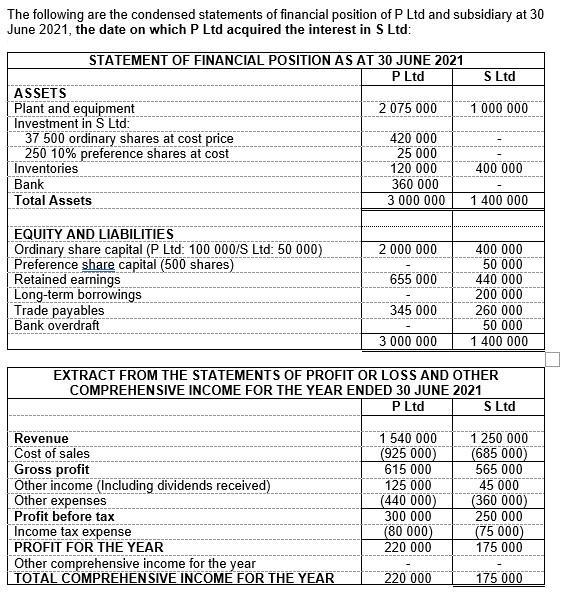

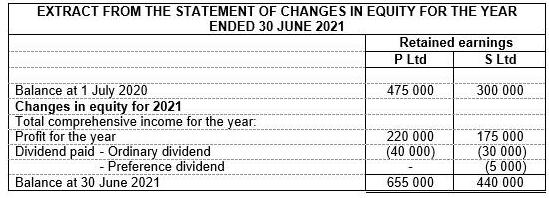

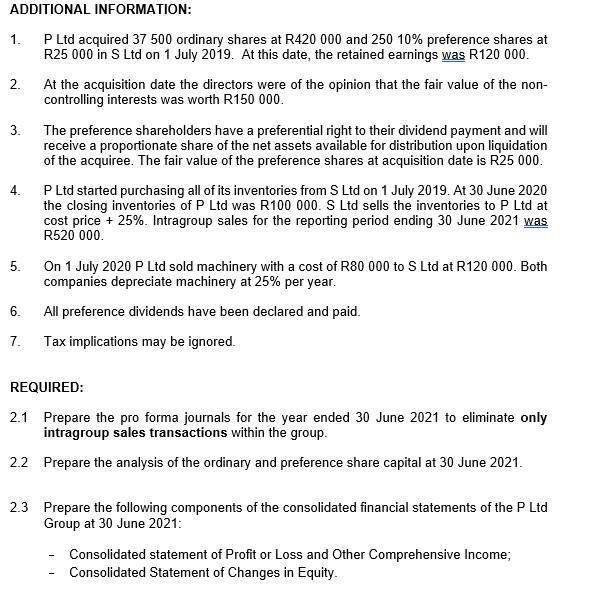

The following are the condensed statements of financial position of P Ltd and subsidiary at 30...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following are the condensed statements of financial position of P Ltd and subsidiary at 30 June 2021, the date on which P Ltd acquired the interest in S Ltd: STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2021 P Ltd S Ltd ASSETS Plant and equipment Investment in S Ltd: 37 500 ordinary shares at cost price 250 10% preference shares at cost Inventories Bank Total Assets 2 075 000 1 000 000 420 000 25 000 120 000 400 000 360 000 3 000 000 1 400 000 EQUITY AND LIABILITIES Ordinary share capital (P Ltd: 100 000/S Ltd: 50 000) Preference share capital (500 shares) Retained earnings Long-term borrowings Trade payables Bank overdraft 400 000 50 000 440 000 200 000 260 000 50 000 2 000 000 655 000 345 000 3 000 000 1 400 000 EXTRACT FROM THE STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2021 P Ltd S Ltd 1 540 000 (925 000) Revenue Cost of sales Gross profit Other income (Including dividends received) Other expenses Profit before tax Income tax expense PROFIT FOR THE YEAR Other comprehensive income for the year TOTAL COMPREHENSIVE INCOME FOR THE YEAR 1 250 000 (685 000) 615 000 125 000 (440 000) 300 000 (80 000) 220 000 565 000 45 000 (360 000) 250 000 (75 000) 175 000 220 000 175 000 EXTRACT FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2021 Retained earnings P Ltd S Ltd Balance at 1 July 2020 Changes in equity for 2021 Total comprehensive income for the year. Profit for the year Dividend paid - Ordinary dividend 475 000 300 000 220 000 175 000 (30 000) (5 000) 440 000 (40 000) - Preference dividend Balance at 30 June 2021 655 000 ADDITIONAL INFORMATION: 1. P Ltd acquired 37 500 ordinary shares at R420 000 and 250 10% preference shares at R25 000 in S Ltd on 1 July 2019. At this date, the retained earnings was R120 000. 2. At the acquisition date the directors were of the opinion that the fair value of the non- controlling interests was worth R150 000. 3. The preference shareholders have a preferential right to their dividend payment and will receive a proportionate share of the net assets available for distribution upon liquidation of the acquiree. The fair value of the preference shares at acquisition date is R25 000. 4. P Ltd started purchasing all of its inventories from S Ltd on 1 July 2019. At 30 June 2020 the closing inventories of P Ltd was R100 000. S Ltd sells the inventories to P Ltd at cost price + 25%. Intragroup sales for the reporting period ending 30 June 2021 was R520 000. 5. On 1 July 2020 P Ltd sold machinery with a cost of R80 000 to S Ltd at R120 000. Both companies depreciate machinery at 25% per year. 6. All preference dividends have been declared and paid. 7. Tax implications may be ignored. REQUIRED: 2.1 Prepare the pro forma journals for the year ended 30 June 2021 to eliminate only intragroup sales transactions within the group. 2.2 Prepare the analysis of the ordinary and preference share capital at 30 June 2021. 2.3 Prepare the following components of the consolidated financial statements of the P Ltd Group at 30 June 2021: Consolidated statement of Profit or Loss and Other Comprehensive Income; Consolidated Statement of Changes in Equity. The following are the condensed statements of financial position of P Ltd and subsidiary at 30 June 2021, the date on which P Ltd acquired the interest in S Ltd: STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2021 P Ltd S Ltd ASSETS Plant and equipment Investment in S Ltd: 37 500 ordinary shares at cost price 250 10% preference shares at cost Inventories Bank Total Assets 2 075 000 1 000 000 420 000 25 000 120 000 400 000 360 000 3 000 000 1 400 000 EQUITY AND LIABILITIES Ordinary share capital (P Ltd: 100 000/S Ltd: 50 000) Preference share capital (500 shares) Retained earnings Long-term borrowings Trade payables Bank overdraft 400 000 50 000 440 000 200 000 260 000 50 000 2 000 000 655 000 345 000 3 000 000 1 400 000 EXTRACT FROM THE STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2021 P Ltd S Ltd 1 540 000 (925 000) Revenue Cost of sales Gross profit Other income (Including dividends received) Other expenses Profit before tax Income tax expense PROFIT FOR THE YEAR Other comprehensive income for the year TOTAL COMPREHENSIVE INCOME FOR THE YEAR 1 250 000 (685 000) 615 000 125 000 (440 000) 300 000 (80 000) 220 000 565 000 45 000 (360 000) 250 000 (75 000) 175 000 220 000 175 000 EXTRACT FROM THE STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2021 Retained earnings P Ltd S Ltd Balance at 1 July 2020 Changes in equity for 2021 Total comprehensive income for the year. Profit for the year Dividend paid - Ordinary dividend 475 000 300 000 220 000 175 000 (30 000) (5 000) 440 000 (40 000) - Preference dividend Balance at 30 June 2021 655 000 ADDITIONAL INFORMATION: 1. P Ltd acquired 37 500 ordinary shares at R420 000 and 250 10% preference shares at R25 000 in S Ltd on 1 July 2019. At this date, the retained earnings was R120 000. 2. At the acquisition date the directors were of the opinion that the fair value of the non- controlling interests was worth R150 000. 3. The preference shareholders have a preferential right to their dividend payment and will receive a proportionate share of the net assets available for distribution upon liquidation of the acquiree. The fair value of the preference shares at acquisition date is R25 000. 4. P Ltd started purchasing all of its inventories from S Ltd on 1 July 2019. At 30 June 2020 the closing inventories of P Ltd was R100 000. S Ltd sells the inventories to P Ltd at cost price + 25%. Intragroup sales for the reporting period ending 30 June 2021 was R520 000. 5. On 1 July 2020 P Ltd sold machinery with a cost of R80 000 to S Ltd at R120 000. Both companies depreciate machinery at 25% per year. 6. All preference dividends have been declared and paid. 7. Tax implications may be ignored. REQUIRED: 2.1 Prepare the pro forma journals for the year ended 30 June 2021 to eliminate only intragroup sales transactions within the group. 2.2 Prepare the analysis of the ordinary and preference share capital at 30 June 2021. 2.3 Prepare the following components of the consolidated financial statements of the P Ltd Group at 30 June 2021: Consolidated statement of Profit or Loss and Other Comprehensive Income; Consolidated Statement of Changes in Equity.

Expert Answer:

Answer rating: 100% (QA)

1 Pro forma journals for the year ended 30 June 2021 to eliminate only intragroup sales transactions within the group Dr Cr Revenue Ac 520000 To Purchase Ac 520000 Cost of sales 4000 To Inventories 40... View the full answer

Posted Date:

Students also viewed these accounting questions

-

The comparative condensed statements of financial position of Garcia SLU are presented below. GARCIA SLU Comparative Condensed Statements of Financial Position December 31 Instructions (a) Prepare a...

-

The comparative condensed statements of financial position of Garcia Corporation are presented below. Garcia Corporation Comparative Condensed Statements of Financial Position December 31...

-

The comparative condensed statements of financial position of Garcia SLU are presented below. Instructions a. Prepare a horizontal analysis of the statement of financial position data for Garcia...

-

Write a program, in Java, to convert from binary to decimal andfrom from binary to hexadecimal. Please use instance variables,preferably strings. The program must do the conversion withoutusing any...

-

A good safety management program requires several steps. What are they? Write a short management training program which would get this message across.

-

In 1972, Irwin Fox and Alvin Samuels established Ironite. The articles of incorporation set forth the guidelines for operation. Irwin and Alvin agreed verbally on additional decisions about the...

-

Jennifer is a salesperson for a major chemical company doing business in China. To close a multimillion-dollar contract, she has been asked by a Chinese government official for a payment of...

-

Prepare a comparative common-size income statement for McMahon Music Co., using the 2012 and 2011 data of Exercise 13-16A and rounding to four decimal places.

-

(a) Explain the following terms as used in international finance: (i) Floating rate notes (FRNs). (1 mark) (ii) Forfaiting. (1 mark) (iii) Crowd funding. (1 mark) (iv) Green bond. (1 mark) (b) One of...

-

Pure Plant Beauty is a sole proprietorship that has a developed a new line of skin care and makeup that uses natural and organic ingredients. The company showed the following adjusted account...

-

Pen Supply Corp. began operations on March 1, 20Y5. On this date, the company paid for the below expenses: legal fees related to organisation, $5,000; rent for the upcoming month, $1,500; license...

-

A motor of \(5 \mathrm{~kW}\) running at \(950 \mathrm{rpm}\) is used in a riveting machine. A flywheel is attached to the machine has a mass of \(100 \mathrm{~kg}\) and radius of gyration of \(0.4...

-

A porter governor has an equal arm's length of \(220 \mathrm{~mm}\) long and pivoted at the axis of rotation. Each ball has a mass of \(5 \mathrm{~kg}\) and the mass of central load on the sleeve is...

-

A Proell governor has an equal arm's length of \(420 \mathrm{~mm}\). The upper and lower ends of the arms are pivoted on the axis of the governor. The extension arms of the lower links are each 80...

-

In a flat belt drive prove that \(\frac{T_{1}}{T_{2}}=e^{\mu \theta}\); where \(T_{1}\) is tension in tight side, \(T_{2}\) is tension in slack side, \(\mu\) is coefficient of friction, \(\theta\) is...

-

The speed of a driving shaft is \(80 \mathrm{rpm}\) and the speed of the driven shaft is \(120 \mathrm{rpm}\). The diameter of the driving pulley is given as \(600 \mathrm{~mm}\). Find the diameter...

-

Query criteria is case sensitive and must match exactly to return the desired results. :TrueFalse

-

What are the 5 Cs of marketing channel structure?

-

A sample of ideal gas is in a sealed container. The temperature of the gas and the volume of the container are both increased. What other properties of the gas necessarily change? (More than one...

-

An aluminum ring is tight around a solid iron rod. If we wish to loosen the ring to remove it from the rod, we should A. Increase the temperature of the ring and rod. B. Decrease the temperature of...

-

Jn Figure 12.22, by comparing the slope of the graph during the time the liquid water is warming to the slope as steam is warming, we can say that A. The specific heat of water is larger than that of...

Study smarter with the SolutionInn App