The following information is also available: a) On 01 May 2010 Deer plc paid 400,000 to purchase

Question:

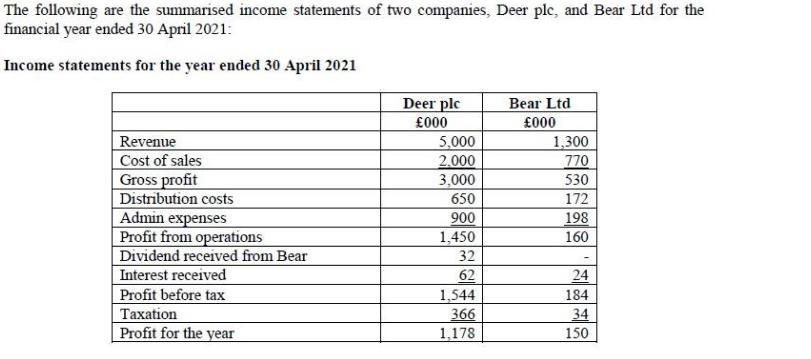

The following information is also available:

a) On 01 May 2010 Deer plc paid £400,000 to purchase 160,000 ordinary shares in Bear Ltd. At that date, Bear Ltd had in issue a total of 200,000 Ordinary shares. Bear Ltd has not issued any ordinary shares since this date. Shares in Deer plc and Bear Ltd have a nominal value of £1.

b) At the date of acquisition, Bear Ltd had retained earnings of £60,000, a share premium account of £100,000, and the fair value of non-current assets in Bear Ltd was £90,000 more than book value. Non-current assets in Bear Ltd have since been adjusted to reflect this. Bear Ltd has not re-valued any non-current assets since this date.

c) During the year ended 30 April 2021, Deer plc sold goods to Bear Ltd for £200,000. These had been marked up by 25%. At 30 April 2021 Bear Ltd still had 40% of these goods in closing inventory.

d) During the year Deer plc paid dividends of £400,000.

e) Retained earnings at 01 May 2020 were:

i. Deer plc - £950,000

ii. Bear Ltd - £200,000

f) A review at 30 April 2021 established impairment of goodwill in the investment in Bear Ltd amounting to £40,000 in the year.

g) The non-controlling interest was in the case of this acquisition, calculated by the normal proportionate share of net assets method.

Required:

(a) Calculate the goodwill arising on the acquisition of Bear Ltd at 01 May 2010.

(b) Prepare a consolidated statement of comprehensive income for the year ended 30 April 2021. Your answer should distinguish between profit for the year attributable to the non-controlling interest and that attributable to the group.

(c) Calculate consolidated retained earnings for the year ended 30 April 2021.

Expert Answer:

a The goodwill arising on the acquisition of Bear Ltd at 01 May 2010 Particulars Amount Consideratio... View the full answer

Fundamental financial accounting concepts

ISBN: 978-0078025365

8th edition

Authors: Thomas P. Edmonds, Frances M. Mcnair, Philip R. Olds, Edward