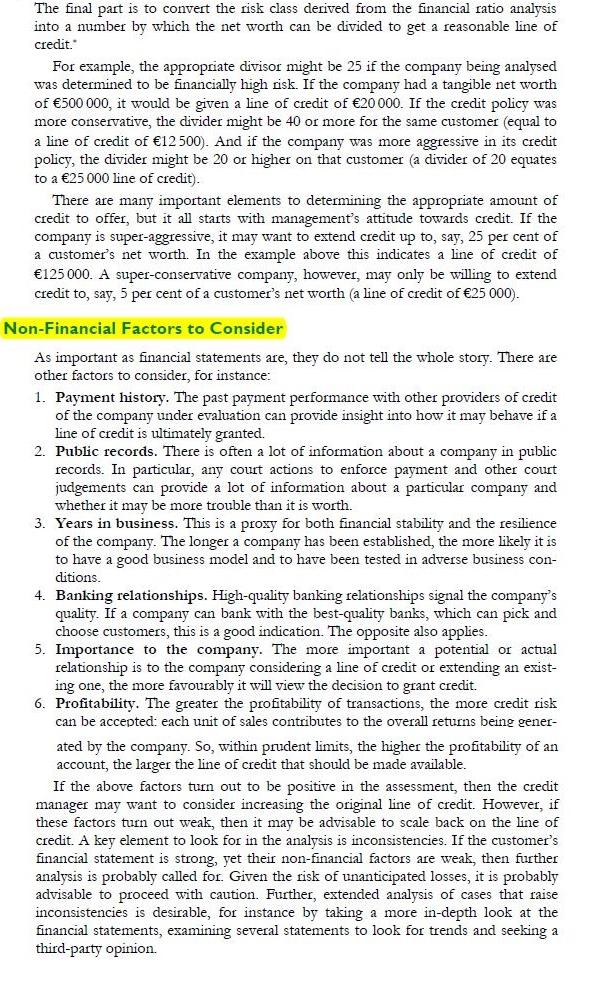

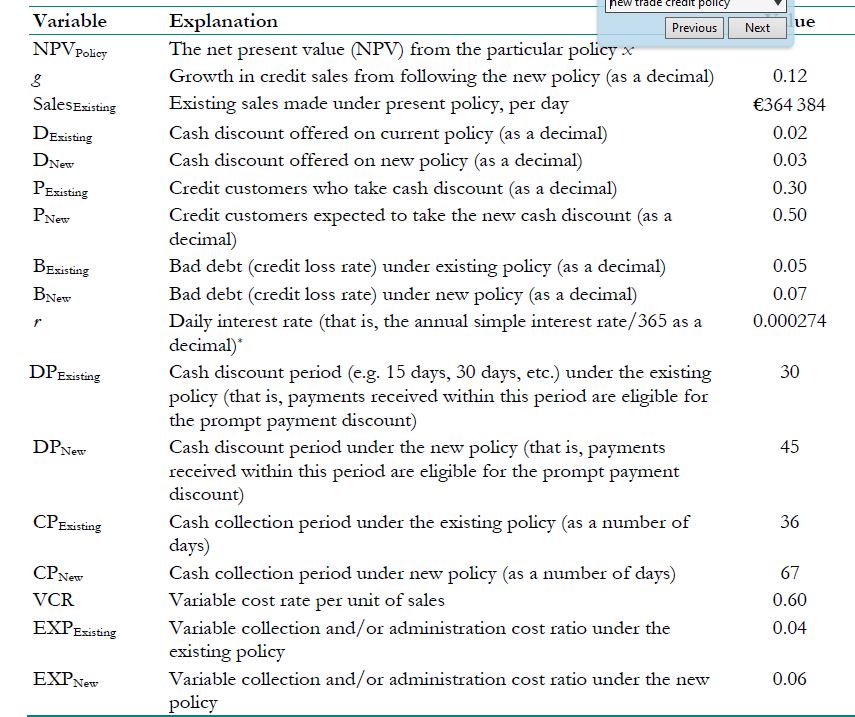

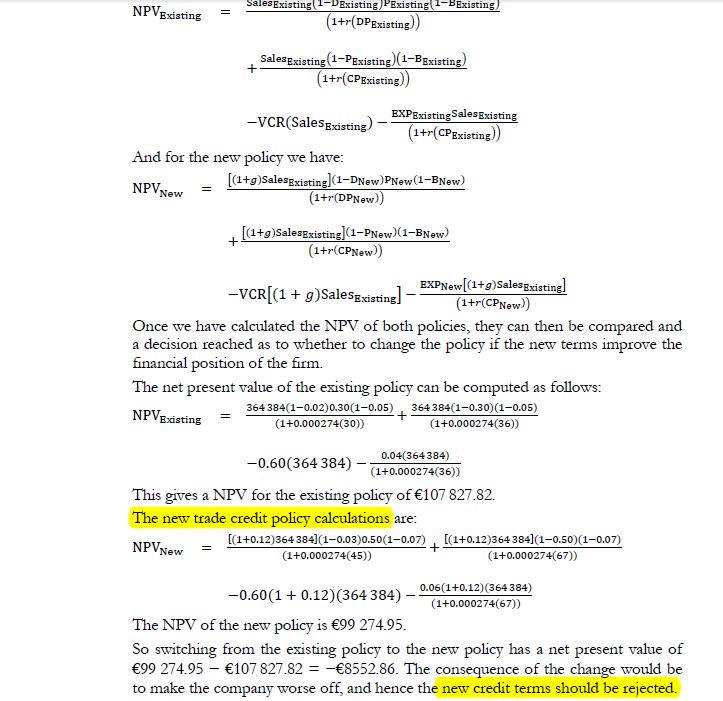

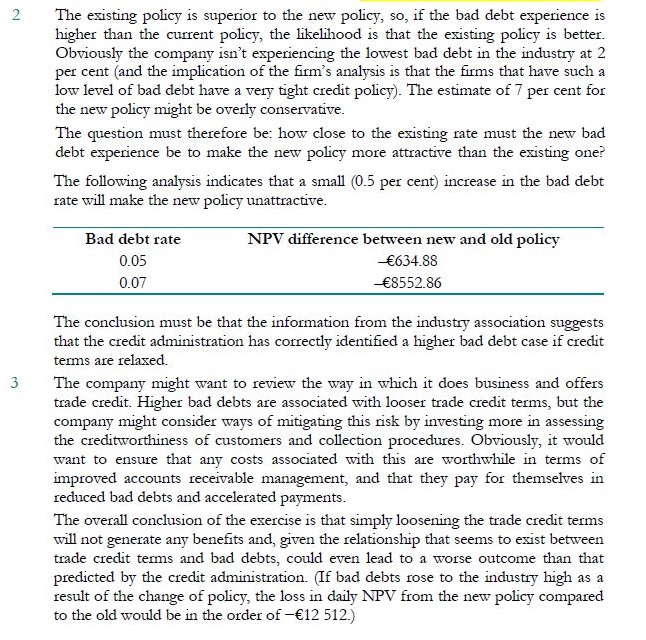

The final part is to convert the risk class derived from the financial ratio analysis into a number by which the net worth can be divided to get a reasonable line of credit.* For example, the appropriate divisor might be 25 if the company being analysed was determined to be financially high risk. If the company had a tangible net worth of 500 000, it would be given a line of credit of 20 000. If the credit policy was more conservative, the divider might be 40 or more for the same customer (equal to a line of credit of 12500). And if the company was more aggressive in its credit policy, the divider might be 20 or higher on that customer (a divider of 20 equates to a 25 000 line of credit). There are many important elements to determining the appropriate amount of credit to offer, but it all starts with management's attitude towards credit. If the company is super-aggressive, it may want to extend credit up to, say, 25 per cent of a customer's net worth. In the example above this indicates a line of credit of 125 000. A super-conservative company, however, may only be willing to extend credit to, say, 5 per cent of a customer's net worth (a line of credit of 25 000). Non-Financial Factors to Consider As important as financial statements are, they do not tell the whole story. There are other factors to consider, for instance: 1. Payment history. The past payment performance with other providers of credit of the company under evaluation can provide insight into how it may behave if a line of credit is ultimately granted. 2. Public records. There is often a lot of information about a company in public records. In particular, any court actions to enforce payment and other court judgements can provide a lot of information about a particular company and whether it may be more trouble than it is worth. 3. Years in business. This is a proxy for both financial stability and the resilience of the company. The longer a company has been established, the more likely it is to have a good business model and to have been tested in adverse business con- ditions. 4. Banking relationships. High-quality banking relationships signal the company's quality. If a company can bank with the best-quality banks, which can pick and choose customers, this is a good indication. The opposite also applies. 5. Importance to the company. The more important a potential or actual relationship is to the company considering a line of credit or extending an exist- ing one, the more favourably it will view the decision to grant credit. 6. Profitability. The greater the profitability of transactions, the more credit risk can be accepted: each unit of sales contributes to the overall returns being gener- ated by the company. So, within prudent limits, the higher the profitability of an account, the larger the line of credit that should be made available. If the above factors turn out to be positive in the assessment, then the credit manager may want to consider increasing the original line of credit. However, if these factors turn out weak, then it may be advisable to scale back on the line of credit. A key element to look for in the analysis is inconsistencies. If the customer's financial statement is strong, yet their non-financial factors are weak, then further analysis is probably called for. Given the risk of unanticipated losses, it is probably advisable to proceed with caution. Further, extended analysis of cases that raise inconsistencies is desirable, for instance by taking a more in-depth look at the financial statements, examining several statements to look for trends and seeking a third-party opinion. Variable NPV Policy 8 Sales Existing DExisting DNew PExisting PNew BExisting BNew r DPExisting DP New CP Existing CP New VCR EXPExisting EXPNew new trade Explanation The net present value (NPV) from the particular policy x Growth in credit sales from following the new policy (as a decimal) Existing sales made under present policy, per day Cash discount offered on current policy (as a decimal) Cash discount offered on new policy (as a decimal) Credit customers who take cash discount (as a decimal) Credit customers expected to take the new cash discount (as a decimal) Previous policy Bad debt (credit loss rate) under existing policy (as a decimal) Bad debt (credit loss rate) under new policy (as a decimal) Daily interest rate (that is, the annual simple interest rate/365 as a decimal)* Cash discount period (e.g. 15 days, 30 days, etc.) under the existing policy (that is, payments received within this period are eligible for the prompt payment discount) Cash discount period under the new policy (that is, payments received within this period are eligible for the prompt payment discount) Cash collection period under the existing policy (as a number of days) Cash collection period under new policy (as a number of days) Variable cost rate per unit of sales Variable collection and/or administration cost ratio under the existing policy Variable collection and/or administration cost ratio under the new policy Next ue 0.12 364 384 0.02 0.03 0.30 0.50 0.05 0.07 0.000274 30 45 36 67 0.60 0.04 0.06 NPV Existing = = Sales Existing (1-DExisting PExisting (1-BExisting) (1+r(DPExisting)) And for the new policy we have: NPV New + Sales Existing (1-PExisting)(1-BExisting) (1+r(CPExisting)) + = -VCR(Sales Existing) [(1+g) Sales Existing] (1-DNew)PNew (1-BNew) (1+r(DPNew)) EXPExisting Sales Existing (1+r(CPExisting)) [(1+g)SalesExisting] (1-PNew)(1-BNew) (1+r(CPNew)) EXPNew [(1+g)Sales Existing] (1+r(CPNew)) -VCR[(1 + g)Sales Existing] Once we have calculated the NPV of both policies, they can then be compared and a decision reached as to whether to change the policy if the new terms improve the financial position of the firm. The net present value of the existing policy can be computed as follows: 364 384(1-0.02)0.30(1-0.05) 364 384(1-0.30)(1-0.05) NPV Existing = + (1+0.000274(30)) (1+0.000274(36)) 0.04(364384) (1+0.000274(36)) -0.60(364 384) This gives a NPV for the existing policy of 107 827.82. The new trade credit policy calculations are: NPV New [(1+0.12)364 384] (1-0.03)0.50(1-0.07) (1+0.000274(45)) + [(1+0.12)364 384] (1-0.50)(1-0.07) (1+0.000274(67)) 0.06(1+0.12) (364 384) (1+0.000274(67)) -0.60(1+0.12) (364 384) - The NPV of the new policy is 99 274.95. So switching from the existing policy to the new policy has a net present value of 99 274.95 8552.86. The consequence of the change would be 107 827.82 to make the company worse off, and hence the new credit terms should be rejected. 2 3 The existing policy is superior to the new policy, so, if the bad debt experience is higher than the current policy, the likelihood is that the existing policy is better. Obviously the company isn't experiencing the lowest bad debt in the industry at 2 per cent (and the implication of the firm's analysis is that the firms that have such a low level of bad debt have a very tight credit policy). The estimate of 7 per cent for the new policy might be overly conservative. The question must therefore be: how close to the existing rate must the new bad debt experience be to make the new policy more attractive than the existing one? The following analysis indicates that a small (0.5 per cent) increase in the bad debt rate will make the new policy unattractive. Bad debt rate 0.05 0.07 NPV difference between new and old policy -634.88 -8552.86 The conclusion must be that the information from the industry association suggests that the credit administration has correctly identified a higher bad debt case if credit terms are relaxed. The company might want to review the way in which it does business and offers trade credit. Higher bad debts are associated with looser trade credit terms, but the company might consider ways of mitigating this risk by investing more in assessing the creditworthiness of customers and collection procedures. Obviously, it would want to ensure that any costs associated with this are worthwhile in terms of improved accounts receivable management, and that they pay for themselves in reduced bad debts and accelerated payments. The overall conclusion of the exercise is that simply loosening the trade credit terms will not generate any benefits and, given the relationship that seems to exist between trade credit terms and bad debts, could even lead to a worse outcome than that predicted by the credit administration. (If bad debts rose to the industry high as a result of the change of policy, the loss in daily NPV from the new policy compared to the old would be in the order of -12 512.) Question 1 In order to gain full marks, please show full workings step by step. Oban is a small building products firm in the construction industry. Conditions have been very poor in the sector, but in the past year there has been an improvement and sales in the industry have been moving forward again. Up to this point Oban has had a credit policy of 'Net 25 with 1.5% discount' and only 30% of their customers were taking the discount. The average payment for those who were not taking the discount was 50 days. However, sales at rival companies have been improving at a quicker pace than at Oban's. The directors have put this down to the fact that the other firms have started to lengthen their credit terms and offer discounts. The directors have decided to change their credit policy. They will instigate a policy of *Net 45 with a 2.5% discount'. Analysts at the firm estimate that 50% of their customers will take up the discount. For those who do not take the discount, payment is expected after 90 days. Oban's existing policy is expected to raise bad debts from 5% to 7%. Industry figures show that the level of bad debts experienced with lengthened credit policies is running at 8%. Oban is confident that their sales will rise by 10% with the new credit policy, which is slightly more generous than rival firms. Current sales are 10m (annually). The variable cost ratio is 0.50 and the administrative expenses incurred from the new credit policy are expected to be 3.0% of the value of unit sales, as opposed to 1.5% with the existing policy. The opportunity cost of capital is 8%. Required: (a) (b) (c) Should Oban's adopt the new trade credit policy? Is it profitable? Show all your workings. (15 marks) Explain in detail how a company would determine what line of credit to offer to a customer if there were financial statements available on the customer. (10 marks) What other non-financial factors should be considered when determining the line of credit offered to a customer? (5 marks)

Step by Step Solution

There are 3 Steps involved in it

SOLUTION a Profitability of the new credit policy To determine the profitability of the new credit policy we need to calculate the expected increase in sales the cost of the new policy and the expecte... View full answer

Get step-by-step solutions from verified subject matter experts