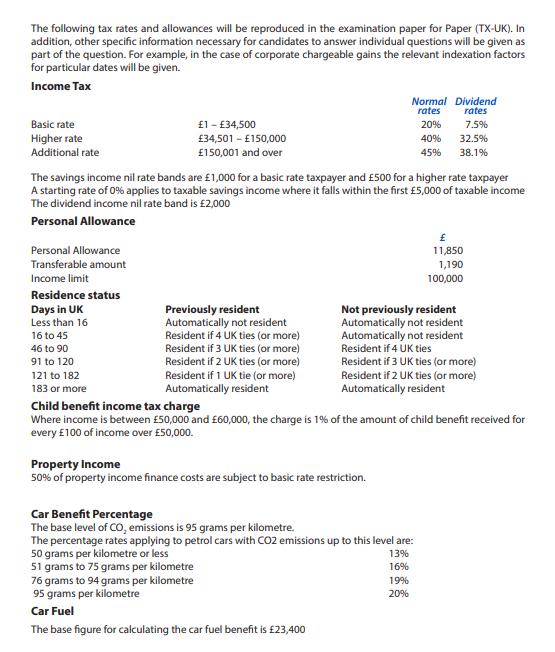

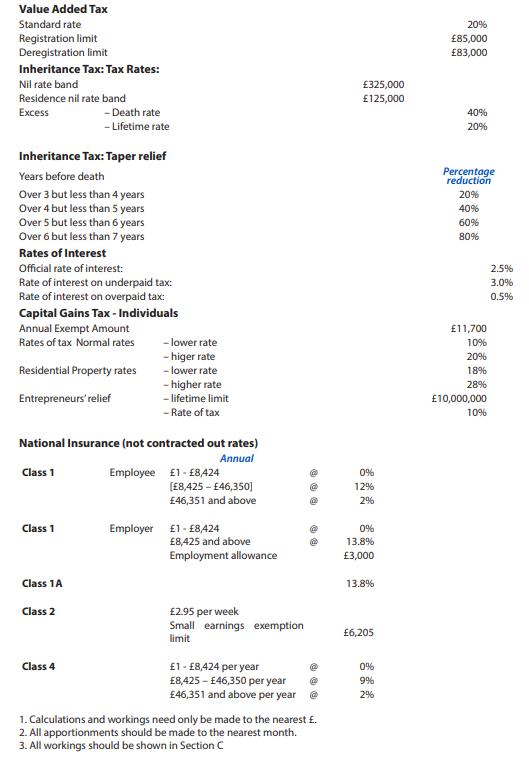

The following tax rates and allowances will be reproduced in the examination paper for Paper (TX-UK)....

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following tax rates and allowances will be reproduced in the examination paper for Paper (TX-UK). In addition, other specific information necessary for candidates to answer individual questions will be given as part of the question. For example, in the case of corporate chargeable gains the relevant indexation factors for particular dates will be given. Income Tax Normal Dividend rates rates Basic rate £1 - £34,500 20% 7.5% Higher rate Additional rate £34,501 - £150,000 £150,001 and over 40% 32.5% 45% 38.1% The savings income nil rate bands are £1,000 for a basic rate taxpayer and £500 for a higher rate taxpayer A starting rate of 0% applies to taxable savings income where it falls within the first £5,000 of taxable income The dividend income nil rate band is £2,000 Personal Allowance Personal Allowance 11,850 Transferable amount 1,190 Income limit 100,000 Residence status Days in UK Less than 16 Previously resident Automatically not resident Resident if 4 UK ties (or more) Resident if 3 UK ties (or more) Resident if 2 UK ties (or more) Not previously resident Automatically not resident Automatically not resident 16 to 45 46 to 90 Resident if 4 UK ties 91 to 120 Resident if 3 UK ties (or more) 121 to 182 Resident if 1 UK tie (or more) Resident if 2 UK ties (or more) 183 or more Automatically resident Automatically resident Child benefit income tax charge Where income is between £50,000 and £60,000, the charge is 1% of the amount of child benefit received for every £100 of income over £50,000. Property Income 50% of property income finance costs are subject to basic rate restriction. Car Benefit Percentage The base level of CO, emissions is 95 grams per kilometre. The percentage rates applying to petrol cars with CO2 emissions up to this level are: 50 grams per kilometre or less 51 grams to 75 grams per kilometre 76 grams to 94 grams per kilometre 95 grams per kilometre 13% 16% 19% 20% Car Fuel The base figure for calculating the car fuel benefit is £23,400 Individual savings accounts (ISAS) The overall investment limit is £20,000. Pension Contribution Limits The maximum contribution that can be made without evidence of earnings is £3,600. Annual allowance £40,000 Minimum allowance £10,000 Income limit £150,000 The maximum contribution that can qualify for tax relief without any earnings is £3,600. Lifetime Allowance £1,030,000 Authorised mileage allowances All cars up to 10,000 miles over 10,000 miles 45p 25p Cash basis Revenue limit £150,000 Capital Allowances Plant and machinery Main pool Special rate pool 18% 8% Motor cars New cars with CO2 emissions up to 50 grams per kilometre Co2 emissions between 51 and 110 grams per kilometre Co2 emissions over 110 grams per kilometre Annual investment allowance 100% 18% 8% Rate of allowance 100% Expenditure limit £200,000 Cap on income tax reliefs Unless otherwise restricted, reliefs are capped at the higher of £50,000 or 25% of income. Corporation Tax Rate of tax FY 2018 19% Rate of tax FY 2017 19% Profit threshold £1,500,000 Value Added Tax Standard rate 20% Registration limit Deregistration limit £85,000 £83,000 Inheritance Tax: Tax Rates: £325,000 £125,000 Nil rate band Residence nil rate band Excess - Death rate 40% - Lifetime rate 20% Inheritance Tax: Taper relief Percentage reduction Years before death Over 3 but less than 4 years Over 4 but less than 5 years Over 5 but less than 6 years Over 6 but less than 7 years 20% 40% 60% 80% Rates of Interest Official rate of interest: 2.5% Rate of interest on underpaid tax: Rate of interest on overpaid tax: 3.0% 0.5% Capital Gains Tax - Individuals Annual Exempt Amount Rates of tax Normal rates £11,700 - lower rate 10% - higer rate 20% Residential Property rates - lower rate 18% - higher rate - lifetime limit - Rate of tax 28% Entrepreneurs'relief £10,000,000 10% National Insurance (not contracted out rates) Annual Class 1 Employee £1- £8,424 0% (E8,425 - E46,350] £46,351 and above 12% 2% Class 1 Employer £1- £8,424 £8,425 and above 0% 13.8% Employment allowance £3,000 Class 1A 13.8% Class 2 £2.95 per week Small earnings exemption limit £6,205 £1 - £8,424 per year £8,425 - £46,350 per year £46,351 and above per year Class 4 0% 9% 2% 1. Calculations and workings need only be made to the nearest £. 2. All apportionments should be made to the nearest month. 3. All workings should be shown in Section c The following tax rates and allowances will be reproduced in the examination paper for Paper (TX-UK). In addition, other specific information necessary for candidates to answer individual questions will be given as part of the question. For example, in the case of corporate chargeable gains the relevant indexation factors for particular dates will be given. Income Tax Normal Dividend rates rates Basic rate £1 - £34,500 20% 7.5% Higher rate Additional rate £34,501 - £150,000 £150,001 and over 40% 32.5% 45% 38.1% The savings income nil rate bands are £1,000 for a basic rate taxpayer and £500 for a higher rate taxpayer A starting rate of 0% applies to taxable savings income where it falls within the first £5,000 of taxable income The dividend income nil rate band is £2,000 Personal Allowance Personal Allowance 11,850 Transferable amount 1,190 Income limit 100,000 Residence status Days in UK Less than 16 Previously resident Automatically not resident Resident if 4 UK ties (or more) Resident if 3 UK ties (or more) Resident if 2 UK ties (or more) Not previously resident Automatically not resident Automatically not resident 16 to 45 46 to 90 Resident if 4 UK ties 91 to 120 Resident if 3 UK ties (or more) 121 to 182 Resident if 1 UK tie (or more) Resident if 2 UK ties (or more) 183 or more Automatically resident Automatically resident Child benefit income tax charge Where income is between £50,000 and £60,000, the charge is 1% of the amount of child benefit received for every £100 of income over £50,000. Property Income 50% of property income finance costs are subject to basic rate restriction. Car Benefit Percentage The base level of CO, emissions is 95 grams per kilometre. The percentage rates applying to petrol cars with CO2 emissions up to this level are: 50 grams per kilometre or less 51 grams to 75 grams per kilometre 76 grams to 94 grams per kilometre 95 grams per kilometre 13% 16% 19% 20% Car Fuel The base figure for calculating the car fuel benefit is £23,400 Individual savings accounts (ISAS) The overall investment limit is £20,000. Pension Contribution Limits The maximum contribution that can be made without evidence of earnings is £3,600. Annual allowance £40,000 Minimum allowance £10,000 Income limit £150,000 The maximum contribution that can qualify for tax relief without any earnings is £3,600. Lifetime Allowance £1,030,000 Authorised mileage allowances All cars up to 10,000 miles over 10,000 miles 45p 25p Cash basis Revenue limit £150,000 Capital Allowances Plant and machinery Main pool Special rate pool 18% 8% Motor cars New cars with CO2 emissions up to 50 grams per kilometre Co2 emissions between 51 and 110 grams per kilometre Co2 emissions over 110 grams per kilometre Annual investment allowance 100% 18% 8% Rate of allowance 100% Expenditure limit £200,000 Cap on income tax reliefs Unless otherwise restricted, reliefs are capped at the higher of £50,000 or 25% of income. Corporation Tax Rate of tax FY 2018 19% Rate of tax FY 2017 19% Profit threshold £1,500,000 Value Added Tax Standard rate 20% Registration limit Deregistration limit £85,000 £83,000 Inheritance Tax: Tax Rates: £325,000 £125,000 Nil rate band Residence nil rate band Excess - Death rate 40% - Lifetime rate 20% Inheritance Tax: Taper relief Percentage reduction Years before death Over 3 but less than 4 years Over 4 but less than 5 years Over 5 but less than 6 years Over 6 but less than 7 years 20% 40% 60% 80% Rates of Interest Official rate of interest: 2.5% Rate of interest on underpaid tax: Rate of interest on overpaid tax: 3.0% 0.5% Capital Gains Tax - Individuals Annual Exempt Amount Rates of tax Normal rates £11,700 - lower rate 10% - higer rate 20% Residential Property rates - lower rate 18% - higher rate - lifetime limit - Rate of tax 28% Entrepreneurs'relief £10,000,000 10% National Insurance (not contracted out rates) Annual Class 1 Employee £1- £8,424 0% (E8,425 - E46,350] £46,351 and above 12% 2% Class 1 Employer £1- £8,424 £8,425 and above 0% 13.8% Employment allowance £3,000 Class 1A 13.8% Class 2 £2.95 per week Small earnings exemption limit £6,205 £1 - £8,424 per year £8,425 - £46,350 per year £46,351 and above per year Class 4 0% 9% 2% 1. Calculations and workings need only be made to the nearest £. 2. All apportionments should be made to the nearest month. 3. All workings should be shown in Section c

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

For all payroll calculations, use the following tax rates and round amounts to the nearest cent Employee: OASDI: 6.2% on first $118,500 earned; Medicare 1.45% up to 5200,000, 2.35% on earnings above...

-

Use the following tax rates and taxable wage bases: Employees' and Employer's OASDI6.2% both on $118,500; HI1.45% for employees and employers on the total wages paid. Employees' Supplemental HI of...

-

Use the following tax rates and taxable wage bases: Employees' and Employer's OASDI6.2% both on $118,500; HI1.45% for employees and employers on the total wages paid. Employees' Supplemental HI of...

-

Express the given quantity in terms of sin x and cos x. sin 2 X

-

When talking about the economy, people often make a distinction between policies that work only in theory compared to those that work in practice. In theory, a fall in money growth slows down the...

-

What is the market for corporate control? What conditions generally cause this external governance mechanism to become active? How does this mechanism constrain top-level managers' decisions and...

-

A low-power college radio station broadcasts \(10 \mathrm{~W}\) of electromagnetic waves. At what distance from the antenna is the electric field amplitude \(2.0 \times 10^{-3} \mathrm{~V} /...

-

1. A product line is sold in 15 different configurations of packaging. How does the large number of package types influence the value of the chi-squared statistic? 2. Why are chi-squared statistics...

-

< On January 22, Jefferson County Rocks Inc., a marble contractor, issued for cash 230,000 shares of $20 par common stock at $25, and on February 27, it issued for cash 12,000 shares of preferred...

-

An employee earns $55,000 per year and is paid on a semi-monthly pay schedule. The employee enjoys the benefit of a company paid cell phone for personal use (cost is $150 per month) and receives 6%...

-

As shown in the figure, the rectangular flat plate with chamfering has three pin holes. The dimensions are shown in the figure (unit: mm), ignoring the thickness of the plate. Material E=2E11Pa, u=...

-

How can complexity science inform the development of organizational strategy in uncertain environments?

-

How has ICT development changed the skills required by e-business managers?

-

In many fire department organizations with limited budgets and resources, leadership and management training are rarely promoted. All training typically focuses on operational tasks. Make an argument...

-

These questions are from "A first look at communication theory by Em Griffen" These are from chapter 4: Mapping the Territory (Seven Traditions in the Field of Communication Theory) QUESTIONS TO...

-

Technological development in industrial societies often results in highly productive machines effectively replacing animal and human workers. Think of a useful mechanical device and consider its...

-

Marketers create messages about their products and for their customers in a variety of different ways - not just through advertising. This module discusses the IMC or Integrated Marketing...

-

(a) Prove that form an orthonormal basis for R3 for the usual dot product. (b) Find the coordinates of v = (1, 1, 1)T relative to this basis. (c) Verify formula (5.5) in this particular case. 48-65...

-

Fellowes and Associates Chartered Accountants is a successful mid-tier accounting firm with a large range of clients across Canada. During 2011, Fellows and Associates gained a new client, Health...

-

Securimax Limited (Securimax) has been an audit client of KFP Partners (KFP) for the past 15 years. Securimax is based in Waterloo, Ontario, where it manufactures high-tech armor-plated personnel...

-

Required For each of the following situations, indicate what type of modification/audit report is most appropriate. (a) There is a scope limitation and it is material. However, the overall financial...

-

Does the snowflake have rotational symmetry in Figure 1.6? If yes, describe the ways in which the flake can be rotated without changing its appearance. Does it have reflection symmetry? If yes,...

-

Which of the following statements are hypotheses? (a) Heavier objects fall to Earth faster than lighter ones. (b) The planet Mars is inhabited by invisible beings that are able to elude any type of...

-

A battery-operated wall clock no longer keeps timeneither hand moves. Develop a hypothesis explaining why it fails to work, and then make a prediction that permits you to test your hypothesis....

Study smarter with the SolutionInn App