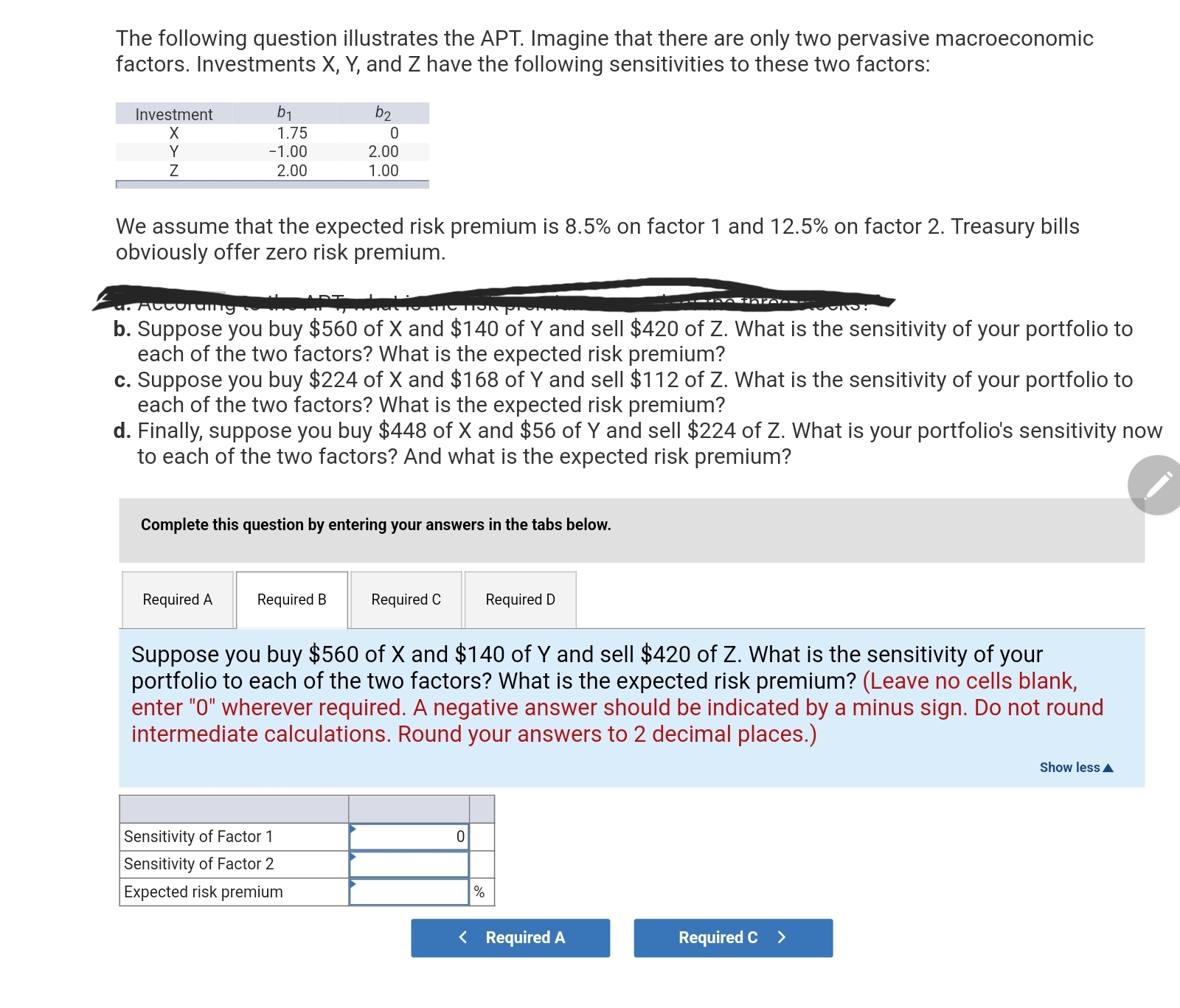

The following question illustrates the APT. Imagine that there are only two pervasive macroeconomic factors. Investments...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following question illustrates the APT. Imagine that there are only two pervasive macroeconomic factors. Investments X, Y, and Z have the following sensitivities to these two factors: Investment b b2 X 1.75 0 Y -1.00 2.00 Z 2.00 1.00 We assume that the expected risk premium is 8.5% on factor 1 and 12.5% on factor 2. Treasury bills obviously offer zero risk premium. According b. Suppose you buy $560 of X and $140 of Y and sell $420 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? c. Suppose you buy $224 of X and $168 of Y and sell $112 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? d. Finally, suppose you buy $448 of X and $56 of Y and sell $224 of Z. What is your portfolio's sensitivity now to each of the two factors? And what is the expected risk premium? Complete this question by entering your answers in the tabs below. Required A Required B Required C Required D Suppose you buy $560 of X and $140 of Y and sell $420 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? (Leave no cells blank, enter "0" wherever required. A negative answer should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.) Sensitivity of Factor 1 Sensitivity of Factor 2 Expected risk premium 0 % < Required A Required C > Show less The following question illustrates the APT. Imagine that there are only two pervasive macroeconomic factors. Investments X, Y, and Z have the following sensitivities to these two factors: Investment b b2 X 1.75 0 Y -1.00 2.00 Z 2.00 1.00 We assume that the expected risk premium is 8.5% on factor 1 and 12.5% on factor 2. Treasury bills obviously offer zero risk premium. According b. Suppose you buy $560 of X and $140 of Y and sell $420 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? c. Suppose you buy $224 of X and $168 of Y and sell $112 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? d. Finally, suppose you buy $448 of X and $56 of Y and sell $224 of Z. What is your portfolio's sensitivity now to each of the two factors? And what is the expected risk premium? Complete this question by entering your answers in the tabs below. Required A Required B Required C Required D Suppose you buy $560 of X and $140 of Y and sell $420 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium? (Leave no cells blank, enter "0" wherever required. A negative answer should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.) Sensitivity of Factor 1 Sensitivity of Factor 2 Expected risk premium 0 % < Required A Required C > Show less

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Night By Elie Wiesel The Holocaust - Why did the members of Sighets Jewish community refuse to believe their horrible situation? (Moshe the Beadle and Madame Schachter portending the horrors that...

-

A tungsten filament is heated to 2700 K. At what wavelength is the maximum amount of radiation emitted? What fraction of the total energy is in the visible range (0.4 to 0.75 m m)?Assume that the...

-

Discuss, using the concept of a load line, how a simple common-source circuit can amplify a time-varying signal.

-

What would a cultural assessment gap analysis contain?

-

With a portfolio as diverse as Googles, what are the companys core brand values?

-

The domestic and international financial marketplace. Topic include financial markets, types of financial intermediaries, the form and methods of stock market operation, the stock market,...

-

\f\f

-

discuss the implications of geopolitical tensions, regulatory changes, and technological innovations on SWIFT's role as a critical infrastructure provider for global financial messaging, and how does...

-

Dark Days at Sunnyvale: Can Teamwork Part the Clouds? The Sunnyvale Resort is a 300-room luxury property with a lake on one side and a golf course, riding stables, and tennis courts on the other....

-

Ankur has N magic sticks, each of some length. All magic sticks are of fixed length and cannot be broken. Now Ankur wants to build a square using exactly 6 of those magic sticks. Now Ankur wonders in...

-

1. Describe three ways that HRM in public service organizations differs according to whether the context is governmental or nonprofit. Look at Figure 1.2 and how the functions are categorized as...

-

Find a common (i.e., a shared resource) that is tragic (i.e., is inevitably degraded) in your own life. It may be something that you observe in your town, job, school, or home, but it must have the...

-

Calculate the future value of the following yearly cash flows at the end of the fifth year assuming a 20% return annum. Year 1 2 3 4 5 Cash Flow (GH) 1000 600 400 200 100 b. Daniel Otu borrowed GH...

-

1. Following are information about Alhadaf Co. Cost incurred Inventory Purchases Sales Adverting expense Salary Expense Depreciation Beginning Inventory Ending Inventory Amount 118,000 350.000 90,000...

-

Discuss the reasoning behind the expected value concept.

-

You have heard the following statements made. Comment critically on them. (a) Equity only increases or decreases as a result of the owners putting more cash into the business or taking some out. (b)...

-

You have been talking to someone who had read a few chapters of an accounting text some years ago. During your conversation the person made the following statements: (a) The income statement shows...

Study smarter with the SolutionInn App