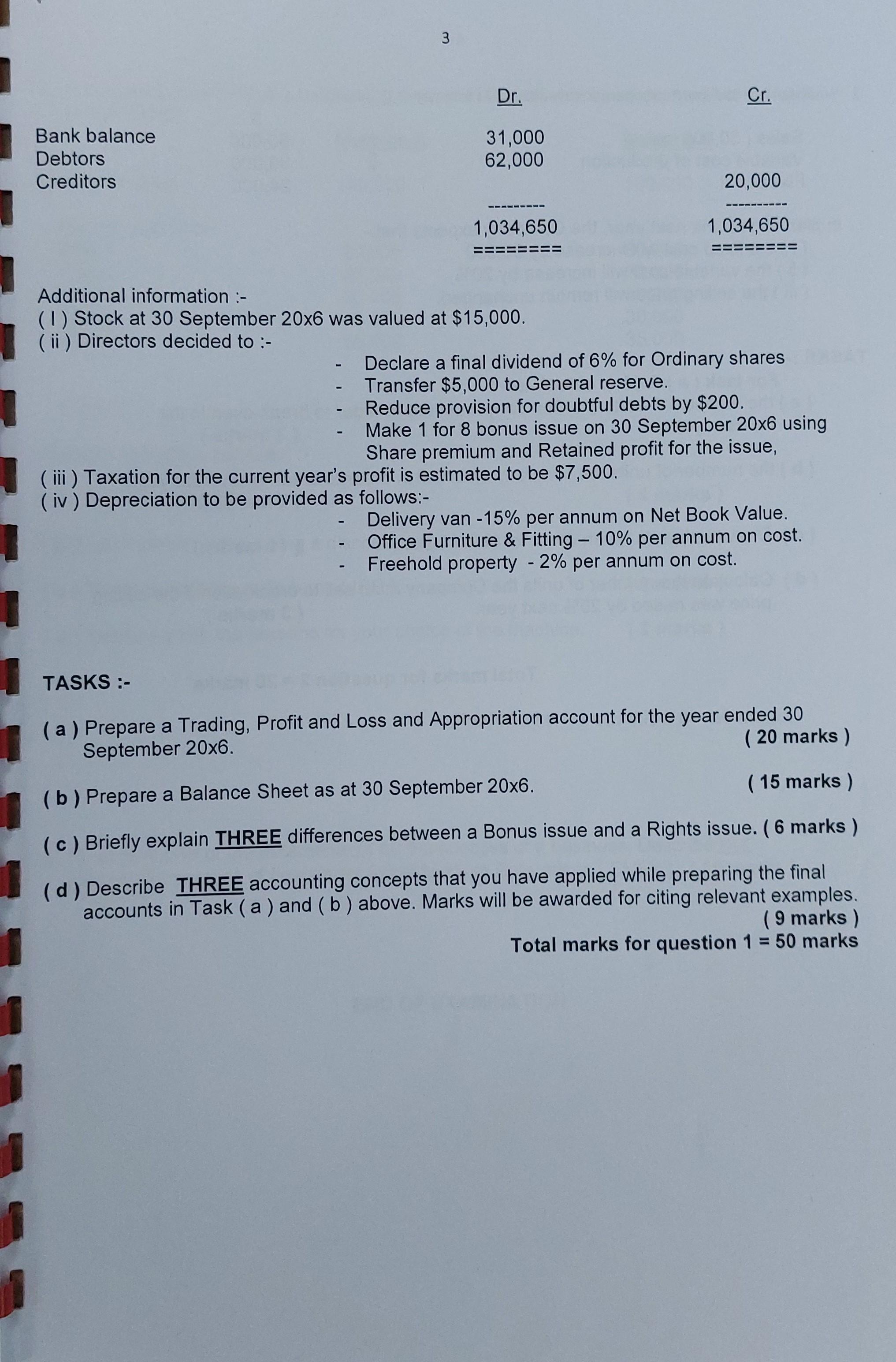

The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

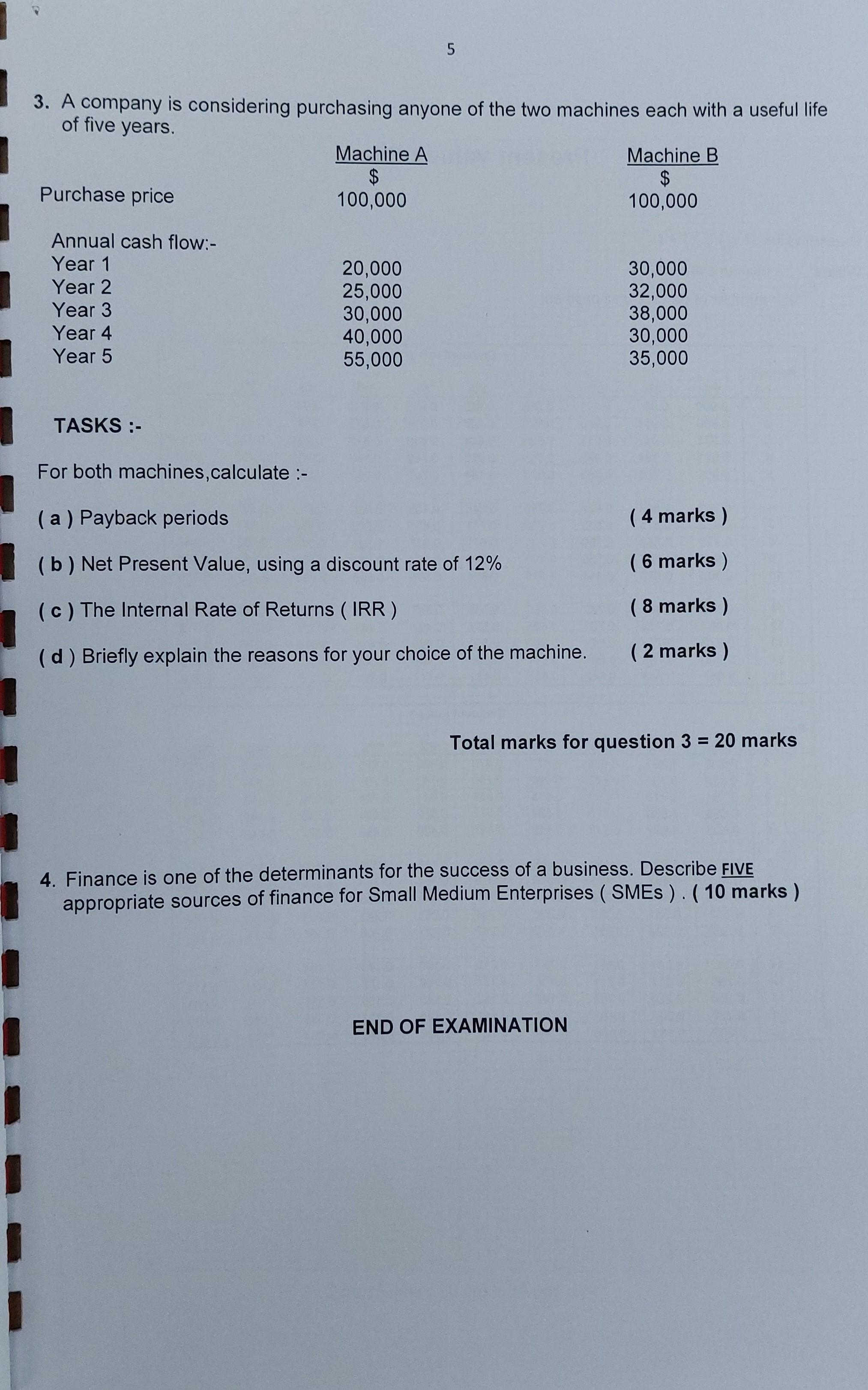

The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074 The following is the trial balance of XLC plc as at 30th September 20x6. Dr. Cr. 200,000 100,000 80,000 40,000 535,000 Ordinary share capital ($1 each) 6% Preference share capital( $2 each) 8% Debentures (repayable in 20x9) General reserve Sales Purchases Directors' remuneration Office rent Office salaries Returns inwards Returns outwards Stock at 1.10.20x5 Retained profit @ 1.10.20x5 Auditors' fee Office lighting Printing and stationery Salesman's commission Debenture interest Warehouse rent Delivery van expenses Rental income from sub-letting of warehouse Interim dividend paid - Preference Interim dividend paid - Ordinary Discounts Carriage inwards Carriage outwards Advertising expenses 2 Share premium Delivery van- at cost Office furniture and fittings - at cost Freehold property -at cost Provision for depreciation - Delivery van Provision for doubtful debts - 247,000 44,600 50,000 84,000 3,000 14,200 7,850 3,600 9.600 1,800 1,100 6,400 Officeice F & F Freehold property 3,200 3,000 6,000 900 7,200 2,600 4,600 46,000 25,000 370,000 12,400 11,500 2,100 2,400 15,000 6,900 2,500 6,400 450 Bank balance Debtors Creditors 3 ✔ Dr. 31,000 62,000 Additional information :- (1) Stock at 30 September 20x6 was valued at $15,000. (ii) Directors decided to :- - 1,034,650 - Declare a final dividend of 6% for Ordinary shares Transfer $5,000 to General reserve. Cr. (iii) Taxation for the current year's profit is estimated to be $7,500. (iv) Depreciation to be provided as follows:- 20,000 1,034,650 Reduce provision for doubtful debts by $200. Make 1 for 8 bonus issue on 30 September 20x6 using Share premium and Retained profit for the issue, Delivery van -15% per annum on Net Book Value. Office Furniture & Fitting - 10% per annum on cost. Freehold property - 2% per annum on cost. PAT TASKS :- (a) Prepare a Trading, Profit and Loss and Appropriation account for the year ended 30 September 20x6. (20 marks) (b) Prepare a Balance Sheet as at 30 September 20x6. (15 marks) (c) Briefly explain THREE differences between a Bonus issue and a Rights issue. (6 marks) (d) Describe THREE accounting concepts that you have applied while preparing the final accounts in Task (a) and (b) above. Marks will be awarded for citing relevant examples. (9 marks) Total marks for question 1 = 50 marks 4 2 Weststar Sdn Bhd's current operating results are as follows:- Sales (30,000 units) Variable cost of production Fixed cost In planning for the next year, the Company expects that:- (i) the fixed cost will increase by $5,000 (ii) the variable cost will increase by 20% (iii) the selling price will remain unchanged. TASKS :- $ 60,000 30,000 24,000 For task (a ) & (b), calculate:- (a) the number of units the Company must sell in order to break-even in the Current year. (3 marks) (b) the number of units the company must sell in order to break-even Next year. (3 marks). (11 marks) (c) Draw the break-even Chart for task (ii) above. (d) Calculate the number of units the Company must sell to break-even if the selling price was raised by 25% next year. (3 marks) Total marks for question 2 = 20 marks 3. A company is considering purchasing anyone of the two machines each with a useful life of five years. Purchase price Annual cash flow:- Year 1 Year 2 Year 3 Year 4 Year 5 Machine A $ 100,000 20,000 25,000 30,000 5 40,000 55,000 TASKS :- For both machines, calculate :- (a) Payback periods (b) Net Present Value, using a discount rate of 12% (c) The Internal Rate of Returns (IRR) (d) Briefly explain the reasons for your choice of the machine. Machine B $ 100,000 30,000 32,000 38,000 30,000 35,000 END OF EXAMINATION (4 marks) (6 marks) (8 marks) (2 marks) Total marks for question 3 = 20 marks 4. Finance is one of the determinants for the success of a business. Describe FIVE appropriate sources of finance for Small Medium Enterprises (SMEs). (10 marks) Present value of 1, i.e. (1 + r) " Where r discount rate n = number of periods until payment Periods (n) 1 5 6 7 8 9 10 11 12. 13 14 15 8799 1% 0.990 0.980 0.971 0.961 0.951 6 Periods (n) 1 2 3 4 5 0.593 Present value table 4% 0.962 0.925 0.889 0.855 0.863 0.822 0.942 0.888 0.837 0.933 0.871 0.813 0.923 0.853 0.789 0.914 0.837 0.766 0.905 0.820 0.744 2% 3% 0.980 0.971 0.961 0.943 0.942 0.915 0.924 0.888 0.906 0.879 0.896 0.804 0.722 0.650 0.625 0.701 0.887 0.788 0.601 0.681 0.773 0.661 0.577 0.758 0.743 0.870 0.861 0.642 0.555 9 0.391 10 0.352 11% 12% 13% 0.893 0.885 0.901 0.812 0.797 0.783 0.731 0.712 0.659 0.636 0.567 0.535 0.507 0.480 0.482 0.452 0.425 0.434 0.404 0.376 0.361 0.333 0.322 0.295 Discount rate (r) 7% 8% 9% 0.935 0.926 0.917 0.873 0.890 0.857 0.842 0.840 0.816 0.794 0.772 0.792 0.763 0.735 0.708 0.747 0.713 0.681 0.650 0.456 0.400 0.351 0.308 0.270 5% 6% 0.952 0.943 0.907 0.864 0.823 0.784 0.746 0.705 0.790 0.760 0.711 0.731 0.703 0.645 0.665 0.627 0.677 0.592 0.676 0.614 0.558 0.585 0.527 0.557 0.497 0.530 0.469 0.505 0.442 0.481 0.417 Discount rate (r) 0.666 0.630 0.623 0.583 0.582 0.540 0.544 0.500 0.508 0.463 14% 15% 16% 17% 0.877 0.870 0.862 0.855 0.769 0.756 0.743 0.731 0.693 0.675 0.658 0.641 0.613 0.592 0.572 0.552 0.543 0.519 0.497 0.476 0.432 0.410 0.376 0.354 0.327 0.305 0.284 0.263 0.247 0.227 0.475 0.429 0.388 0.444 0.397 0.356 0.415 0.368 0.326 0.340 0.299 0.388 0.362 0.315 0.275 0.596 0.547 0.502 18% 19% 0.847 0.840 0.718 0.706 0.624 0.609 0.593 0.534 0.516 0.499 0.456 0.437 0.419 0.390 0.333 0.285 0.266 0.460 0.422 0.370 0.314 0.352 0.296 0.249 0.243 0.225 0.209 0.208 0.191 0.176 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0 148 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467 0.424 0.386 0.350 0.319 0.290 0.263 0.239 20% 0.833 0.694 0.579 0.482 0.402 0.335 0.279 0.233 0.194 0.162 0.135 0.112 0.116 0.104 0.093 0.099 0.088 0.078 0.065 0.084 0.074

Expert Answer:

Answer rating: 100% (QA)

XL PIC TRADING ProFit and Loss Account FOR THE YEAR ENDED 300920x6 Sales DR Openi... View the full answer

Related Book For

Advanced Financial Accounting

ISBN: 978-0137030385

6th edition

Authors: Thomas Beechy, Umashanker Trivedi, Kenneth MacAulay

Posted Date:

Students also viewed these accounting questions

-

Following is the trial balance of the Platteville Golf Club, Inc. as of December 31. The books are closed annually on December 31. Instructions (a) Enter the balances in ledger accounts. Allow five...

-

Following is the trial balance of Rashid Products Company, Inc., as of December 31 of this year. You are given the following information for the adjustments: a. f. Year- end inventories: raw...

-

The following is the trial balance for Jills Fitness Centre of Etobicoke for December 31, 2013. Given The following adjustment data on December 31: a. Fitness supplies on hand, $900 b. Amortization...

-

Assume that you are looking at three perpetuities. Perpetuity 1 (P) has annual cash flows of $850 in Years 1 through infinity (1 - oo) and a present value at Year 0 of $10,119.047619. Perpetuity 2...

-

What is the difference between the R& D phase for internally generated intangibles?

-

Two alcohols, isopropyl alcohol and propyl alcohol, have the same molecular formula, C 3 H 8 O. A solution of the two that istwo-thirds by mass isopropyl alcohol has a vapor pressure of 0.110 atm at...

-

With reference to the preceding exercise, test the null hypothesis \(\beta=0.75\) against the alternative hypothesis \(\beta <0.75\) at the 0.10 level of significance.

-

1. What micro-environmental factors have affected Fitbit since it opened for business? 2. How should Fitbit overcome the threats and obstacles it faces? 3. What factors in the marketing environment...

-

Explain why a notable innovation through virtual reality (VR) and augmented reality (AR) technologies is so innovative in sport? Why should sports leaders cultivate a culture of openness and...

-

Kai is the president of Zebra Antiques. An employee, Reese Francis, is due a raise. Reeses current benefit analysis is as follows: Compute the benefit analysis assuming: 3 percent increase in pay. ...

-

BioShamp is a global shampoo brand with its own store in Singapore. The company sells three types of shampoo - silky smooth, hair fall and dandruff. All shampoos are produced at their single...

-

What is a Project Management Information System (PMIS)?

-

What is stakeholder co-creation?

-

What two key models of communication were introduced in this chapter and when would one be preferred over the other?

-

What does mapping stakeholders in the Contribution/Commitment Grid enable the project manager to do?

-

What does the control strategy 'escalate' mean to the project manager?

-

make a Balance sheet using this information in the Trial Balance. Separate BS for 2022 and 2023. A B 1 2 234 C D E J.K HOTEL CEBU TRIAL BALANCE AS OF DECEMBER 31, 2022 and 2023 5 AMOUNTS 6 ACCOUNT...

-

Open Text Corporation provides a suite of business information software products. Exhibit 10-9 contains Note 10 from the companys 2013 annual report detailing long-term debt. Required: a. Open Text...

-

Muskoka Furniture Inc. (Muskoka) imports pine furniture from factories around the world for sale to retailers in Canada. On October 31, 20X4, Muskoka bought bedroom furniture set from a supplier in...

-

How do unrealized profits on upstream sales affect the non-controlling interests share of a subsidiarys earnings?

-

What is a fair-value hedge?

-

In July 2022, in a press conference after a meeting of the FOMC, a reporter asked Chair Powell the following question: Within the Fed, there are staff economists whove argued that NAIRU, the...

-

In early 2021, an article in the New York Times quoted Fed Chair Jerome Powell as saying that a robust job market can be sustained without causing an outbreak of inflation. a. What did Powell mean by...

-

What role did the natural rate of unemployment traditionally play in the Feds approach to monetary policy? How does the new monetary policy strategy the Fed announced in 2020 affect that role?

Study smarter with the SolutionInn App