Question: The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 10 % 0.95 35 % B 17 1.50 45 The

The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 10 % 0.95 35 % B 17 1.50 45 The market index has a standard deviation of 19% and the risk-free rate is 12%. a) What are the standard deviations of stocks A and B? b) Suppose we build a portfolio with the following proportion: 0.35 in stock A, 0.35 in stock B, and 0.3 in riskfree T-bills. Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio

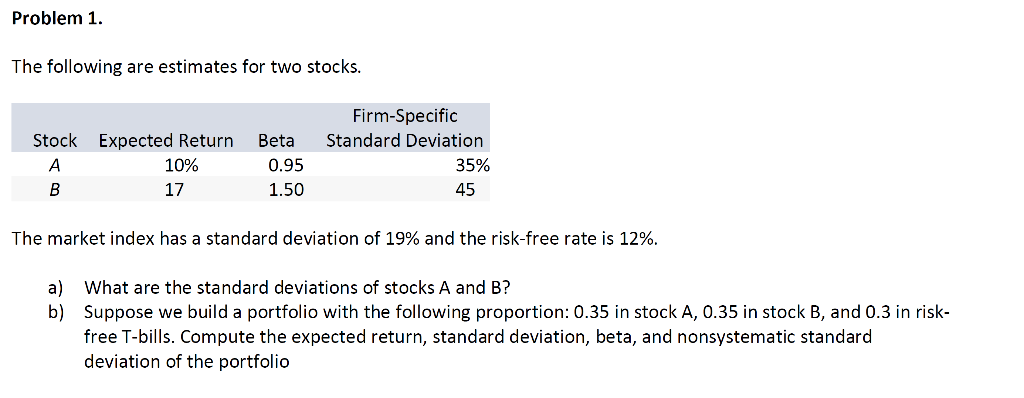

Problem 1. The following are estimates for two stocks. Stock A B Expected Return 10% 17 Beta 0.95 1.50 Firm-Specific Standard Deviation 35% 45 The market index has a standard deviation of 19% and the risk-free rate is 12%. a) What are the standard deviations of stocks A and B? b) Suppose we build a portfolio with the following proportion: 0.35 in stock A, 0.35 in stock B, and 0.3 in risk- free T-bills. Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts