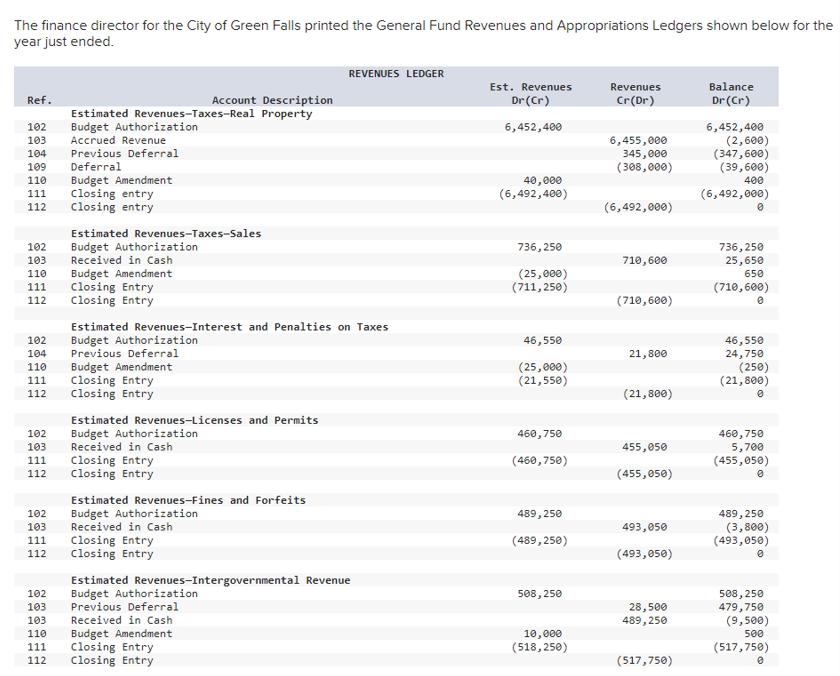

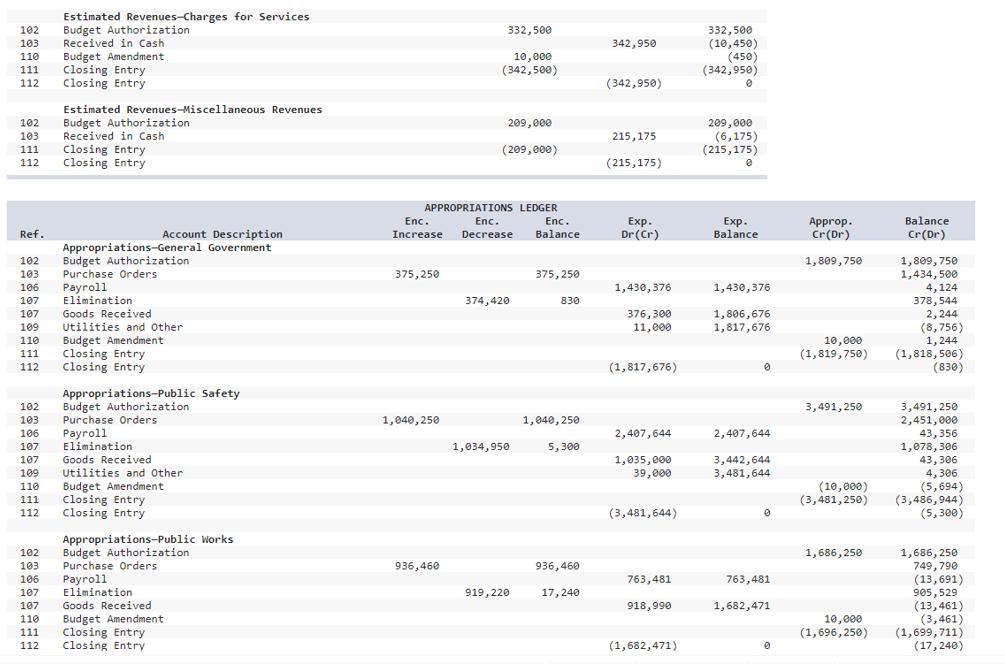

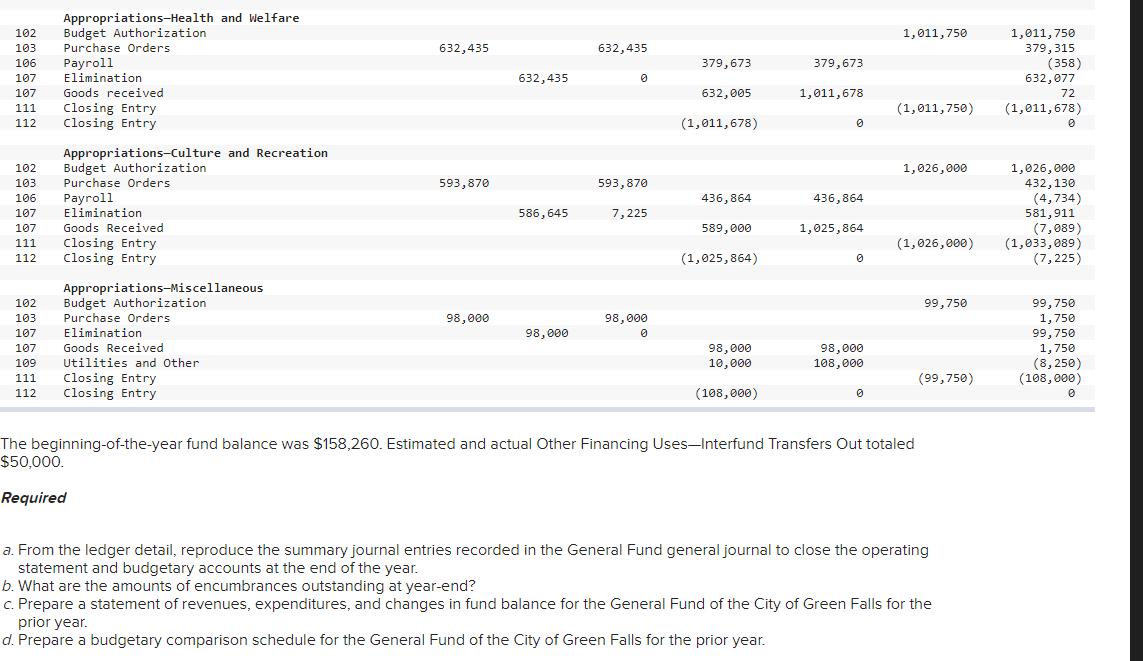

The finance director for the City of Green Falls printed the General Fund Revenues and Appropriations...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The finance director for the City of Green Falls printed the General Fund Revenues and Appropriations Ledgers shown below for the year just ended. Ref. 102 103 Accrued Revenue Previous Deferral 104 109 Deferral 110 Budget Amendment 111 Closing entry 112 Closing entry 102 104 110 102 103 Received in Cash 110 Budget Amendment 111 Closing Entry 112 Closing Entry 111 112 102 103 111 112 102 103 111 112 Account Description Estimated Revenues-Taxes-Real Property Budget Authorization 102 103 103 Estimated Revenues-Taxes-Sales Budget Authorization 110 111 Estimated Revenues-Interest and Penalties on Taxes Budget Authorization. Previous Deferral Budget Amendment Closing Entry Closing Entry Estimated Revenues-Licenses and Permits Budget Authorization Received in Cash Closing Entry Closing Entry REVENUES LEDGER Estimated Revenues-Fines and Forfeits Budget Authorization Received in Cash Closing Entry Closing Entry Estimated Revenues-Intergovernmental Revenue Budget Authorization Previous Deferral Received in Cash Budget Amendment Closing Entry 112 O Closing Entry Est. Revenues Dr (Cr) 6,452,400 40,000 (6,492,400) 736,250 (25,000) (711,250) 46,550 (25,000) (21,550) 460,750 (460,750) 489, 250 (489,250) 508,250 10,000 (518,250) Revenues Cr(Dr) 6,455,000 345,000 (308,000) (6,492,000) 710,600 (710,600) 21,800 (21,800) 455,050 (455,050) 493,050 (493,050) 28,500 489,250 (517,750) Balance Dr (Cr) 6,452,400 (2,600) (347,600) (39,600) 400 (6,492,000) 736,250 25,650 650 (710,600) 0 46,550 24,750 (250) (21,800) 0 460,750 5,700 (455,050) 489,250 (3,800) (493,050) 0 508,250 479,750 (9,500) 500 (517,750) Estimated Revenues-Charges for Services 102 Budget Authorization 103 Received in Cash 110 Budget Amendment 111 Closing Entry Closing Entry 112 102 103. Received in Cash Closing Entry 112 Closing Entry 111 Ref. Account Description Appropriations-General Government 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 Elimination 107 109 110 111 112 102 103 106 107 Estimated Revenues-Miscellaneous Revenues Budget Authorization 107 109 110 111 112 102 103 106 107 107 110 Goods Received Utilities and Other Budget Amendment Closing Entry Closing Entry Appropriations-Public Safety Budget Authorization Purchase Orders Payroll Elimination Goods Received Utilities and Other Budget Amendment Closing Entry Closing Entry Appropriations-Public Works Budget Authorization Purchase Orders Payroll Elimination Goods Received Budget Amendment 111 Closing Entry 112 Closing Entry 375,250 APPROPRIATIONS LEDGER Enc. Enc. Enc. Increase Decrease Balance 1,040,250 332,500 10,000 (342,500) 936,460 209,000 (209,000) 374,420 1,034,950 919, 220 375,250 830 1,040, 250 5,300 936,460 17,240 342,950 (342,950) 215,175 (215,175) Exp. Dr (Cr) 1,430,376 376,300 11,000 (1,817,676) 2,407,644 1,035,000 39,000 (3,481,644) 763,481 918,990 (1,682,471) 332,500 (10,450) (450) (342,950) 0 209,000 (6,175) (215,175) 0 Exp. Balance 1,430,376 1,806,676 1,817,676 0 2,407,644 3,442,644 3,481,644 0 763,481 1,682,471 0 Approp. Cr(Dr) 1,809,750 10,000 (1,819,750) 3,491,250 (10,000) (3,481,250) 1,686,250 10,000 (1,696,250) Balance. Cr(Dr) 1,809,750 1,434,500 4,124 378,544 2,244 (8,756) 1,244 (1,818,506) (830) 3,491,250 2,451,000 43,356 1,078, 306 43,306 4,306 (5,694) (3,486,944) (5,300) 1,686,250 749,790 (13,691) 905,529 (13,461) (3,461) (1,699,711) (17,240) 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 Elimination 107 Goods received 111 Closing Entry 112 Closing Entry Appropriations-Health and Welfare 111 112 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 107 Appropriations-Culture and Recreation 109 111 112 Elimination Goods Received Closing Entry Closing Entry Appropriations-Miscellaneous 102 Budget Authorization 103 Purchase Orders 107 Elimination 107 Goods Received Utilities and Other Closing Entry Closing Entry 632,435 593,870 98,000 632,435 586,645 98,000 632,435 0 593,870 7,225 98,000 0 379,673 632,005 (1,011,678) 436,864 589,000 (1,025,864) 98,000 10,000 (108,000) 379,673 1,011,678 0 436,864 1,025,864 0 98,000 108,000 0 1,011,750 (1,011,750) 1,026,000 (1,026,000) The beginning-of-the-year fund balance was $158,260. Estimated and actual Other Financing Uses-Interfund Transfers Out totaled $50,000. Required 99,750 (99,750) a. From the ledger detail, reproduce the summary journal entries recorded in the General Fund general journal to close the operating statement and budgetary accounts at the end of the year. b. What are the amounts of encumbrances outstanding at year-end? c. Prepare a statement of revenues, expenditures, and changes in fund balance for the General Fund of the City of Green Falls for the prior year. d. Prepare a budgetary comparison schedule for the General Fund of the City of Green Falls for the prior year. 1,011,750 379,315 (358) 632,077 72 (1,011,678) 0 1,026,000 432, 130 (4,734) 581,911 (7,089) (1,033,089) (7,225) 99,750 1,750 99,750 1,750 (8,250) (108,000) 0 The finance director for the City of Green Falls printed the General Fund Revenues and Appropriations Ledgers shown below for the year just ended. Ref. 102 103 Accrued Revenue Previous Deferral 104 109 Deferral 110 Budget Amendment 111 Closing entry 112 Closing entry 102 104 110 102 103 Received in Cash 110 Budget Amendment 111 Closing Entry 112 Closing Entry 111 112 102 103 111 112 102 103 111 112 Account Description Estimated Revenues-Taxes-Real Property Budget Authorization 102 103 103 Estimated Revenues-Taxes-Sales Budget Authorization 110 111 Estimated Revenues-Interest and Penalties on Taxes Budget Authorization. Previous Deferral Budget Amendment Closing Entry Closing Entry Estimated Revenues-Licenses and Permits Budget Authorization Received in Cash Closing Entry Closing Entry REVENUES LEDGER Estimated Revenues-Fines and Forfeits Budget Authorization Received in Cash Closing Entry Closing Entry Estimated Revenues-Intergovernmental Revenue Budget Authorization Previous Deferral Received in Cash Budget Amendment Closing Entry 112 O Closing Entry Est. Revenues Dr (Cr) 6,452,400 40,000 (6,492,400) 736,250 (25,000) (711,250) 46,550 (25,000) (21,550) 460,750 (460,750) 489, 250 (489,250) 508,250 10,000 (518,250) Revenues Cr(Dr) 6,455,000 345,000 (308,000) (6,492,000) 710,600 (710,600) 21,800 (21,800) 455,050 (455,050) 493,050 (493,050) 28,500 489,250 (517,750) Balance Dr (Cr) 6,452,400 (2,600) (347,600) (39,600) 400 (6,492,000) 736,250 25,650 650 (710,600) 0 46,550 24,750 (250) (21,800) 0 460,750 5,700 (455,050) 489,250 (3,800) (493,050) 0 508,250 479,750 (9,500) 500 (517,750) Estimated Revenues-Charges for Services 102 Budget Authorization 103 Received in Cash 110 Budget Amendment 111 Closing Entry Closing Entry 112 102 103. Received in Cash Closing Entry 112 Closing Entry 111 Ref. Account Description Appropriations-General Government 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 Elimination 107 109 110 111 112 102 103 106 107 Estimated Revenues-Miscellaneous Revenues Budget Authorization 107 109 110 111 112 102 103 106 107 107 110 Goods Received Utilities and Other Budget Amendment Closing Entry Closing Entry Appropriations-Public Safety Budget Authorization Purchase Orders Payroll Elimination Goods Received Utilities and Other Budget Amendment Closing Entry Closing Entry Appropriations-Public Works Budget Authorization Purchase Orders Payroll Elimination Goods Received Budget Amendment 111 Closing Entry 112 Closing Entry 375,250 APPROPRIATIONS LEDGER Enc. Enc. Enc. Increase Decrease Balance 1,040,250 332,500 10,000 (342,500) 936,460 209,000 (209,000) 374,420 1,034,950 919, 220 375,250 830 1,040, 250 5,300 936,460 17,240 342,950 (342,950) 215,175 (215,175) Exp. Dr (Cr) 1,430,376 376,300 11,000 (1,817,676) 2,407,644 1,035,000 39,000 (3,481,644) 763,481 918,990 (1,682,471) 332,500 (10,450) (450) (342,950) 0 209,000 (6,175) (215,175) 0 Exp. Balance 1,430,376 1,806,676 1,817,676 0 2,407,644 3,442,644 3,481,644 0 763,481 1,682,471 0 Approp. Cr(Dr) 1,809,750 10,000 (1,819,750) 3,491,250 (10,000) (3,481,250) 1,686,250 10,000 (1,696,250) Balance. Cr(Dr) 1,809,750 1,434,500 4,124 378,544 2,244 (8,756) 1,244 (1,818,506) (830) 3,491,250 2,451,000 43,356 1,078, 306 43,306 4,306 (5,694) (3,486,944) (5,300) 1,686,250 749,790 (13,691) 905,529 (13,461) (3,461) (1,699,711) (17,240) 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 Elimination 107 Goods received 111 Closing Entry 112 Closing Entry Appropriations-Health and Welfare 111 112 102 Budget Authorization 103 Purchase Orders 106 Payroll 107 107 Appropriations-Culture and Recreation 109 111 112 Elimination Goods Received Closing Entry Closing Entry Appropriations-Miscellaneous 102 Budget Authorization 103 Purchase Orders 107 Elimination 107 Goods Received Utilities and Other Closing Entry Closing Entry 632,435 593,870 98,000 632,435 586,645 98,000 632,435 0 593,870 7,225 98,000 0 379,673 632,005 (1,011,678) 436,864 589,000 (1,025,864) 98,000 10,000 (108,000) 379,673 1,011,678 0 436,864 1,025,864 0 98,000 108,000 0 1,011,750 (1,011,750) 1,026,000 (1,026,000) The beginning-of-the-year fund balance was $158,260. Estimated and actual Other Financing Uses-Interfund Transfers Out totaled $50,000. Required 99,750 (99,750) a. From the ledger detail, reproduce the summary journal entries recorded in the General Fund general journal to close the operating statement and budgetary accounts at the end of the year. b. What are the amounts of encumbrances outstanding at year-end? c. Prepare a statement of revenues, expenditures, and changes in fund balance for the General Fund of the City of Green Falls for the prior year. d. Prepare a budgetary comparison schedule for the General Fund of the City of Green Falls for the prior year. 1,011,750 379,315 (358) 632,077 72 (1,011,678) 0 1,026,000 432, 130 (4,734) 581,911 (7,089) (1,033,089) (7,225) 99,750 1,750 99,750 1,750 (8,250) (108,000) 0

Expert Answer:

Answer rating: 100% (QA)

a The summary journal entries to close the operating statement and budgetary accounts at the end of the year can be derived from the ledger detail provided Here are the entries 1 Closing entry for Est... View the full answer

Related Book For

Accounting for Governmental and Nonprofit Entities

ISBN: 978-1259917059

18th edition

Authors: Jacqueline L. Reck, James E. Rooks, Suzanne Lowensohn, Daniel Neely

Posted Date:

Students also viewed these accounting questions

-

On 1/4" square grid paper, draw a structural framing plan and elevation of a 90' x 90' steel frame building at 1/4" 5'-0" scale. Framing Plan: o Columns spaced 30' on center: HSS 8x8x3/8" o Girders...

-

The finance director for the City of Green Falls printed the General Fund Revenues and Appropriations Ledgers shown below for the year just ended. The beginning-of-the-year fund balance was $160,160....

-

The printout of the Revenues and Appropriations subsidiary ledger accounts for the General Fund of the City of Augusta for the first quarter of the fiscal year appeared as follows: Required Assuming...

-

1. [20 points] A mattress manufacturer has three production facilities located in Pittsburg (PA), Houston (TX), and Los Angeles (CA). They supply their products to three distribution centers in...

-

A water pump that consumes 2 kW of electric power when operating is claimed to take in water from a lake and pump it to a pool whose free surface is 30 m above the free surface of the lake at a rate...

-

Design a differential amplifier with the configuration shown in Figure 11.28 incorporating a basic two-transistor current source to establish \(I_{Q}\). The bias voltages are to be \(V^{+}=+5...

-

Did it change your view of the company? Have you used a social network or similar site to interact with, or make comments about, an organisation?

-

Rapid Delivery, Inc. is considering the purchase of an additional delivery vehicle for $38,000 on January 1, 2010. The truck is expected to have a five-year life with an expected residual value of...

-

A $169,700 initial investment will generate the following present values of net cash flows. What is the break-even time for this investment? (PV of \$1, FV of \$1, PVA of \$1, and FVA of \$1) Note:...

-

The decedent used his own funds in the amount of $80,000 to acquire stock naming himself and his daughter as joint tenants with right of survivor ship. When the father died, the stock was worth...

-

Summarize the following types of interventions and give examples. Do not use examples given in the book. Reality orientation Remotivation Emotion Regulation Executive Functions Sensorimotor...

-

Everyone at some point has had issues with time management and procrastination in their work life, academic life and social life. How have you been handling time management issues in your life? Have...

-

You want to make three peanut butter and jelly sandwiches. What is the best way to make them that's consistent with an agile mindset? Create a sandwich assembly line, applying all the peanut butter...

-

1 pts Joan Reed exchanges commercial real estate that she owns for other commercial real estate, plus $50,000 cash. The following additional information pertains to this transaction: Property given...

-

It is believed that 86% of Padres fans would have liked Trevor Hoffman to remain in San Diego to finish out his career as a San Diego Padre. You would like to simulate asking 10 Padres fans their...

-

The videos below cover why American higher education, including public colleges and universities, is so expensive. They also explore factors that have resulted in the current student loan debt...

-

1 A. Rough Stuff makes 2 products: khaki shorts and khaki pants for men. Each product passes through the cutting machine area, which is the chief constraint during production. Khaki shorts take 15...

-

Whats the difference between an ordinary annuity and an annuity due? What type of annuity is shown below? How would you change the time line to show the other type of annuity?

-

Forest City has recently implemented GAAP reporting and is attempting to determine which of the following special revenue funds should be classified as major funds and therefore be reported in...

-

What are the three broad categories of service efforts and accomplishments (SEA) measures? Provide an example of each.

-

You completed a managerial accounting class last semester and learned about budgeting concepts. How do government budgeting concepts differ from those used in a corporate setting?

-

7. If a subsidiary purchases parent bonds at a price in excess of recorded book value, is the gain or loss attributed to the parent or the subsidiary? Explain.

-

PR 6-2 What information should be disclosed about property, plant, and equipment in the consolidated financial statements?

-

1. What reciprocal accounts arise when one company borrows from an affiliate?

Study smarter with the SolutionInn App