Question: The following regression output has been generated by estimating the index model for stocks B using monthly return data for the period from January 2017

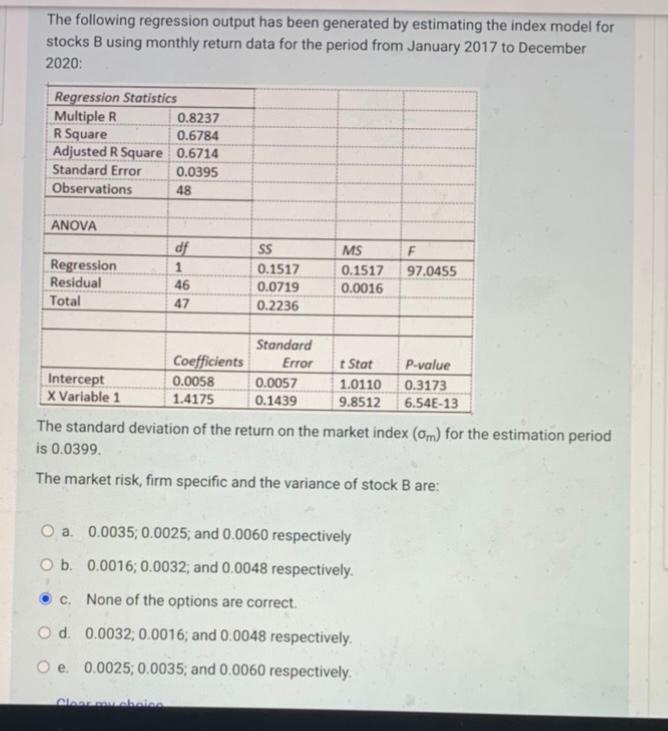

The following regression output has been generated by estimating the index model for stocks B using monthly return data for the period from January 2017 to December 2020: Regression Statistics Multiple R 0.8237 R Square 0.6784 Adjusted R Square 0.6714 Standard Error 0.0395 Observations 48 ANOVA F df 1 46 47 Regression Residual Total 97.0455 SS 0.1517 0.0719 0.2236 MS 0.1517 0.0016 Standard Coefficients Error t Stot P-value Intercept 0.0058 0.0057 1.0110 0.3173 X Variable 1 1.4175 0.1439 9.8512 6.54E-13 The standard deviation of the return on the market index (om) for the estimation period is 0.0399 The market risk, firm specific and the variance of stock B are: O a. 0.0035, 0.0025; and 0.0060 respectively O b. 0.0016; 0.0032, and 0.0048 respectively. c. None of the options are correct. Od 0.0032;0.0016; and 0.0048 respectively O e. 0.0025, 0.0035, and 0.0060 respectively Alan..bec

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts